Key Benefits

- Height and weight impact premiums

- Build charts vary by insurer

- Small weight changes affect rates

- Wrong carrier can cost thousands

- Pre-check charts before applying

You filled out the application. You felt confident. Then came the denial or worse, a premium three times higher than the quote you expected.

Most people don’t realize that their height and weight alone can determine whether they are approved, rated up or decline entirely. The insurance companies use a life insurance build chart that is a height weight grid directly to your underwriting classification. If you apply without checking it first, you are flying blind.

What Is a Life Insurance Build Chart?

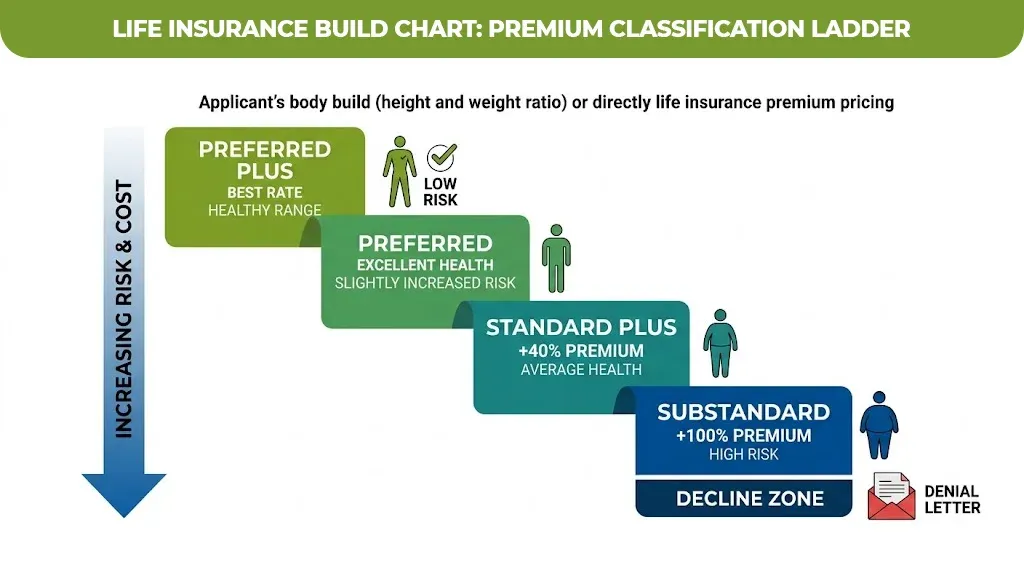

A life insurance build chart is a standardized table that is used by the insurance companies to evaluate an applicant’s body size relative to mortality risk. It makes your height to your weight to assign an appealed rating, which then feeds into your overall underwriting class.

Your class – preferred class, preferred, standard, substandard or decline drives your premium. A difference of one classification can mean paying 40 to 100% more per year or being declined outright.

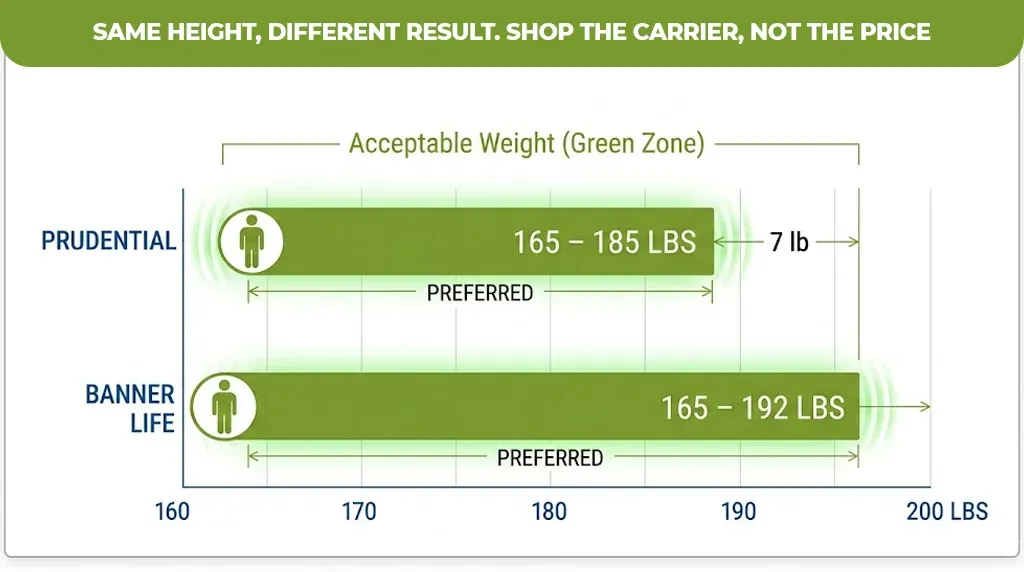

Most of the major insurance carriers including Prudential, banner life, and Pacific life publish their own proprietary build charts. The ranges are similar but not identical, which is why shopping multiple insurance companies matters.

How the Build Chart Actually Works: Height, Weight, and BMI

Insurance does not use BMI. They look at your actual weight to height ratio using their internal buildable, which is often stricter than the standard CDC BMI classifications.

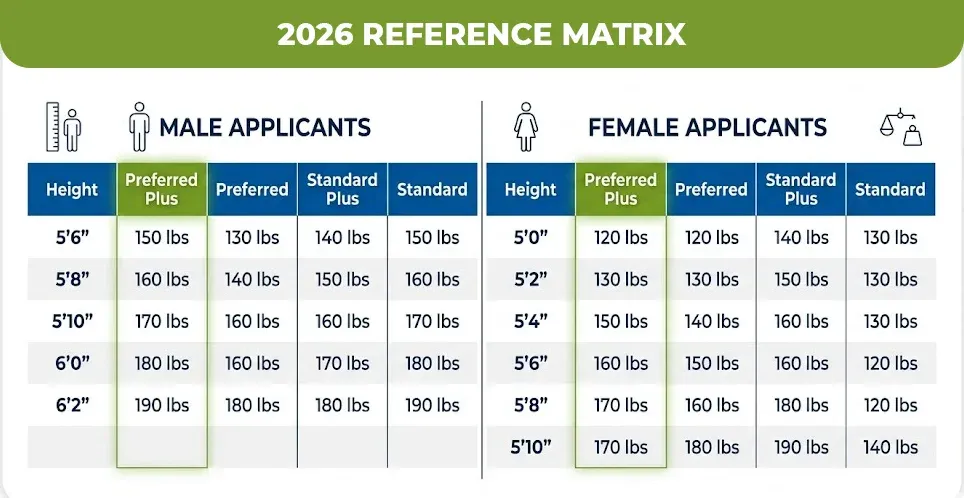

Here is a general 2026 reference guide based on standard industry build charts values represent maximum weight for each classification

Life Insurance Build Chart — Male (2026 Reference)

| Height | Preferred Plus | Preferred | Standard Plus | Standard |

| 5’6″ | 174 lbs | 185 lbs | 202 lbs | 220 lbs |

| 5’8 | 185 lbs | 197 lbs | 215 lbs | 234 lbs |

| 5’10” | 196 lbs | 209 lbs | 228 lbs | 249 lbs |

| 6’0″ | 209 lbs | 222 lbs | 243 lbs | 264 lbs |

| 6’2″ | 222 lbs | 236 lbs | 257 lbs | 280 lbs |

Life Insurance Height and Weight Chart — Female (2026 Reference)

| Height | Preferred Plus | Preferred | Standard Plus | Standard |

| 5’6″ | 148 lbs | 158 lbs | 172 lbs | 188 lbs |

| 5’4 | 157 lbs | 167 lbs | 182 lbs | 199 lbs |

| 5’6″ | 166 lbs | 177 lbs | 193 lbs | 210 lbs |

| 5’8″ | 176 lbs | 187 lbs | 204 lbs | 222 lbs |

| 5’10” | 186 lbs | 198 lbs | 216 lbs | 235 lbs |

Note that these are approximate composite values. Individual carriers charts can be different, always verified with a licensed agent or the specific carriers underwriting guidelines.

Prudential Build Chart: What Makes It Different

The Prudential build chart is one of the most widely referenced in the industry, particularly for the applicants in the midweight range. Potential uses a dual threshold model they look at both maximum and minimum weight for height, which is being significantly overweight can also affect your rating.

Potential preferred plus category generally requires a BMI between 17 and 28. The applicants above 38 BMI are typically limited to standard or sub standard classification. Their underwriting guidelines, including build tables are available through licensed brokers for their agent portal.

Banner Life Insurance Weight Chart: A More Lenient Option?

Banner life insurance that is operated by legal and general America is often cited as one of the most applicant friendly carriers for build. Their weight limits for preferred classification tend to run 5 to 8 Lbs higher than potential at most height for male applicants.

For female applicants, banners standard plus threshold is not notably more forgiving then the industry average for height under 5 ‘5. If you have been declined or rated up by another carrier, banner is frequently the next application independent brokers recommend.

Life Insurance BMI Requirements: When BMI Alone Isn’t the Full Story

Most people assume insurance companies used standard BMI cut off. Actually they don’t, not entirely. While life insurance BMI requirements are part of the equation, carriers also factored in build high to weight ratio, waist circumference in some cases and medical history.

According to American Academy of Insurance Medicine (AAIM), body build is one of the top five factors, alongside blood pressure, cholesterol, tobacco use and family history. BMI is a proxy, where build charts are the actual tools.

BMI of 31, you are in a standard with one carrier and standard plus with another, depending on how their propriety build table is weighted. This is why getting multiple cords is not optional, it is an essential strategy.

How to Use a Life Insurance Build Chart Before You Apply

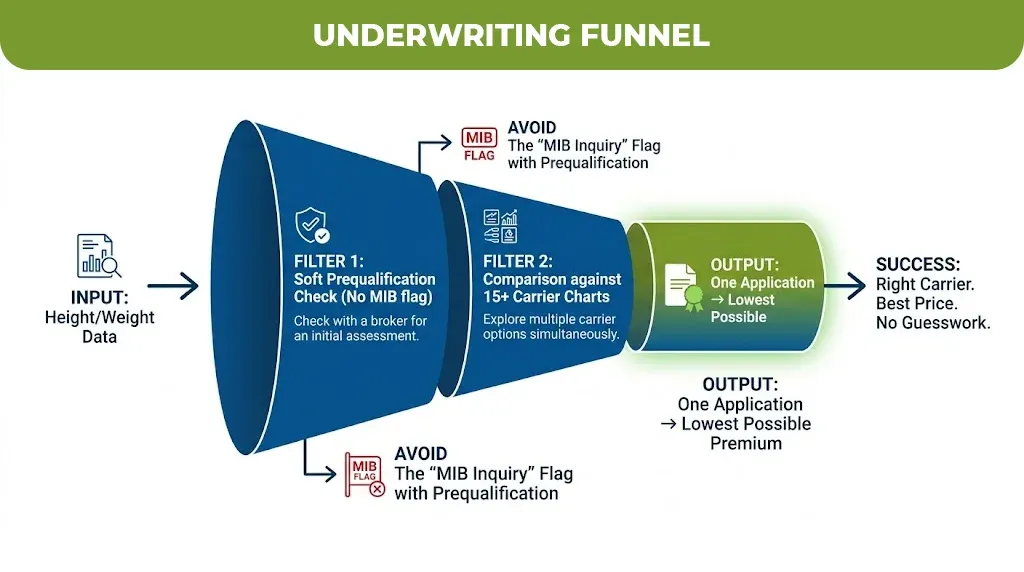

Check your height and your weight against the multiple carriers charge before submitting any application. Each formal application triggers a medical information Bureau MIB inquiry, and multiple applications in a short window can raise flags for underwriters.

There are three steps to protect yourself

- Use a broker who has access to at least 10 to 15 carriers and can run a soft prequalification check.

- Ask specifically about build chart threshold before any application is submitted

- If you are within 10 to 15 LBS of a classification boundary then ask the broker which carrier’s chart gives you the best placement.

A broker runs your number first like no application until you know where you will land.

Find the Right Coverage Without Guessing

If you have read this far, you already understand something most applicants don’t: that the build chart is a system and you can navigate it strategically.

The difference between the right carrier and the wrong one could mean thousands of dollars over your policy. An independent broker with multiple carrier underwriting can tell you for a simple application is filed exactly where you will likely land.

At M-life Insurance, our licensed team runs prequalification checks across our carriers so you can apply once, to the right place, with the best possible outcome. No guesswork. No surprises on your premiums.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.