You have signed up for your employer’s benefits and UC life insurance is included in using that your family is covered. Then you find out that the basic policy pays out only one or two times your salary. Now here near what would actually replace your income or pay off a mortgage.

The gap between that i have coverage and my family would actually be okay is where most of the working adults end up under insured without realizing it. Supplemental life insurance exists and it is specifically for the one to close the cap, but only if you understand how it actually works before you need it.

What Is Supplemental Life Insurance?

The supplemental life insurance is the option coverage that you can purchase at the top of your employer’s basic group life insurance plan. It is usually through the payroll deduction. It is also called voluntary life insurance or supplemental employee life insurance. It is designed to increase your tax benefit beyond what your employer provides for free.

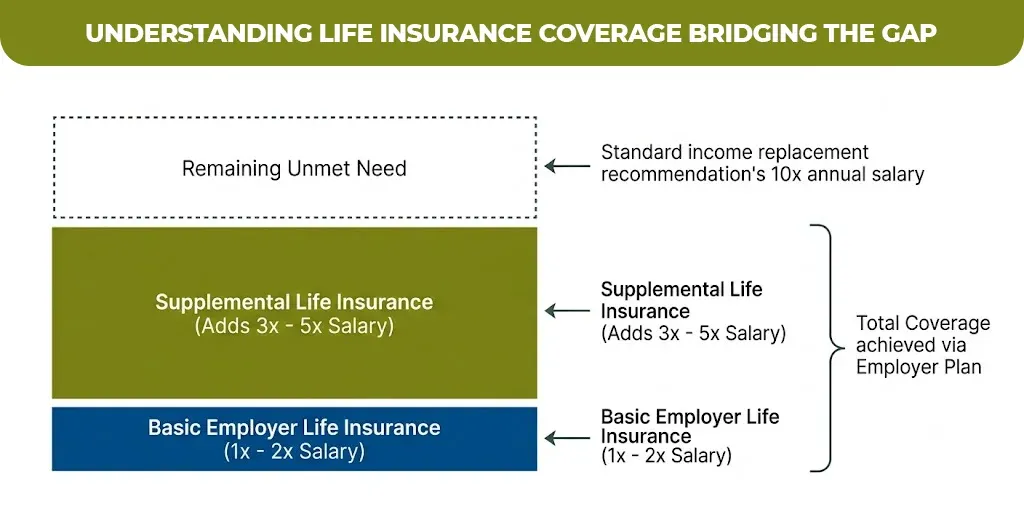

According to MoneyGeek’s 2026 coverage data most of the employers offer a basic life insurance that is equal to one or two times your annual salary at no cost. The supplemental life insurance that you add to that and generally up to 3 to 5 times your salary.You pay the premium yourself, but it’s usually cheaper than buying an equivalent individual policy because employers negotiate group rates.

understanding life insurance coverage bridging the gap

Basic Life Insurance vs. Supplemental Life Insurance: What’s the Difference?

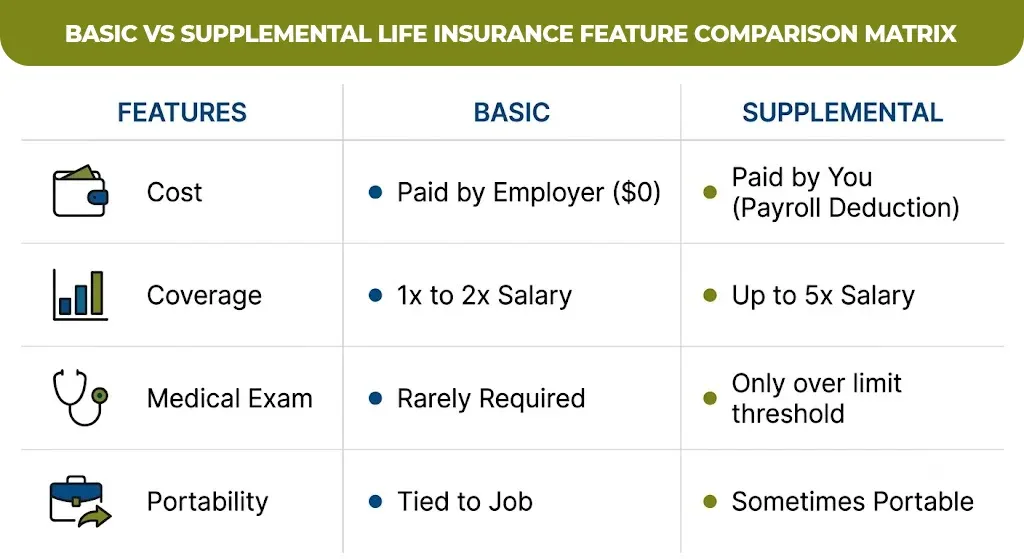

Basic life insurance is the free or low cost policy that your employer provides automatically, while the supplemental life insurance is the additional coverage that you choose to buy and pay for yourself. The two can work together, not as competing products, but as a base layer plus an optional top-up.

| Feature | Basic Life Insurance | Supplemental Life Insurance |

| Who pays the premium | Employer | Employee, via payroll deduction |

| Typical coverage amount | 1x to 2x annual salary | Up to 3x to 5x salary, or flat amounts |

| Medical exam required | Rarely | Only above a guaranteed issue threshold |

| Portability | Usually not portable | Sometimes portable, check with your carrier |

| Cost to employee | Free or minimal | $15 to $30/month is common, varies by age and amount |

An employee earning $70,000 with a standard 1x basic policy has $70,000 in coverage automatically. If that same employee’s family actually needs closer to $500,000 to cover a mortgage, childcare, and years of lost income, supplemental life insurance is the tool built to close that specific gap without leaving the employer’s plan entirely.

How Does Supplemental Life Insurance Work?

You elect supplemental coverage during open enrollment or after a qualifying life event, choose a coverage amount in salary multiples or flat dollar increments, and the premium comes out of your paycheck automatically. Coverage is often available up to a set threshold, commonly $200,000 to $500,000, without a medical exam, which is one of the biggest practical advantages over shopping for an individual policy.

Above that guaranteed issue threshold, the insurer may require health questions or a full medical exam before approving higher amounts. Premiums are typically based on your age, and they increase as you get older, since this is usually structured as yearly renewable term coverage rather than a fixed-rate policy.

What Does Supplemental Life Insurance Cover?

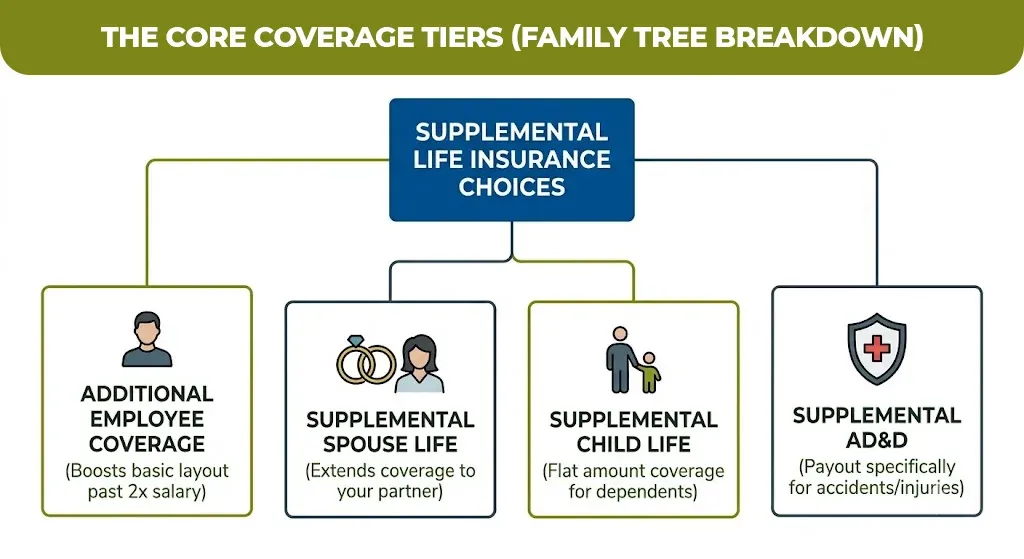

The supplemental life insurance fee that benefits for most of the causes of death, and so many plans also that you had the coverage for a spouse, domestic partner or dependent children. There are some employers who are also often accidental death and dismemberment coverage as a separate writer within the same supplemental plan.

The main categories generally available include

- Additional employee coverage: increases your own death benefit beyond the basic policy

- Supplemental spouse life insurance: extends coverage to a spouse or domestic partner, usually at a lower amount than the employee’s own coverage

- Supplemental child life insurance: covers dependent children, often as a flat amount like $10,000 or $25,000

- Supplemental life and AD&D insurance: adds a payout specifically for accidental death or serious injury, on top of the standard death benefit

Family coverage tiers are usually smaller than what’s available to the employee, and you typically have to elect coverage for yourself before you can add a spouse or child, according to Guardian’s overview of supplemental life insurance.

Is Supplemental Life Insurance Worth It?

Supplemental life insurance is worth it if you have a genuine coverage gap, a health condition that limits your options elsewhere, or an employer that subsidizes part of the premium. It works less well as your only source of life insurance, since coverage typically ends the moment you leave your job.

LIMRA’s 2025 research found that only 51% of American adults own any form of life insurance, leaving a substantial share of households under-protected or entirely uninsured.

The tradeoff is portability. If your job ends, so does most supplemental coverage, unless your plan specifically allows conversion to an individual policy. That’s the main reason financial professionals generally recommend supplemental life insurance as a layer on top of an individual policy, not a full replacement for one.

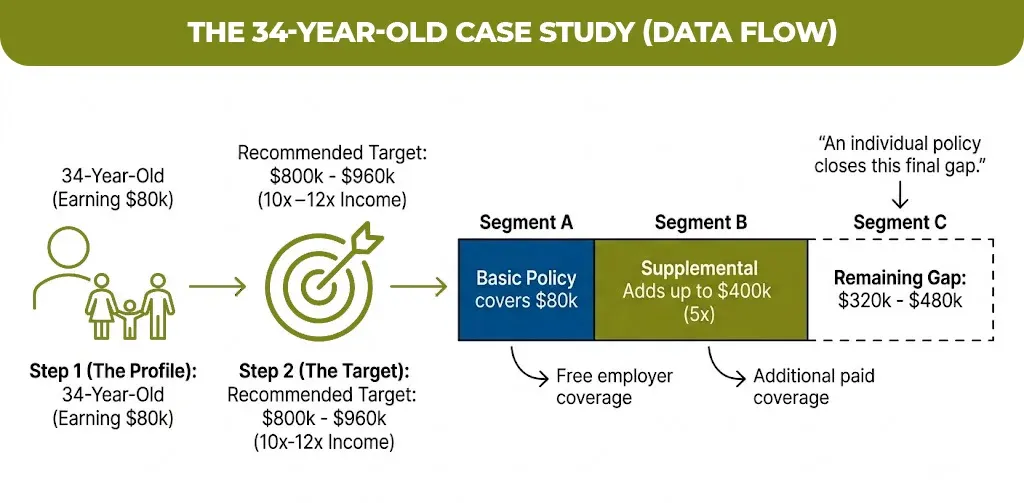

Calculating Your Actual Coverage Gap With The Help Of Example

Consider a 34-year-old earning $80,000 with a spouse and two young children. Their employer provides basic life insurance equal to one times salary, or $80,000, at no cost.

Financial professionals commonly suggest total coverage of 10 to 12 times annual income for households with young dependents, which in this case would be roughly $800,000 to $960,000. That leaves a coverage gap of $720,000 to $880,000 after subtracting the free basic policy, a gap that supplemental life insurance, capped at 3x to 5x salary through most employer plans, would only partially close, meaning an individual policy may still be needed to fully cover the difference.

Is Supplemental Life Insurance Taxable?

The death benefit itself is generally not taxable to your beneficiary, following the same tax treatment as any other life insurance payout. There’s one specific wrinkle worth knowing if your employer pays any part of the premium.

Under IRS rules, the first $50,000 of employer-paid group term life insurance is tax-free; coverage above that amount can create a small amount of taxable imputed income, calculated using IRS Table I rates. This is generally applies to the basic coverage paid entirely by the employer rather than supplemental coverage you pay for yourself, but it’s worth confirming with your HR or benefits team if you’re unsure how your specific plan is structured.

If you’ve run the numbers and found a real gap between your basic coverage and what your family would actually need, M-Life Insurance can help you figure out whether an individual policy, more supplemental coverage, or a combination of both makes the most sense for your budget.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.