You see a $10,000 whole life policy advertised as affordable, sign up without comparing it to anything else, and later realize it may not cover what you actually needed it for. That’s the most common mistake with small face-amount policies: buying based on the round number instead of the real math behind it.

A $10,000 whole life insurance policy generally cost between $20 and $90 per month depending on your age, your health and also your gender. It also builds cash value slowly over the life of the policy. No matter what, the right amount of coverage depends entirely on what you are trying to protect against.

How Much Does $10000 Whole Life Insurance Cost?

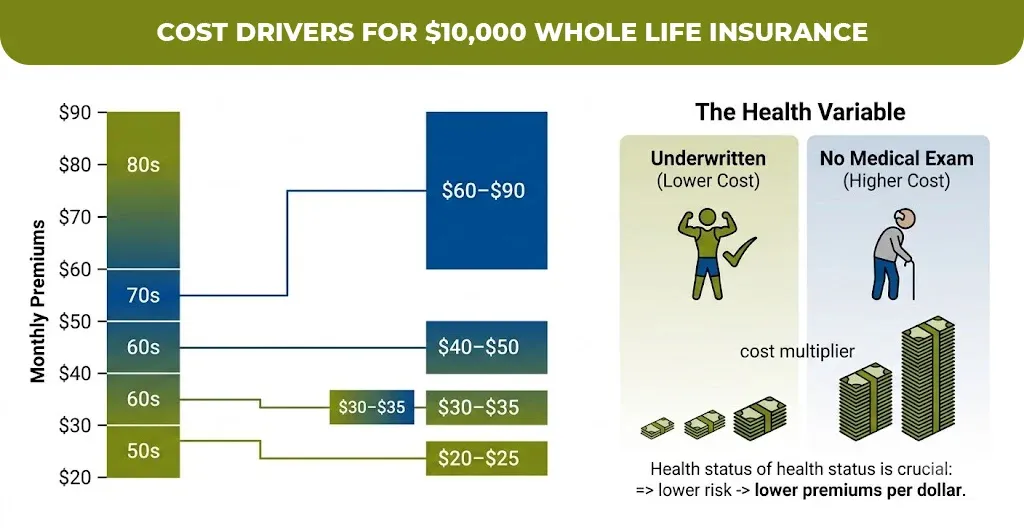

A $10,000 whole life insurance can cause strange stuff from $20-$40 per month for someone in their 50s in good health. It climbed two50 to 90 $ per month for someone in their 70s or in their 80s. These figures scale down from standard $100,000 industry pricing data, since a $10,000 policy is 1/10 the coverage amount that is used in most of the published rate charts.

Health status changes this more than almost any other factor at this coverage size. A senior using a no-medical-exam option will generally pay more per dollar of coverage than someone who qualifies for fully underwritten pricing, since the insurer is taking on more uncertainty without a health screening.

| Age | Monthly Cost ($10,000 coverage, healthy nonsmoker) |

| 50 | $20 to $25 |

| 60 | $30 to $35 |

| 70 | $40 to $50 |

| 80 | $60 to $90 |

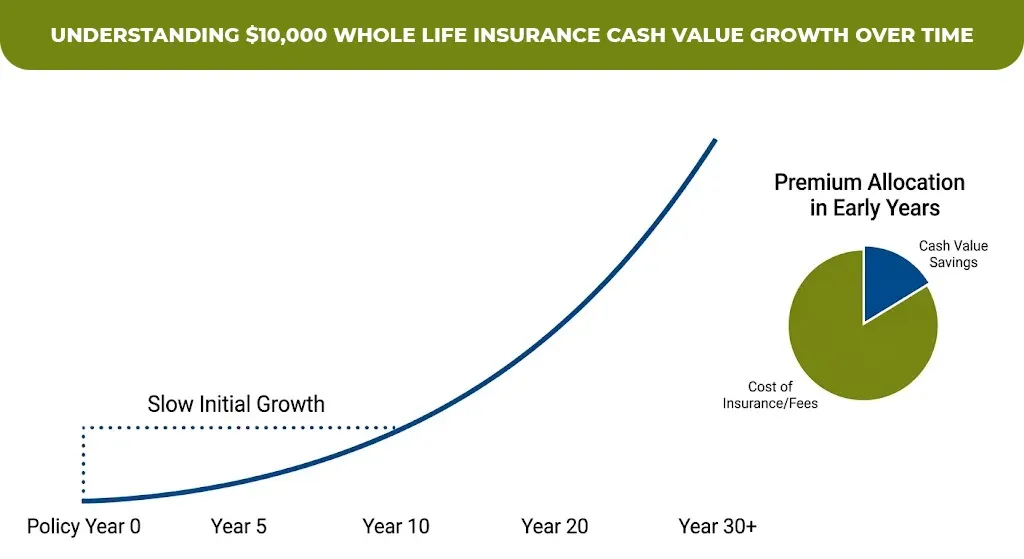

What Does $10000 Whole Life Insurance Cash Value Look Like Over Time?

$10000 Whole Life Insurance cash value your bills slowly in the early years and it will go up the longer the policy stays active. It generally reaching a meaningful amount only after 10 to 20 years of the premium payment. In the first few years, the cash value is often minimal, since a large share of your premium goes towards the cost of insurance and administrative fees rather than savings.

This is normal and it is not sign of a bad policy. Whole life insurance is specially designed for the cash value to grow slowly over the decades, not function like a saving account with fast and early returns.

Would a $10,000 Term Policy Be Cheaper Than Whole Life?

The $10,000 term life insurance policy generally cost less per month as compared to the whole life insurance policy. But this plan expires at the end of the term and builds no cash value. For someone specifically who want lifelong coverage that never need renewing, whole life remain the better fit despite of the higher price. Since term life coverage at this size becomes far more expensive or unavailable entirely once you have passed your 70s or 80s.

The tradeoff is straightforward once you see it side by side. Term life makes sense if you only need coverage for a defined number of years, such as until a specific debt is paid off, while whole life makes sense if the goal is guaranteed coverage that lasts as long as you do, regardless of when that is.

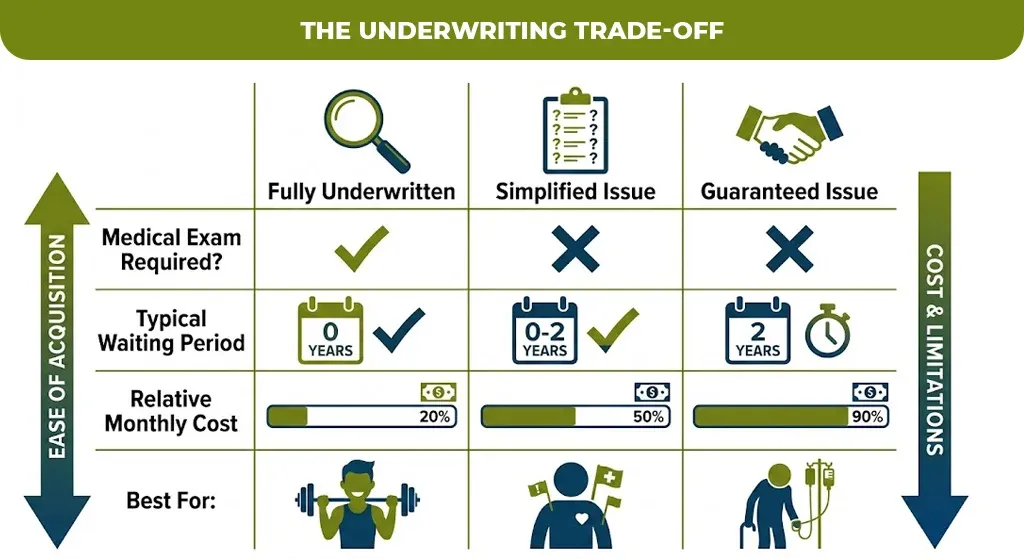

Is $10000 Whole Life Insurance No Medical a Good Option?

$10,000 no medical whole life insurance policy can be a reasonable choice for the seniors who have health conditions that would otherwise disqualify them from the regular underwriting. But it usually cost more per dollar of coverage than a fully underwritten policy. The guaranteed version of this coverage generally apply a two year wedding. It means that if the policyholder passes away within the first two years then the beneficiaries usually receive only the premium paid backs, plus modest interest rather than the full death benefit.

This waiting period catches people off guard more than any other detail in this category. If a buyer’s health would qualify them for a simplified issue policy instead of guaranteed issue, that route is almost always worth checking first, since it can mean a lower price and no waiting period.

| Policy Type | Medical Exam Required? | Waiting Period | Waiting Period |

| Fully underwritten | Yes | None | Lowest |

| Simplified issue | No (health questions only) | Usually none | Moderate |

| Guaranteed issue | No | Often 2 years | Highest |

Is $10,000 Whole Life Insurance Enough Coverage for Seniors?

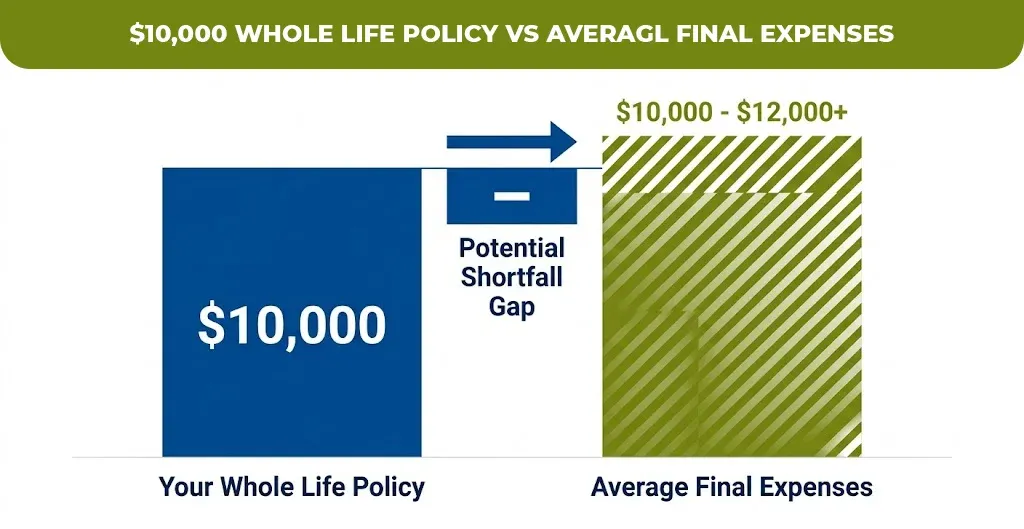

For seniors specifically planning around the final expenses, $10,000 policy in whole life insurance often false short for covering a full funeral and burial. Since the average funeral cost in the recent years have run closer to $10,000-$12,000 nationally. A $10,000 policy can still meaningfully reduce the financial burden on the family, just not necessarily eliminated entirely.

This gap is worth knowing before buying, not after. If covering the full cost of final expenses is the specific goal, running the math against current local funeral pricing before choosing a face amount avoids a shortfall your family discovers at the worst possible time.

How Do You Compare Real Quotes Instead of Guessing?

Comparing the real quotes from at least two or three insurance companies at the same coverage amount and underwriting type is the only reliable way to know if $10,000 in coverage is priced fairly for your situation. Searching for the specific insurance companies rate, such as how much $10,000 whole life insurance cost with the state farm, will only return an accurate number through a direct code, since published rate charts rarely reflect any single companies actual underwriting.

Asking each insurance company the same three questions, your exact health classification, whether the policy is a simplified or guaranteed issue, and the length of any waiting period, and this will make quotes genuinely comparable instead of three different apples being measured against each other.

What Happens to the Cash Value If You Need to Access It Early?

You can typically borrow against the cash value or withdraw up to a amount of premium you have paid without earning the taxes. But the amount beyond that can be taxed as income.

According to IRS guidance for senior taxpayers, if you surrender a life insurance policy for cash, you must include in income any proceeds that exceed the total cost of the policy, meaning only the gain above what you’ve paid in is taxable, not the full surrender amount.

This distinction matters because many people assume any withdrawal from a life insurance policy is tax-free, which isn’t accurate once you exceed your own premium contributions. Confirming this with the insurer or a tax professional before taking a withdrawal avoids an unexpected tax bill later.

A $10,000 whole life policy can be exactly the right size for some families and not quite enough for others, and the only way to know is comparing your real numbers against your real goal. For more on figuring out the coverage amount that actually fits your situation, see our guide to choosing the right life insurance coverage amount. When you’re ready to see where you land, Mlife Insurance can walk you through your real options, with no pressure to decide today.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.