You are self employed and staring at health insurance options that range from $278 a month to over $1,300 a month. You do not know if you qualify for subsidies, you are not sure which plan tier actually makes sense, and you suspect you might be leaving a significant tax deduction on the table.

That last part is almost certainly true. Health insurance for self employed individuals comes with a tax break that most freelancers and contractors either claim incorrectly or miss entirely and it can reduce your taxable income by thousands of dollars per year.

This article gives you the clear answer. No filler, no vague comparisons. Just what you need to choose the right plan, know the real cost, and protect yourself financially in 2026.

What Are The Best Health Insurance Plans For Self Employed In 2026?

The best health insurance for the self employed individuals in 2026 totally depends on one thing before anything else and it is whether you qualify for income based subsidies through the ACA marketplace.

If your annual income falls in between $15,960 and $63,840, then the marketplace add HealthCare.gov is almost certain by starting point. The premi tax credit at this income can range automatically reduce what you pay each month.

If your income is above this threshold and the private PPO plans and of exchange options will be offering better flexibility and network access, and sometimes at 40 to 60% less per month then the unsubsidized marketplace plan.

Here are the four main options available to self-employed workers in 2026

ACA Marketplace Plans

ACA Marketplace Plans are available at HealthCare.gov during the open enrollment that is starting from November one to January 15. These offers that guarantee coverage regardless of the medical history and these are the only plans that qualify for the premium tax credits and cost trading reductions.

Private Off-Exchange Plans

Private Off Exchange Plans from the companies like Blue Cross Blue Shield, Aetna, UnitedHealthcare, and Cigna allow the year round enrollment. No subsidy eligibility, but the stronger networks and more carrier options in many states.

Health Savings Account (HSA)

The healthcare saving accounts HSA plans that you contribute pretax dollars to cover the medical expenses. For the year 2026, all the marketplace bronze and catastrophic plans now qualify as high deductible health plans HDHP’s and making them HSA eligible.

Medicaid

Medicaid applies if your income falls below the federal poverty level. Eligibility and coverage vary by state.

How Much Does Health Insurance Cost for Self Employed Workers in 2026?

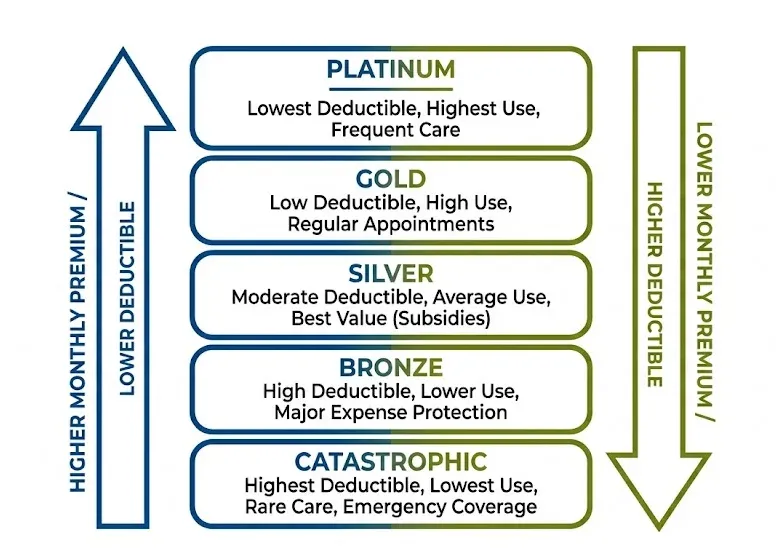

The monthly cost for health insurance for self employed is not fixed as it totally depends on your age, location, plan tier, and whether you receive subsidies. Below are the average unsubsidized monthly premiums for a 40 year old in 2026:

2026 ACA Marketplace Plan Costs (40-Year-Old, Unsubsidized)

| Plan Tier | Avg. Monthly Premium | Avg. Deductible | Best For |

| Catastrophic | $278 | $9,450+ | Young, healthy, rarely use care |

| Bronze | $350 – $420 | $7,500 – $9,000 | Low monthly cost, HSA-eligible |

| Silver | $540 | $3,000 – $5,000 | Subsidy-eligible workers (best value) |

| Gold | $718 | $1,057 – $2,500 | Moderate-to-high healthcare users |

| Platinum | $1,384 | $0 – $500 | Frequent healthcare needs |

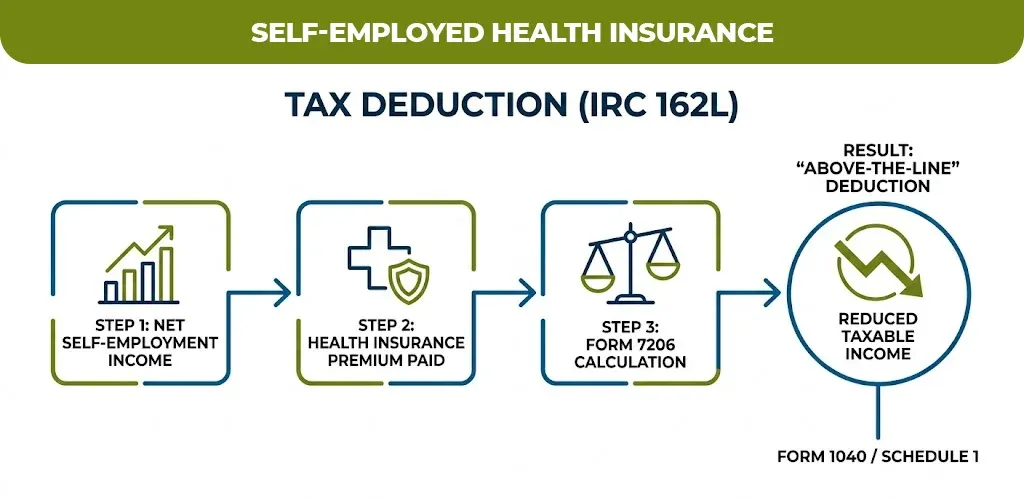

Is Health Insurance For Self Employed Is Tax Deductible

Yes and this is the protection that most of the self-employed people either under use or calculate incorrectly.

The IRS allows an above the line deduction for the health insurance premium and IRC section 162 I it means that you reduce your taxable income directly without itemizing. The reduction applies to the premium you pay for yourself, your spouse and your dependents.

According to IRS Form 7206, which is now the required form to calculate this deduction, the key rules are:

You must have net self-employment income. The deduction cannot exceed what your business actually earned. If your net profit is $40,000 and your annual premiums are $8,000, you can deduct the full $8,000.

You must not have been eligible for employer-sponsored coverage during the months you are claiming. Eligibility is calculated month by month. If you had access to a spouse’s employer plan for three months, you lose the deduction for those three months only.

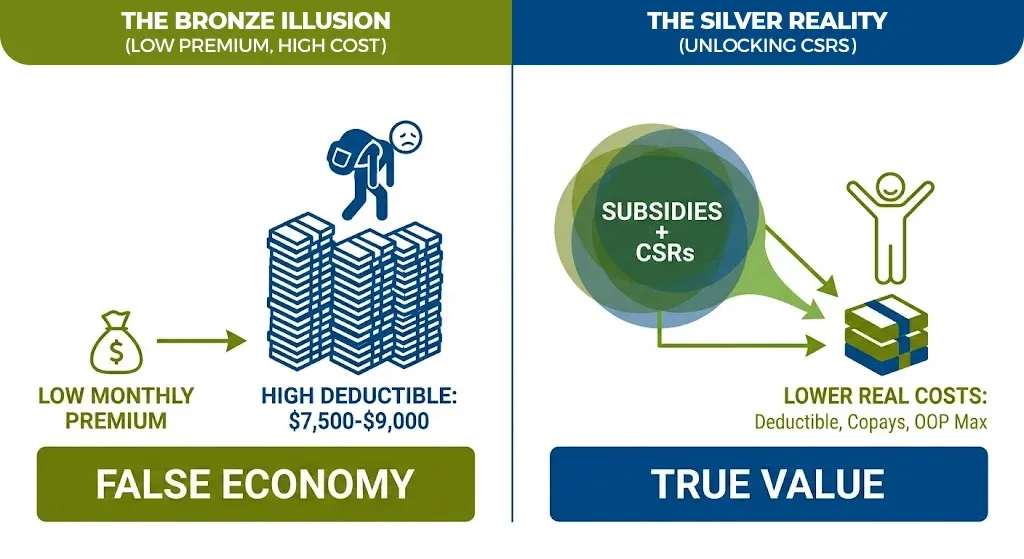

The Silver Plan Rule That Most Self Employed Workers Do Not Know

If you qualify for subsidies, Silver plans are the only tier that unlocks cost-sharing reductions (CSRs). This is not widely understood and it is where most people leave money behind.

The cost sharing deductions will lower your actual deductibles, your co-pay and out-of-pocket maximum is not just the monthly premium. A silver plan with CSR can look like a cold plan in the real world uses, at a standard plan price once subsidies are applied.

On the other hand the bronze plant look cheaper monthly but come with the deductibles that are between $7500-$9000. Most of the self-employed people who pick bronze because it seems affordable end up paying for more than when they actually need care. The silver plan at $540 per month unsubsidized, we reduced to $200-$300 monthly with the subsidies that is often outer prawns on the total annual spend.

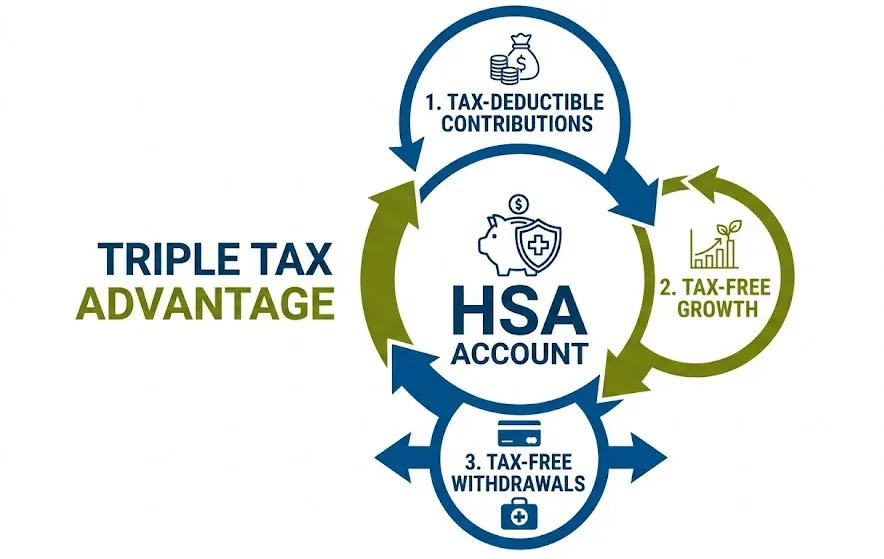

HSA Contribution Limits for 2026: Stack Your Tax Savings

If you choose a bronze or catastrophic plan that is all now as eligible in 2026, paying it with the health savings account is one of the most smartest financial move that is available to self-employed workers.

For 2026, the IRS allows H essay contributions of $4400 for the individual coverage and $8750 for the family coverage under a high deductible health plan. The contributions and the tax deductibles, growth tax and withdrawals for qualified medical expenses are also text me. This is a triple tax advantage on the funds you would spend on healthcare anyway.

The contribution deadline for the 2026 tax year is April 15, 2027, so you can contribute retroactively even after year end if you have an eligible plan.

How To Choose The Right Health Insurance For Self Employed Plan Without Overpaying

Three questions narrow it down fast.

Do you qualify for subsidies? Check your income against the 2026 federal poverty level thresholds at HealthCare.gov. If yes, start with the Marketplace and compare Silver plans first.

How often do you actually use healthcare? If you are generally healthy and rarely see a doctor, a Bronze plan paired with an HSA may cost you less total annually even with the higher deductible. If you take ongoing medications or have regular appointments, Gold tier or a subsidized Silver plan typically wins.

Is flexibility more important than price? If you want year-round enrollment, access to out-of-state providers, or specific specialist networks, a private off-exchange PPO may serve you better than an ACA-only HMO network.

A Note for Anyone Still Figuring This Out

If you are self-employed and still sorting through your options, you are not behind. Health insurance is genuinely complex for independent workers, and most of the generic advice online either oversimplifies the subsidy math or ignores the tax interaction entirely.

At mlife Insurance, we work with the self employed individuals and small business owners who want clear, personalized guidance, not a generic quote form. If you are trying to compare the plans, understand your subsidy eligibility, or figure out how the deduction applies to your specific situation, mlifeinsurance.com is worth a look.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.