Are you curious about a type of life insurance that works with your budget changes? How does graded premium life insurance differ from a life insurance policy? How can premium life insurance provide financial peace of mind for the future?

Welcome to the world of premium life insurance! Enter the solution that prompts the question: What if your insurance premiums could start low and gradually increase over time? This premium life insurance is a dynamic option designed to offer affordability in the early years while accommodating the potential growth in your financial capacity.

Let’s delve into this innovative approach that balances your present circumstances and future aspirations, providing a unique perspective on life insurance tailored to your journey.

What is Graded Premium Life Insurance?

A premium life insurance is a unique form of life insurance that offers a flexible payment structure, particularly designed to accommodate individuals whose budgetary constraints may vary over time. Unlike traditional life insurance plans with fixed premiums, graded premium life insurance starts with lower initial premium payments, increasing gradually over the policy’s term.

This structure allows policyholders to ease into the financial commitment associated with life insurance, making it especially appealing for those with limited resources early in their careers. The graded increase in premiums typically occurs at predetermined intervals, providing individuals with the opportunity to adjust to changing financial circumstances.

It’s an option that balances providing essential life coverage and recognizing the potential fluctuations in a policyholder’s ability to pay premiums. This life insurance aims to make life insurance accessible to a broader demographic, ensuring that financial protection remains within reach throughout various stages of an individual’s life.

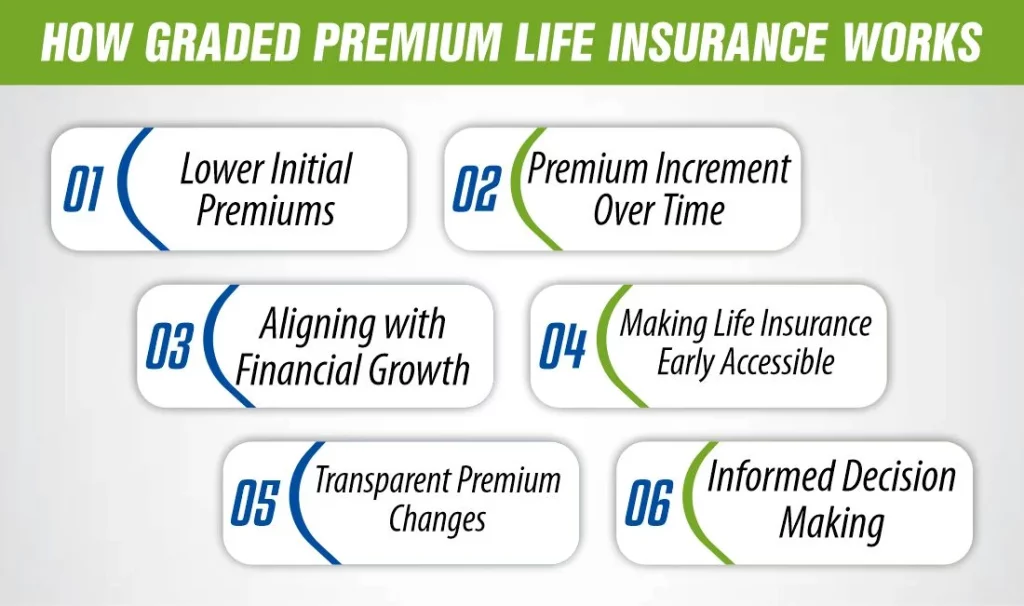

How Graded Premium Life Insurance Works?

This life insurance operates on a distinct payment structure that sets it apart from traditional life insurance plans. At its core, this insurance type eases the financial burden on policyholders, especially those who might face budgetary constraints early in their careers or during specific life stages.

1- Lower Initial Premiums

Insurance policy begins with lower initial premiums, providing an accessible entry point for individuals seeking life coverage without a significant upfront financial commitment.

2- Premium Increment Over Time

A defining feature of this insurance is the graded increase in premiums. Rather than a fixed amount, premiums gradually rise at predetermined intervals, allowing policyholders to adapt to changing financial circumstances.

3- Aligning with Financial Growth

The adaptive structure of graded premiums aligns with the policyholder’s financial journey, acknowledging the potential for increased stability as individuals progress through their careers.

4- Making Life Insurance Early Accessible

This life insurance is an ideal choice for those looking for budget-friendly entry into life coverage, especially during early career stages or periods of financial constraint.

5- Transparent Premium Changes

Policyholders benefit from transparent and predictable premium adjustments. The predetermined increases provide clarity, allowing individuals to plan for future changes.

6- Informed Decision-Making

Policyholders can make informed decisions about their coverage, considering the graded structure and planning strategically for future premium adjustments. Premium life insurance plan offers a dynamic and flexible approach to life coverage, aligning with individuals’ financial realities and aspirations.

Secure Your Family's Future with Confidence

Don’t leave your loved ones' financial security to chance. Use our expert tools and free resources to find the perfect coverage today.

How Is the Graded Premium Life Insurance Modified?

Graded premium life insurance changes its cost over time in a planned way. When you start the policy, the insurance company decides on a schedule to increase the payments gradually. This helps ensure that the insurance stays affordable initially, and as your money situation improves, the payments go up. The idea is to make it easier for people to start with lower payments and adjust as they can afford more later.

Pros and Cons of Graded Premium Life Insurance

In deciding on premium life insurance, individuals should thoroughly assess their Pros and cons:

Pros

- Affordability in Initial Premiums

This life insurance stands out for its affordability. The lower initial premiums make life coverage accessible, especially for those navigating budget constraints or early careers. This advantage ensures individuals can initiate their life insurance journey without a substantial upfront financial burden. The affordable entry point enables a broader demographic to secure essential life coverage, promoting financial inclusivity.

- Balanced Financial Commitment

The gradual increase in premiums provides a balanced financial commitment. This feature particularly benefits individuals anticipating improved financial situations but prefers starting with more affordable premiums.

- Gradual Premium Increase

One of the key strengths of this life insurance lie in its graded increase in premiums. This incremental approach allows policyholders to navigate the financial commitment more comfortably. Predictable increases at predetermined intervals enable individuals to plan for adjustments, aligning their coverage with evolving financial capabilities. The gradual premium increase is a strategic feature, acknowledging that financial circumstances can change over time and providing a balanced approach to managing life insurance costs.

- Transparent Predictability

Graded premiums bring transparency and predictability to financial planning. Policyholders know when and how premiums will increase, allowing for informed decision-making and enabling them to align their coverage with their evolving financial capabilities.

- Cash Value Accumulation

These premium life insurance policies often offer a cash value accumulation component. As policyholders pay premiums, some of these payments accumulate as cash value over the policy’s duration. This cash value serves as a valuable asset, providing individuals with flexibility. They can access this accumulated value or borrow against it for various financial needs, offering policyholders an additional layer of financial security and versatility. The cash value accumulation feature enhances the overall financial value of the life insurance policy.

- Customized Approach

This life insurance offers a customized approach to life coverage. It recognizes the diverse financial journeys of individuals, allowing them to tailor their insurance to match their unique circumstances and aspirations.

Cons

- Long-Term Cost Increase

While the initial premiums are low, this insurance plan may become more expensive over time. The gradual cost increase could lead to higher overall expenses compared to other types of life insurance with fixed premiums.

- Potential Budget Strain

Despite the predictability, the gradual rise in premiums might still create challenges for some people’s budgets. If there are unexpected financial difficulties or delays in improvement, the increasing costs may pose a strain.

- May Not Be Cost-Effective in the Long Run

This life insurance may not be the most cost-effective choice for those with stable and consistent finances. Individuals expecting long-term financial stability might find traditional policies with fixed premiums to offer better value over time.

- Limited Immediate Affordability for Some

While designed for affordability, some individuals may still need help to meet the initial premiums. In such cases, alternative insurance options with more immediate affordability may be more suitable.

Eligibility Criteria for Graded Premium Life Insurance

The eligibility requirements for premium life insurance are similar to those for any other insurance policy. While the exact requirements may vary among insurance providers, some common factors typically influence eligibility:

- Age: Insurance companies usually set age limits for applicants. This life insurance may be available to individuals within a specific age range, and eligibility can differ based on term or permanent life insurance.

- Health Status: Health is a significant factor in determining eligibility. Insurers may assess your health through a medical examination or health questionnaire. Life insurance might be more lenient than traditional policies, making it accessible to individuals with certain health conditions.

- Financial Stability: While graded premiums are designed to be affordable initially, insurers may evaluate your financial stability. This assessment ensures that you can meet the increasing premium payments over time.

- Coverage Amount: Eligibility may also depend on the desired coverage amount. Insurance providers may have minimum and maximum limits for the death benefit, and your eligibility could be influenced by the coverage you seek.

- Insurance History: Your previous insurance history, if any, can impact eligibility. Insurers may consider your experience with other insurance policies and your payment history.

To determine your eligibility accurately, it is advisable to consult with insurance professionals, carefully review the specific policy terms, and provide accurate information during the application process.

Comparison Graded Premium vs. Modified Whole Life Insurance

A quick comparison between Graded Premium vs. Modified Whole Life Insurance:

- Graded Premium Life Insurance

Graded Premium Life Insurance stands out for its unique premium structure. It begins with lower initial premiums, offering individuals an affordable entry point into life coverage. This accessibility is particularly beneficial for those with budget constraints early in their careers or individuals facing financial challenges. The graded increase in premiums occurs at predetermined intervals, providing a transparent and predictable schedule for policyholders.

- Modified Whole Life Insurance

Modified Whole Life Insurance takes a different approach, with an initial period featuring lower premiums. This design allows policyholders to enjoy affordability in the early years, making it an attractive option for those seeking a balance between lower initial costs and a more predictable premium structure over the long term. After the initial period, premiums transition to a higher, fixed amount. The death benefit remains in place throughout the policy’s duration, although the premium adjustments can influence the overall death benefit amount.

Key Contrasts: Graded Premium vs. Modified Whole Life Insurance

While both Graded Premium and Modified Whole Life Insurance aim to provide accessible options for individuals seeking life coverage, their premium structures and overall approaches differ.

- Graded Premium Life Insurance focuses on affordability initially, with gradual premium increases catering to those with fluctuating budgets.

- On the other hand, Modified Whole Life Insurance offers lower initial premiums, followed by a transition to fixed premiums, striking a balance between affordability in the early years and a more predictable long-term premium structure.

Choosing between the two depends on individual preferences, financial goals, and circumstances. It’s advisable to consult with insurance professionals to determine the most suitable option based on one’s unique needs.

Conclusion

In life insurance, Graded Premium Life Insurance is like a friendly guide, ensuring everyone can access the protection they need. Starting with low-cost premiums, it’s perfect for those just beginning their careers or going through tight money times.

What’s cool is that the cost slowly increases over time, giving you room to adjust as your money situation improves. It’s like a financial friend, constantly adapting to what you can afford. With clear and predictable changes in the cost and even a nod to folks with health concerns, Premium Life Insurance is saying, “Hey, everyone deserves a shot at affordable coverage!” So, if you’re looking for a budget-friendly and flexible way to safeguard your future, this Premium Life Insurance could be your go-to companion on this financial journey.

FAQS

It is a type of permanent whole life insurance where the premiums start very low and increase annually or every few years for a set period (usually 5 to 10 years). After this initial “graded” phase, the premium reaches a fixed amount and remains level for the rest of your life.

The main advantage is affordability at the start. It allows young professionals, medical students, or new business owners with temporary budget constraints to secure a large amount of permanent lifetime coverage immediately, without paying high upfront costs.

Because initial premiums are low, the cash value builds up much slower during the first few years compared to standard whole life. However, once the graded period ends and premiums level out at a higher rate, the cash value accumulation accelerates and grows tax-deferred.

Yes. As the owner, you can cancel the policy at any time, but if you do so early during the graded period, you will likely receive little to no cash surrender value. It cannot be converted back to a lower premium rate, so you must ensure your future budget can handle the scheduled increases.

This is a common point of confusion! A Graded Premium policy changes the cost over time but provides full coverage from day one. A Graded Benefit policy keeps the cost level but restricts the payout during the first two years, usually for applicants with severe health issues.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.