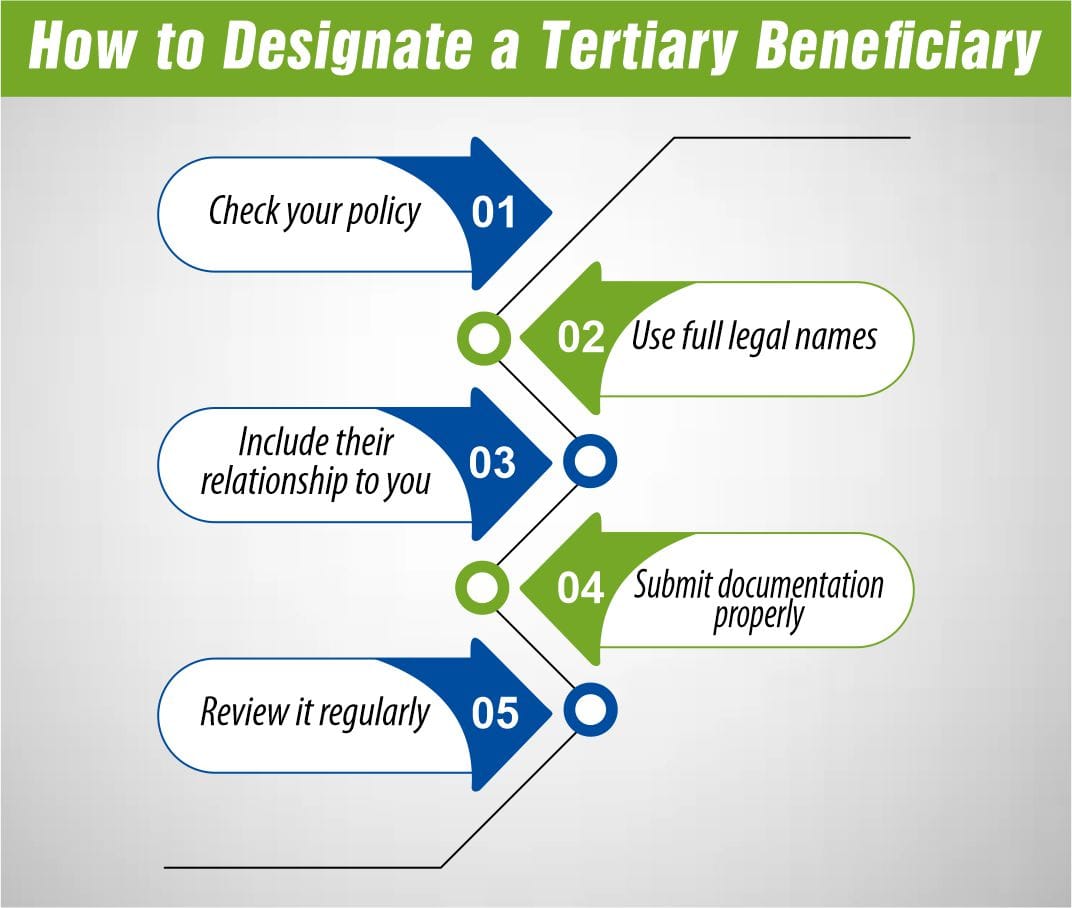

How to Designate a Tertiary Beneficiary

Designating a tertiary beneficiary is simple but important. Here’s how to do it right:

- Check your policy: Some forms allow space for tertiary designations, others may require a written request.

- Use full legal names: Avoid using nicknames or vague labels like “my cousin.”

- Include their relationship to you: This helps avoid confusion.

- Submit documentation properly: Ensure it’s filed with your insurer or estate planner.

Review it regularly: Keep it current as your life and relationships change.

Tertiary Beneficiary in Estate Planning

In estate planning, a tertiary beneficiary can help keep your estate out of probate court. If both your primary and contingent beneficiaries are unavailable and there’s no tertiary, your estate could face delays, legal fees, and unintended distributions. Tertiary designations are especially useful in large or blended families, or when your beneficiaries are elderly or have health concerns.

Tertiary Beneficiary Trusts

Instead of naming a person, you can list a trust as your tertiary beneficiary. This is especially helpful if your desired recipient is a minor, has special needs, or struggles with money management. A trust can hold and manage the assets according to your instructions—like limiting withdrawals or requiring funds to be used for education. This gives you greater control over how your legacy is handled.

Tertiary Beneficiary in a Will: What You Need to Know

Just like insurance policies, wills can include tertiary beneficiaries. This can provide an additional safety net for asset distribution. However, remember:

- Wills go through probate, which can delay things.

- Language matters—be specific and use legally accepted terms.

- It’s best to consult an estate attorney to ensure your will is enforceable and reflects your exact wishes.

Contingent vs. Tertiary Beneficiary: Which One Should You Choose?

You shouldn’t have to choose one over the other—include both if your policy or plan allows. The contingent beneficiary is more likely to receive the benefit, but the tertiary provides an added level of protection. Always select people you trust, who are capable of handling financial responsibilities, and who understand your goals. This is particularly crucial in high-value estates or situations with potential family conflict.

Tertiary Beneficiary Designation by State

Every U.S. state has different rules around beneficiary designations and estate planning. For example:

- Community property states (like California and Texas) may automatically allocate assets to a spouse unless otherwise specified.

- Some states give preference to children if no beneficiaries are named.

- Probate processes vary by jurisdiction.

By naming a tertiary beneficiary, you reduce the risk of these default rules overriding your intentions. Always work with a local estate planning expert to comply with state laws.

When to Review or Update Your Tertiary Beneficiary

Life doesn’t stay the same—and neither should your estate plan. You should review and update your beneficiary designations:

- After marriage or divorce

- When a child is born or adopted

- Following a death in the family

- After a major financial or health change

Set a reminder to review your entire estate plan at least once a year. Keeping your documents up to date ensures your assets always go where you want them to.

Conclusion: Why Naming a Tertiary Beneficiary Matters

Naming a tertiary beneficiary isn’t just a technicality—it’s a smart way to protect your legacy. It ensures that even if your primary and contingent beneficiaries can’t receive your assets, your backup plan stays intact. Whether you’re managing a simple policy or a complex estate, this third designation gives your loved ones clarity and reduces the chances of legal delays. The best estate plans prepare for every possibility—and that’s exactly what a tertiary beneficiary helps you do.

Final Tip: Work with a qualified estate planner or insurance advisor to make sure all your beneficiary designations are up-to-date, clearly documented, and legally sound.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.