Key Points

- Your beneficiary receives the full death benefit even if you die during the grace period

- Grace periods last 30-31 days on most individual life insurance policies

- You stay fully covered during the grace period at no additional cost

- Your policy lapses permanently after the grace period ends

- Reinstatement has strict limits

You are three weeks late on your life insurance premium. Your inbox has notifications. Your spouse does not know you are stressed about making the payment. Here is what keeps you protected right now, a grace period.

The grace period is a safety unit that is built into almost every life insurance policy. If you miss a premium payment then you are not immediately uninsured. Your policy stays active for a limited time, giving you a window to catch up without losing the coverage or paying the penalties.

And if you die before you pay all the grace period expires, your beneficiaries financial security depends on an understanding exactly how this works.

What Is a Grace Period for Life Insurance?

Grace period is a set number of days, typically 30 or 31 after your premium due date during which your life insurance remains in full force even though you haven’t paid. You are covered at no extra cost. The insurance company hold your policy active. Legally, they cannot drop you during this time.

Think of it as a built-in buffer. Life happens. Payments get lost in the mail. The period recognizes this reality and protects you while you get things sorted.

The key thing to remember is your beneficiary is protected during the grace period. If you pass away, they will receive the full death benefit, minus any unpaid premiums. That is the law in more states.

Will Your Beneficiary Receive the Death Benefit During the Grace Period?

Yes, your beneficiary will receive the full death benefit if you die during the grace period, even if you have not paid the premium.

Here is how it works. If you die on day 15 of your 31 day grace period, the insurance company will pay out your full death benefit. However they will deduct any unpaid premiums from the benefit before sending the check to your beneficiary.

Without grace period, insurance companies “legally deny the entire claim. Instead, they are required to pay. This protection is mediated by state insurance regulation across all 50 states.

How Long Is the Grace Period for Life Insurance?

Most individuals’ life insurance policies offer 30 or 31 days grace periods, though some policies allow up to 60 days

The exact length depends on your specific policy and your insurance company. When you bought your policy, the grace period terms were spelled out in your policy document. The timeframe typically begins on your premium due date, not the date you receive the bill.

Real World Timeline

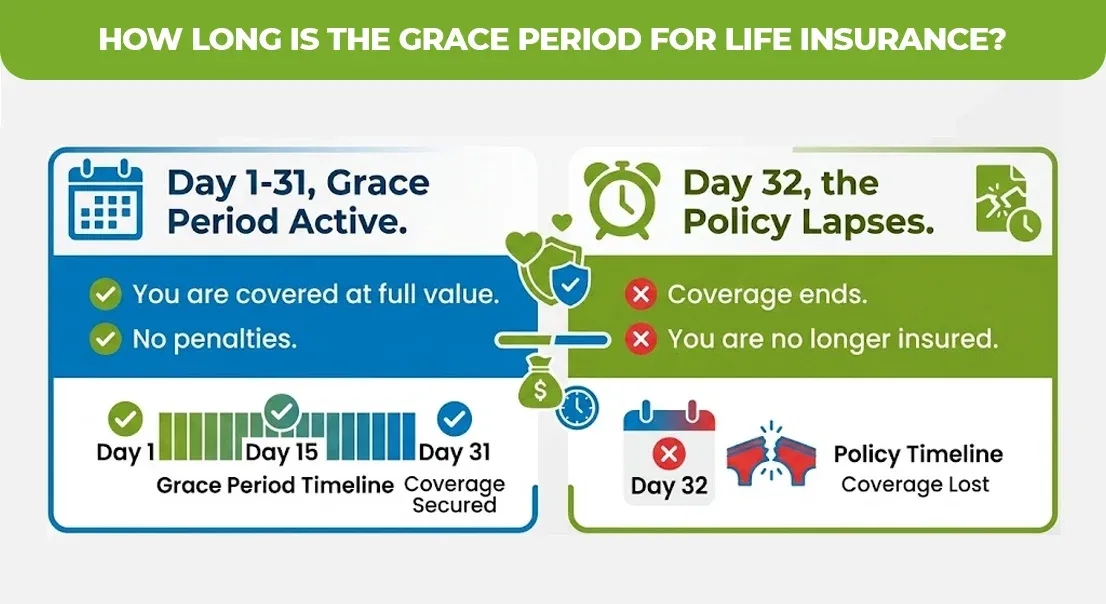

- Day 1-31, grace period active. You are covered at full value. No penalties.

- Day 32, the policy lapses. Coverage ends and you are no longer insured.

Some employers offer group life insurance for longer grace period. That is up to 60 days because group plans have different regulations. Individual policies are stricter and stick to 30 to 31 days as standard.

Accidental death and dismemberment insurance policies follow the same grace period rules. The grace period protects you whether you die from natural causes or an accident.

What Happens After the Grace Period Ends?

Once the grace period expires and you have not paid, your policy lapses. The coverage ends immediately. You are no longer insured.

The lapsed policy is that. It is not suspended. It is not dormant . It is over. Your beneficiary would receive nothing if you died after the grace period because there is no active coverage.

This is very critical. The difference between the 31 and day 32 of grace period can mean $500,000 to your family or nothing at all.

Some people confuse the grace period with the reinstatement period. They are different

Aspect | Grace Period | Reinstatement Period |

Definition | Unpaid coverage window after missed payment | Time frame to restore a lapsed policy |

Length | 30-31 days (typically) | 2-3 years (varies by insurer) |

Cost | Free; no additional premiums | Requires back premiums + interest + possible medical exam |

Coverage Status | Active and paid | Inactive until reinstated |

Underwriting | None required | May require medical underwriting |

Reinstatement: Bringing a Lapsed Policy Back to Life

If your grace period passes in your policy lapses, you have a second chance, the reinstatement period that is usually 2 to 3 years to restore coverage.

But it is not automatic. You have to ask your insurance company to reinstate it. And they have conditions.

To reinstate a lapsed policy, you will typically need

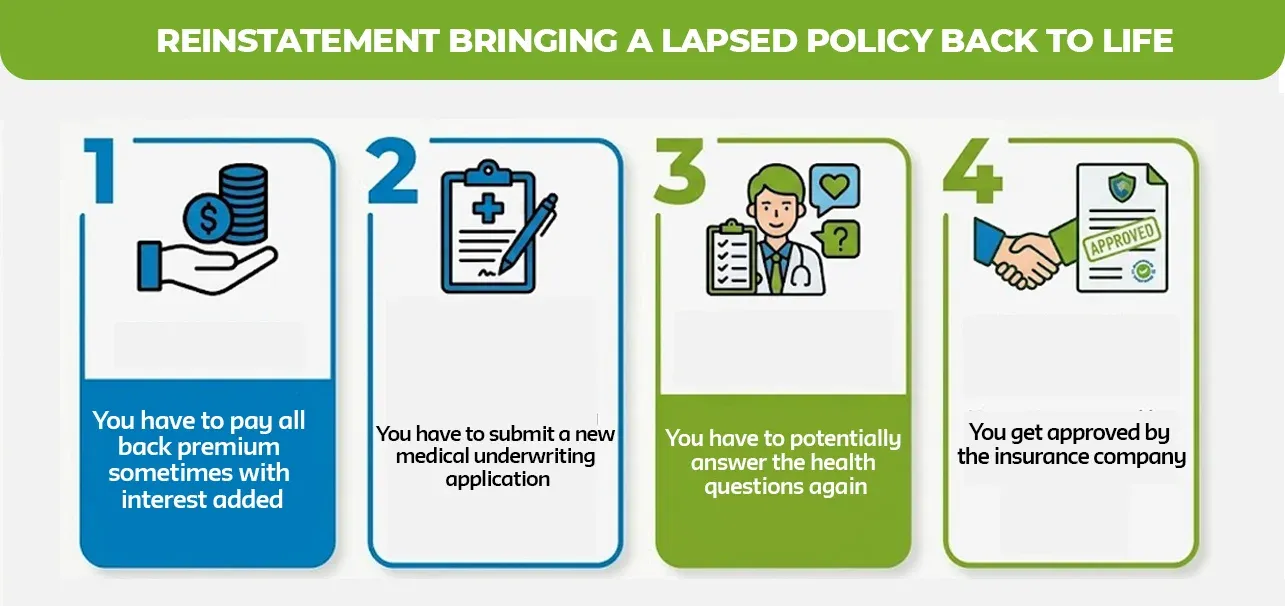

- You have to pay all back premium sometimes with interest added

- You have to submit a new medical underwriting application

- You have to potentially answer the health questions again

- You get approved by the insurance company

Reinstatement is not guaranteed. If your health has declined significantly, then the company can deny reinstatement or approve it at a higher rate.

That is why the grace period matters so much. It is your free pass. Once it is gone, getting coverage back is expensive and uncertain.

Policy Status | Time Window | Cost to Restore | Medical Exam Required? |

Active with paid premium | Ongoing | $0 | No |

During grace period | 30-31 days | $0 | No |

After grace, before lapse | 0 days | N/A | |

Lapsed (reinstatement period) | 2-3 years | Back premiums + interest | Usually yes |

Lapsed (reinstatement period) | N/A | Must apply as new policy | Yes |

Grace Periods and Accidental Death & Dismemberment (AD&D) Insurance

AD&D policies have the same grace period protection as regular life insurance. If you die from an accident during the grace period, your beneficiary will receive the full accidental death benefit, minus unpaid premiums.

The grace period exist for the same reason, that is to protect you during temporary payment caps. Whether your death is accidental or from natural causes, the coverage remains active during those 30 to 31 days

However AD&D policies have strict definitions of what qualifies as an accidental. Suicide, for example typically excluded even during the grace period. But accidental injuries, vehicle accident and falls are covered.

The grace period for an AD&D writer on your main life insurance policy operates on the same timeline as your base policy. A single grace period covers both.

What to Do If You’re in a Grace Period Right Now

If you have messed a payment and you are currentlySLknn win your grace period, use this time. Pay your premium as soon as possible. Call your insurance company if you are unsure of the exact date of the grace period and date.

If you need help understanding your specific policy? Contact your insurance agent or provider directly, they can confirm your exact erase period length and reinstatement terms.

If you want to make sure your life insurance is optimized for your family then M-life Insurance experts can review your current policy, explain your grace period terms and help you to avoid coverage gaps.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.