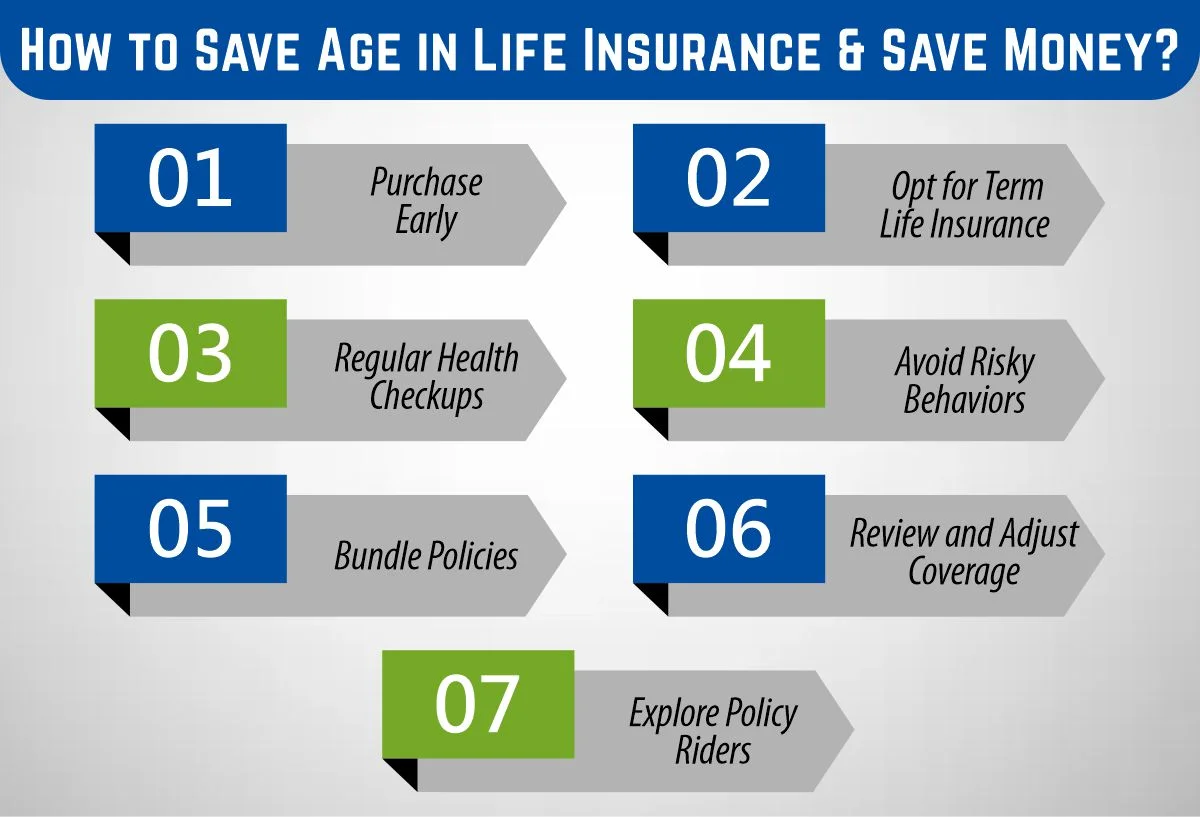

How to Save Age in Life Insurance and Save Money?

Saving age on life insurance is a strategic move that can translate into significant cost savings over the life of your policy. Here’s a breakdown of effective ways to save age in life insurance and, in turn, save money:

1- Purchase Early

The golden rule is to buy life insurance as early as possible. Insurance premiums are often directly tied to age, and younger individuals generally enjoy lower rates. Locking in a policy at a younger age can result in substantial long-term savings.

2- Opt for Term Life Insurance

Consider choosing term life insurance, especially if you are looking for cost-effective coverage. Term policies offer protection for a specific period, and their premiums are typically more affordable than those of permanent life insurance.

3- Regular Health Checkups

Maintain good health, as it directly impacts your insurability and premium rates. Regular health checkups and a healthy lifestyle can contribute to lower premiums. Insurance companies often offer better rates to individuals with a clean bill of health.

4- Avoid Risky Behaviors

Insurance companies assess risk factors when determining premiums. Engaging in risky behaviors such as smoking or participating in extreme sports can lead to higher premiums. By avoiding such behaviors, you not only enhance your well-being but also save on insurance costs.

5- Bundle Policies

Consider bundling your life insurance with other insurance policies like home or auto insurance. Many insurance providers offer discounts for bundled policies, providing an opportunity for additional savings.

6- Review and Adjust Coverage

Regularly review your life insurance policy and adjust the coverage as needed. Life circumstances change, and your coverage should reflect your current financial situation. By ensuring your coverage aligns with your needs, you can avoid overpaying for unnecessary protection.

7- Explore Policy Riders

Policy riders are additional features that can be added to your life insurance policy. Some riders may help you save money by providing flexible options or additional benefits. Explore available riders and assess if any align with your needs.

How Long Can You Backdate a Life Insurance Policy?

The ability to backdate a life insurance policy typically comes with certain limitations, and the specific rules can vary among insurance providers. In general, insurance companies may allow policyholders to backdate a policy for a specified duration, usually up to six months from the date of application.

Here are key points to consider regarding the duration for which you can backdate a life insurance policy:

Policyholder Age

The allowable backdating period often depends on the age of the policyholder at the time of application. Younger individuals may have a more extended window for backdating compared to older applicants.

Insurance Company Policies

Different insurance companies have varying rules regarding backdating. It’s crucial to review the specific guidelines of your chosen insurer to understand their limitations on backdating.

Purpose of Backdating

Insurance companies generally require a valid reason for backdating a policy. Common reasons include aligning the policy’s effective date with a significant life event or obtaining a lower premium by basing it on a younger age.

Premium Payments

When a policy is backdated, the policyholder is usually required to pay the premiums retroactively from the selected effective date. This means catching up on missed premium payments for the period being backdated.

Consultation with the Insurer

If you are considering backdating your life insurance policy, it’s advisable to consult with your insurance company directly. They can provide specific information about their backdating policies, including the allowable duration and any associated requirements.

What Happens When an Insurance Policy is Backdated?

When an insurance policy is backdated, it means that the effective date of the policy is set to a date in the past, typically before the actual application date. This can have several implications, both in terms of premium calculations and the overall administration of the insurance policy.

Here’s what happens when an insurance policy is backdated:

Premium Calculation

The primary impact of backdating is on premium calculations. The premium for a life insurance policy is often determined based on the age of the insured at the time of application. By backdating, the insurance company recalculates the premiums, considering the lower age of the insured at the earlier effective date.

Premium Payment

If the policy is backdated, the policyholder is generally required to pay the premiums retroactively from the selected effective date. This means catching up on the missed premium payments for the period being backdated. The policyholder must settle any outstanding premiums before the policy becomes active.

Policy Term Adjustment

Backdating affects the term of the insurance policy. If the policy is backdated by, for example, six months, the coverage period effectively starts six months earlier than the application date. This adjustment can impact when the coverage expires.

Underwriting Considerations

The underwriting process, which assesses the risk associated with insuring an individual, may take into account the health status and other relevant factors at the backdated effective date. This is crucial for determining the appropriateness of the backdating request.

Policy Activation

The insurance policy is not considered active until the backdated premiums are paid. Once the policyholder fulfills the premium payment obligations, the policy becomes active, and the coverage takes effect from the backdated effective date.

It’s important for policyholders to carefully consider the implications of backdating, including the financial commitment required to pay retroactive premiums. While backdating can result in lower premiums based on a younger age, individuals should weigh the benefits against the costs and ensure that it aligns with their overall financial strategy.

Tips to Save on Life Insurance

Securing life insurance is a vital financial decision, but it doesn’t have to break the bank. Here are some practical tips to help you save on life insurance while still ensuring that you provide financial protection for your loved ones:

Purchase Early:

Act sooner rather than later. Premiums are often lower for younger individuals, as age is a significant factor in determining life insurance rates. Lock in a lower rate by purchasing a policy when you’re younger and healthier.

Choose Term Life Insurance:

Consider term life insurance for cost-effective coverage. Term policies offer protection for a specific period, and their premiums are generally more affordable than those of permanent life insurance.

Maintain Good Health:

Your health directly influences your insurability and premium rates. Adopt a healthy lifestyle, including regular exercise and a balanced diet. Non-smokers often qualify for lower premiums, so consider quitting smoking to save on costs.

Shop Around:

Don’t settle for the first quote you receive. Compare rates from multiple insurance providers to find the best deal. Different companies may offer varying premiums for similar coverage.

Bundle Policies:

Explore the option of bundling your life insurance with other insurance policies, such as home or auto insurance. Many insurers provide discounts for bundled policies, leading to overall cost savings.

Consider Group Insurance:

Check if your employer offers group life insurance as part of the employee benefits package. Group policies often have lower premiums, and some companies even provide coverage without requiring a medical exam.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.