You are shopping for an IMO and every organization you find claims to offer the best commissions, the most carrier access, and the strongest support. They all sound identical. You sign with one based on a recommendation from a colleague. Three months later, you realize the commission grid was lower than advertised, the support team is hard to reach, and you have no idea how to switch.

This happens constantly. The IMO insurance space is full of organizations that look solid on the surface and underdeliver once you are contracted. Choosing the wrong one does not just cost you a few percentage points. It shapes your entire sales operation, your client relationships, and your income ceiling.

Here is everything you need to make a confident, informed decision.

What Is IMO Insurance, and What Does It Actually Do for Agents?

An IMO, or independent marketing organization is the company that is sitting between the insurance carriers and the independent agents. The company negotiate the contract with multiple insurance companies then offer those contact to the agent along with the training, marketing tools, back Office support and often generation assistance.

The IMO insurance meeting is very simple than it sounds, and that is think of it as a whole seller for potential insurance distribution. Instead of an agent contracting directly with each company one at the time, the IMO bundles access two dozen of the insurance companies under one trailer. That saves agent months of paperwork and often unlocked the pet commission rates then they could negotiate on their own.

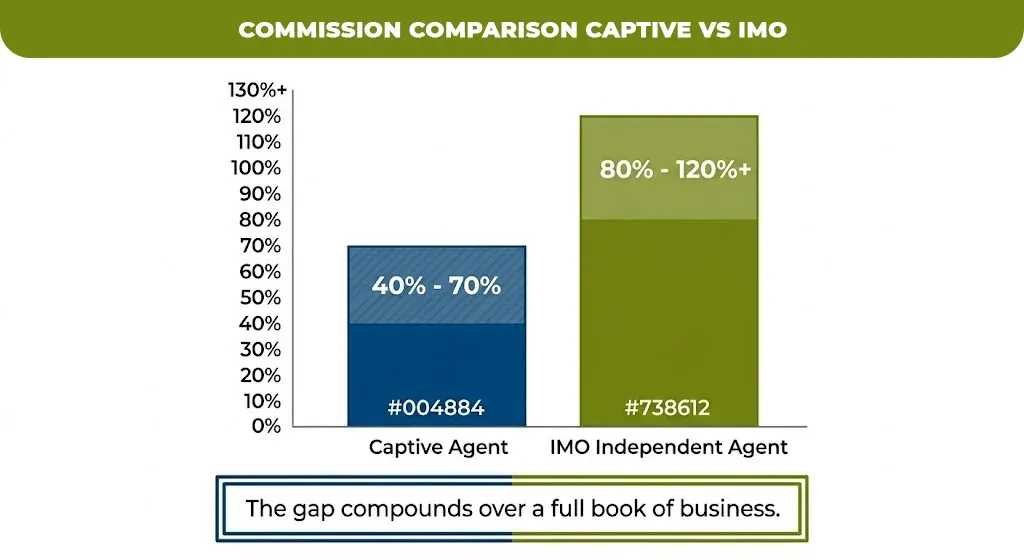

According to Redbird Agents’ 2026 commission analysis, independent agents working through a quality IMO typically access commissions ranging from 80% to 120% of first-year premium on life products, compared to 40–70% for captive agents tied to a single carrier. That gap compounds significantly over a full book of business.

IMO Insurance vs. FMO vs. Captive Agent: Which Structure Pays and Supports You Best?

This is the comparison most agents get wrong because the labels matter less than the actual contract terms. IMO and FMO are often used interchangeably. The meaningful distinction is between working through any marketing organization versus going captive or direct.

Here is how the three models compare in practice:

| Factor | Captive Agent | Direct Carrier Contract | IMO / FMO |

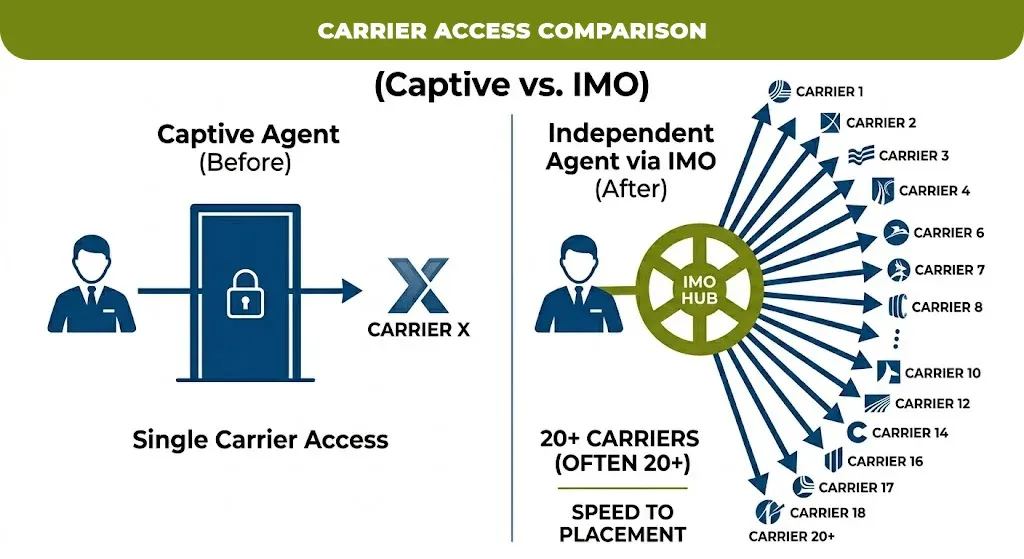

| Carrier access | One carrier | One or two | Multiple (often 20+) |

| First-year commission | 40–70% | Moderate, unenhanced | 80–120%+ |

| Training and support | Company-provided | Minimal | Varies by IMO |

| Lead generation | Sometimes provided | Rarely | Often available |

| Flexibility to switch carriers | None | Limited | High |

| Override taken by middleman | None | None | 1–3 points typical |

According to Brokers Fidelity’s 2026 FMO vs IMO guide, IMOs typically take a 1–3 point commission override while FMOs often take 2–5 points. Many agents never see these grids until after signing, which is why transparency is one of the most important things to ask about upfront.

The captive model offers stability for brand-new agents. But for anyone building an independent book of business, contracting through an IMO delivers far more flexibility and earning potential at scale.

What the Best IMO Insurance for Life Insurance Actually Provides

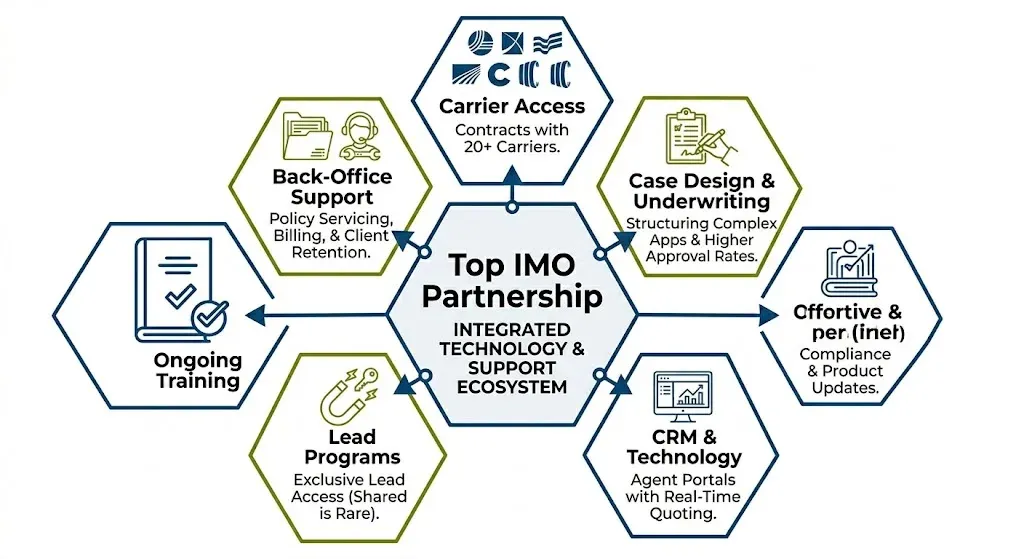

Commission rates are the entry point, not the whole picture. The best IMO for life insurance does several things that directly affect your day-to-day sales operation.

Carrier access and contracting speed

Top IMOs maintain active contracts with 20 or more carriers. When a client needs a specific product, you should be able to place it within days, not weeks. Slow onboarding with carriers is a sign of a poorly organized IMO back office.

Case design and underwriting support

This is where newer agents leave money on the table. A strong IMO assigns case specialists who help structure complex applications, navigate underwriting quirks, and increase approval rates. That support directly affects placed business and client satisfaction.

Technology and CRM tools

According to DMI Marketing’s breakdown of life insurance IMOs, modern IMOs now offer agent portals with real-time quoting, CRM access, and marketing templates. Agents using these tools spend less time on administration and more time in front of clients.

Training and compliance

Carrier products change. Regulations shift. An IMO that invests in ongoing agent education keeps you compliant and competitive without requiring you to track every update yourself.

Lead programs

Not every IMO offers leads, but many do. Evaluate whether the program is shared (five agents calling the same prospect) or exclusive. Shared leads are rarely worth the cost.

Top IMO Insurance Companies Worth Knowing in 2026

This is not an exhaustive ranking, and that right fit totally depends on your product focus, experience level, and if your primarily cell life, health, Medicare or NVT products. That’s it, these organization consistently comes up with the experience agent that I discussed who deliver on their promise.

| IMO | Primary Focus | Known For |

| Integrity Marketing Group | Life, Medicare, annuities | Largest IMO by scale, extensive carrier network |

| AmeriLife | Life, health, Medicare | National reach, strong agent training and mentorship |

| Family First Life (FFL) | Life insurance, final expense | Agent-friendly commissions, mortgage protection focus |

| The Marketing Alliance | Life, annuities | Training programs, personalized agent support |

| Agent Pipeline | Medicare, final expense, health | Compliance support, Medicare Advantage specialization |

Integrity Marketing Group has grown rapidly through acquisitions, now controlling a significant portion of IMO distribution in the United States. That scale brings carrier leverage and technology resources, but some agents report the support experience becoming less personal as the organization has grown.

AmeriLife and Family First Life remain popular with agents who prioritize mentorship and commission transparency over raw organizational size.

The honest answer about IMO insurance companies is this: the largest IMO insurance organizations have the most resources, but a mid-sized IMO with genuine agent focus can deliver a better day-to-day experience for producers who are not yet generating high enough volume to move the needle at the national level.

How IMO Insurance Connects to Broader Sales Operations

Most conversations about IMOs focus only on commission rates and carrier access. The less-discussed value is what a strong IMO does for the entire sales operation behind an agent or agency.

Customer service and client retention are significantly easier when your IMO provides back-office support that handles policy changes, billing questions, and reinstatement requests without pulling you out of sales mode. For agents running a one-person shop, that operational support is the difference between scaling and staying stuck.

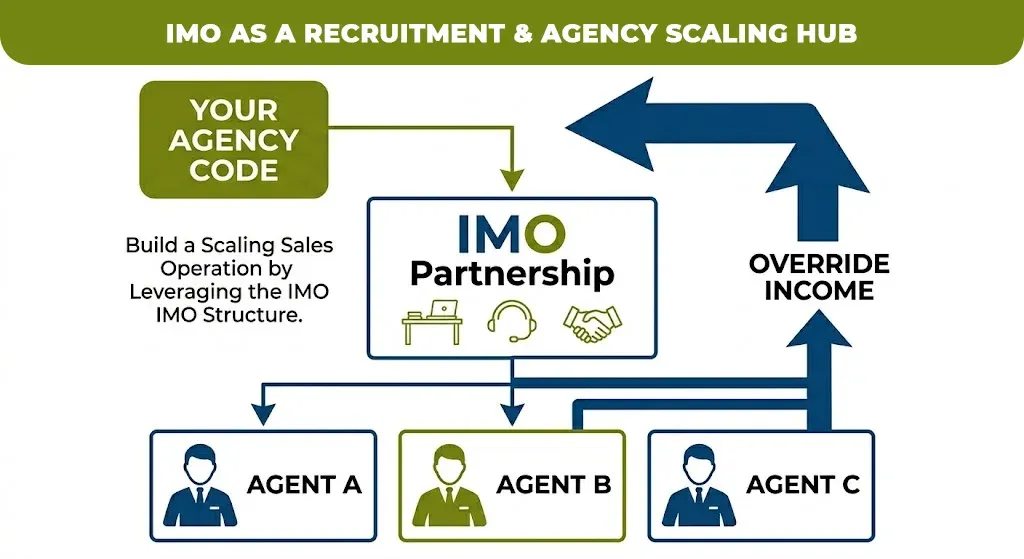

For agencies and downlines, the IMO also functions as a distribution engine. When you recruit sub-agents, the IMO structure allows them to contract under your agency code, creating override income as your team grows. This is how the largest independent agencies are built, not by writing every policy themselves, but by building teams under a well-structured IMO arrangement.

The 2026 BPO call center guide from MyCustomer360 notes that outsourced sales support functions, including inbound lead handling and policy servicing, are increasingly integrated into how insurance agencies manage their back office. Agents who combine a strong IMO relationship with dedicated sales support infrastructure consistently outperform those trying to manage everything alone.

How to Choose the Right IMO Insurance: 6 Questions That Matter

Most agents ask the wrong questions when evaluating an IMO. Here are the six that actually separate a good partnership from a frustrating one.

What is the actual commission grid for my primary product?

Ask for it in writing before signing anything. A verbal promise means nothing once you are contracted.

Which carriers can I access on day one?

Some IMOs require a production ramp before unlocking their full carrier shelf. Know exactly what you are starting with.

What does the release process look like?

If you want to leave, how long does it take and what are the conditions? A difficult release process is a red flag before you even sign.

What does back-office support include?

Ask specifically about case design, underwriting assistance, and policy change handling. Vague answers mean minimal support.

Do you offer leads, and are they exclusive?

If yes, ask for the cost per lead and the average conversion rate agents in your product line are seeing.

What does onboarding with a new carrier actually take?

Some IMOs can get you contracted and appointed within a week. Others take six to eight weeks. That timeline affects your cash flow.

Thinking About How Your IMO Insurance Fits into a Bigger Picture?

If you are an agent or agency owner trying to figure out whether your current IMO setup is holding you back, or if you are exploring how to build a more scalable sales operation, the IMO relationship is just one piece of the puzzle.

The agents and teams growing fastest right now are combining strong IMO contracts with dedicated sales support, structured lead follow-up, and back-office processes that do not depend entirely on the producer. If you are curious about what that looks like in practice, Mlife Insurance has resources built specifically for agents at that stage of growth.

No pressure to change anything. Sometimes just seeing how others have structured their operation is enough to spot where yours can improve.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.