Most people pick a life insurance company the same way they pick a streaming service: they go with the name they recognize most. That is how families end up overpaying by thousands of dollars over a 20-year policy term, or worse, locked into coverage that does not pay out how they expected.

Choosing from the best life insurance company is not about finding the most advertised brand. It is about matching your financial situation, health, and coverage goals to the right company, at the right price, before you sign anything.

Which Company Has the Best Life Insurance in 2026?

The honest answer is that it depends on what you need. But here is the short version for the most common situations:

According to Insure.com’s 2026 rankings, based on a survey of over 2,000 U.S. life insurance consumers, the north western mutual ranked the number one overall for the financial strain, low compliant for him and also the customer satisfaction. It holds an A+ plus rating from a.m. best, that is the highest possible designation for a US life insurance company.

If you want whole life with strong cash value growth, MassMutual and Guardian are the top competitors. If price is your priority, Banner Life and Transamerica consistently deliver premiums well below the industry average.

The industry average premium sits at $382 per year, but the most affordable carriers, including Corebridge Financial, Lincoln Financial, Pacific Life, and Transamerica, all come in noticeably below that figure.

Top 10 Life Insurance Best Rated Companies: 2026 Comparison Table

| Company | Best For | AM Best Rating | COMDEX Score | Avg. Annual Premium |

| Northwestern Mutual | Overall / Customer service | A++ | 100 | Above average |

| New York Life | Seniors / Financial strength | A++ | 100 | Above average |

| Guardian Life | Affordable term / HIV coverage | A++ | 99 | Moderate |

| MassMutual | Whole life / Cash value | A++ | 98 | Moderate |

| Protective | Best term life rates | A+ | 97 | Below average |

| USAA | Military / Veterans | A | 94 | Moderate |

| Pacific Life | Budget-conscious buyers | A+ | 85+ | Below average |

| Transamerica | Lowest premiums | A | 93 | Lowest |

| Mutual of Omaha | Ease of service | A+ | 92 | Moderate |

| Banner Life | Term value / Healthy applicants | A+ | 92 | Lowest |

Best Whole Life Insurance Companies: Where Cash Value Actually Grows

Whole life is a different product category and requires a different comparison framework. You are not just buying a death benefit. You are buying a long-term financial instrument, and dividend history matters as much as the premium.

As of January 20 26, the north western mutual and New York live share the perfect comdex scores for for 100, the only two United States life insurance companies at that level holding A+ plus from a.m. best and AA plus from S&P, Aaa from Moody’s, and AAA from Fitch.

Northwestern Mutual also announced a record $9.2 billion dividend payout for 2026, the largest in the company’s history and in industry history, with surplus hitting a company-record $42 billion.

MassMutual is the strongest competitor on flexibility. MassMutual offers the most customizable paid-up additions riders among mutual insurers, along with high cash value growth rates, making it the go-to for buyers who want to build cash value aggressively over time.

For buyers who want mutual company benefits without the premium price tag of the top two, Penn Mutual and Guardian are worth a serious look.

Best Term Life Insurance Companies: What Actually Saves You Money

Term life is where the biggest pricing gaps exist between companies. Paying more for a famous brand name buys you nothing extra when the underlying financial strength is nearly identical.

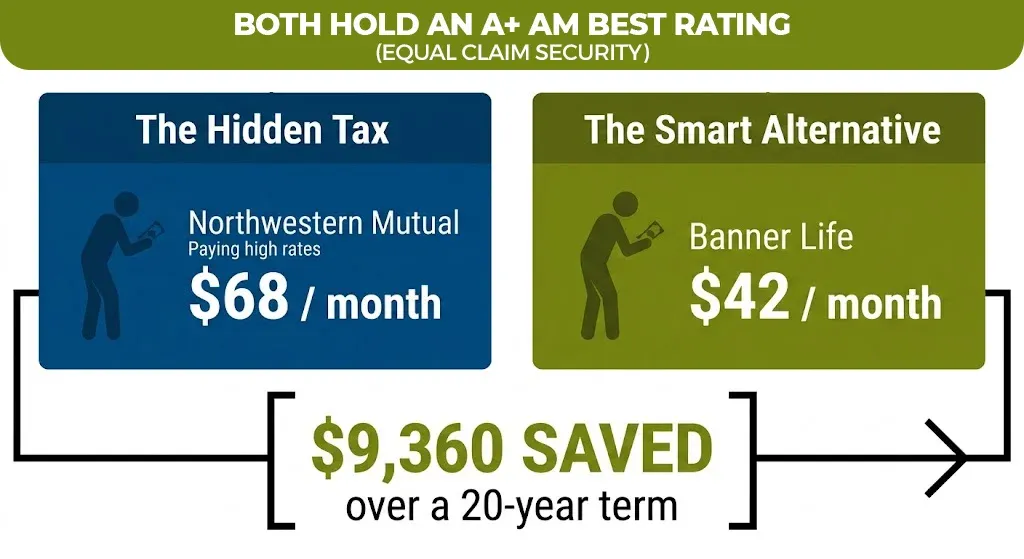

A 40-year-old male buying $500,000 in 20-year term coverage pays approximately $68 per month with Northwestern Mutual and $42 per month with Banner Life. Both carry A+ AM Best ratings. Both will pay the claim. That $26 per month difference is $9,360 over the policy term, locked in permanently at application.

What Financial Strength Ratings Actually Mean for You

This is the section most comparison guides skip, and it is the most important one.

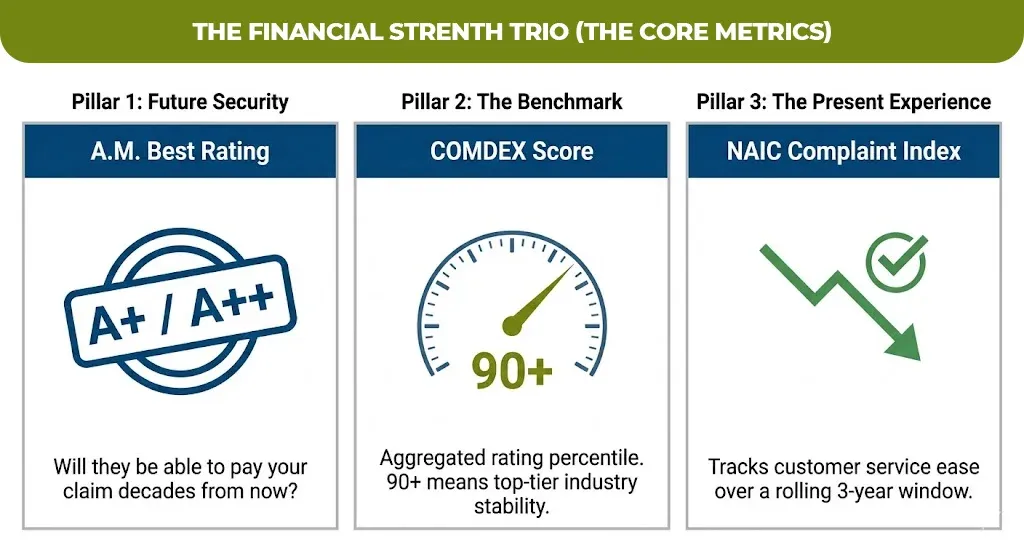

An A.M. The best rating tells you whether the company will be financially able to pay your family’s claim decades from now. A complaint index from the NAIC tells you whether the company is easy to deal with today.

You need both.

The top life insurance companies carry A+ or A+ plus ratings from a M best and they have fewer than the expected number of complaints to the state regulators over a three years rolling period.

A COMDEX score, which aggregates ratings from all four major agencies into a single percentile, is the fastest way to compare financial strength across companies. A COMDEX score above 90 places a company in the top tier of all rated insurers. For long-term financial strategies like retirement income planning, sticking with carriers rated A- or higher by A.M. Best with COMDEX scores of 90 or above is strongly recommended by independent advisors.

For basic term life coverage, anything with an A- or higher from A.M. Best is generally sufficient. The risk of underinsurance is almost never about financial strength at this level. It is about choosing the wrong policy type.

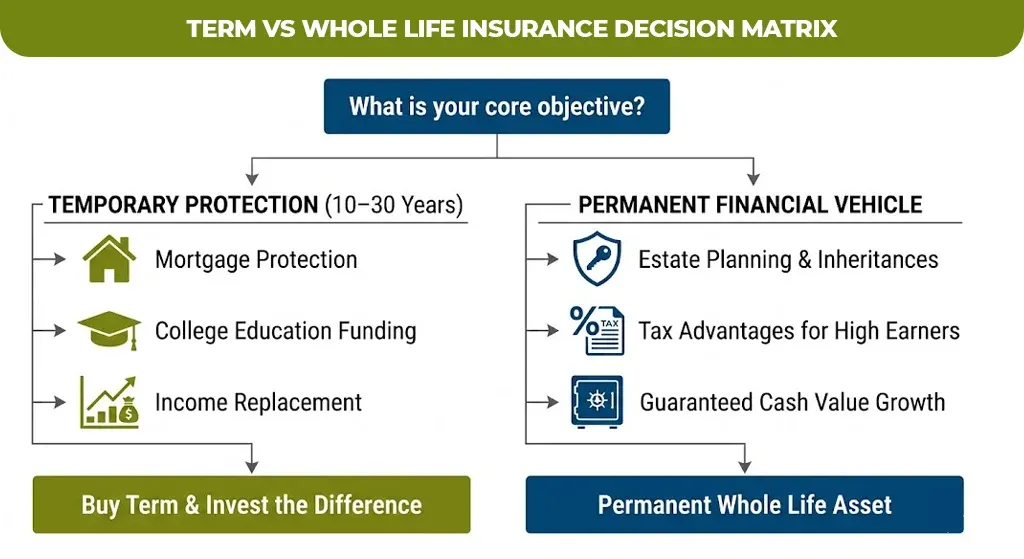

Term vs. Whole Life: Which Should You Actually Buy?

Most people should start with term life. Term life is typically the cheapest option, especially if you are young and healthy, and NerdWallet’s advice for most families in 2026 is to buy term and invest the difference rather than defaulting to a permanent policy.

Whole life insurance makes sense in the specific situations like if you want a financial vehicle that will build the guaranteed cash value, you need permanent coverage for the estate planning purposes or you are in a high income bracket with the tax advantages for the cash value accumulation are meaningful.

The mistake most people make is buying whole life because a salesperson told them it was an investment. It is a financial tool. Whether it is the right tool depends entirely on your situation, not on the commission structure of whoever is selling it.

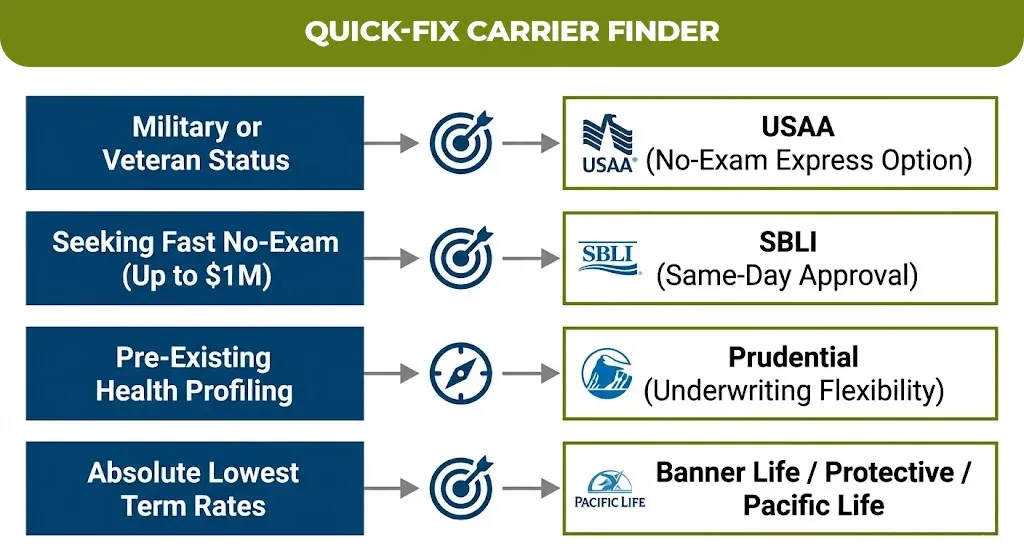

How to Find the Best Company for Life Insurance: A Quick Decision Framework

Before you request a single quote, answer these four questions:

- How long do you need coverage? If you need it for 10 to 30 years to cover a mortgage, income replacement, or children’s education, term life is almost always the right answer.

- What is your health profile? Healthy applicants get the best rates from companies like Banner Life and Protective. If you have diabetes, heart disease, or a recent health event, Prudential’s underwriting flexibility makes them the better starting point.

- Do you need coverage without a medical exam? SBLI offers genuine no-exam coverage up to $1 million with same-day approval and pricing that competes with fully underwritten policies.

- Are you a veteran or active military? USAA is the clear answer. Their Eagle Express term policy offers same-day coverage without a medical exam for applicants between 18 and 70.

If none of the above applies and you are simply looking for the lowest rate for clean-health term coverage, get quotes from at least three of these: Banner Life, Protective, Pacific Life, and SBLI. Then choose based on rate and any riders that matter to your situation.

One More Thing Worth Knowing in 2026

Individual life insurance premiums reached a record $17.5 billion in 2025, yet roughly 40% of U.S. adults say they need more life insurance than they currently have.

The protection gap is wide. Most people who have life insurance are underinsured, and most people who are shopping are comparing the wrong things. Brand recognition, website design, and agent likability are not metrics. Financial strength, complaint ratios, and actual premium for your health profile are.

Compare before you commit. The companies on this list are all legitimate, financially sound providers. The best one for you is the one whose policy fits your life, not the one with the most recognizable name.

Looking for Help Navigating Your Life Insurance Options?

If you want to compare policies across multiple carriers without the pressure of a sales call, mLife Insurance helps individuals review coverage options based on their actual needs and health profile.

You can explore your options at mLife Insurance and see what policies look like for your specific situation, with no obligation to buy.

This guide gives you everything you need to make an informed decision on your own. If you want a second set of eyes on what you find, that resource is there when you are ready.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.