When planning for your financial future, it’s common to hear about two important options: the conservative portfolio of permanent life insurance and a Roth IRA. They are important sources for attaining financial security with some differences between them. Knowledge of these differences can assist in decision-making regarding future objectives to achieve your financial potential. Today, I would like to share with you a few major differences between permanent life insurance and a Roth IRA, so you will be able to make your choice.

What is Permanent Life Insurance?

This one here is called permanent life insurance because of the provisions that guarantee a death benefit without fail regardless of when it may occur to the insured, provided that premiums are being made continually. Term life insurance duration is predetermined while a permanent life insurance policy will cover you throughout your lifetime.

Key Features of Permanent Life Insurance:

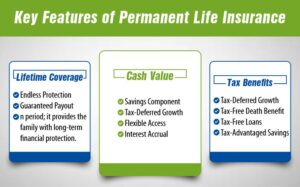

– Lifetime Coverage

- Endless Protection: While term policies end ona specific date, permanent life insurance coverage lasts for the entire lifespan of the policyholder provided he pays premiums.

- Guaranteed Payout: This policy promises to pay out a lump sum to the beneficiaries when you die, thus protecting your loved ones should that event happen at any time.

- Peace of Mind: This means you do not have to fret over a policy expiring after a given period; it provides the family with long-term financial protection.

– Cash Value

- Savings Component: Concerning the policy, a part of the premiums paid is contributed to the cash value, which is a saving or investment-like account.

- Tax-Deferred Growth: It continues to earn interest year after year and you will not be taxed on your investment until you decide to withdraw the money that is held by the company to grow your cash value.

- Flexible Access: Policy loans or withdrawals are available to you to use the cash value for any emergencies or to meet your financial needs throughout the policy.

- Interest Accrual: Such cash value may earn interest, dividends, and investment returns depending on the type of policy,y and in the process, the policy grows.

– Tax Benefits

- Tax-Deferred Growth: The cash value component has tax advantages; that is, the earnings won’t attract taxes if they are kept inside the policy.

- Tax-Free Death Benefit: The monies paid to the beneficiaries as death benefits, are often exempted from income tax, an aspect that is very encouraging when the need arises.

- Tax-Free Loans: And policy loans that are borrowed against the cash value of the insurance policy are generally tax-free which allows you to access funds freely without penalty of taxes being levied.

- Tax-Advantaged Savings: To the same effect, the policy has the advantage of growing wealth without taxes on such an increase making it an ideal long-term savings plan.

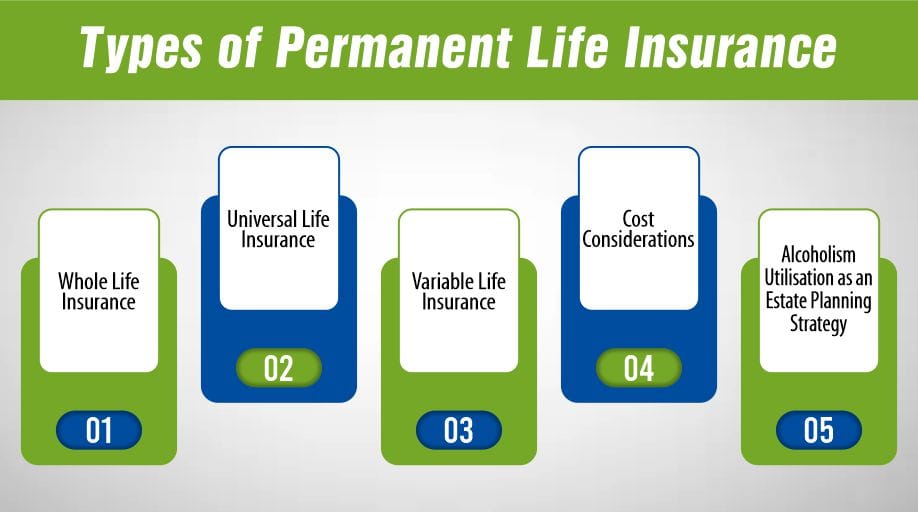

Types of Permanent Life Insurance

Whole Life Insurance:

- Fixed Premiums: The cost of premiums depends on the type of policy to be paid all the same period the policy exists.

- Guaranteed Cash Value: It provides for a guaranteed cash value growth and death benefit to the person who owns the policy.

- Predictability and Stability: This suits the clients who want to have a constant uninterrupted signal to provide a stable connection.

Universal Life Insurance:

- Flexible Premiums: It allows flexibility in that premium payments as well as the amount of the death benefit can also be changed over some time.

- Flexible Cash Value: It saves cash value at a minimum interest rate, and you may be allowed to invest the cash values in different accounts.

- Adaptable: Recommended for those who wish to have control over the patterns in which their coverage and cash value progress.

Variable Life Insurance:

- Investment Options: The policy enables you to direct the cash value’s investment to securities like shares, bonds, or mutual funds.

- Variable Death Benefit: The death benefit as well as cash value is flexible and may rise (or fall) depending on the performance of the invested sum.

- Risk and Reward: This type of account is ideal for those people who understand more risks inherent in investments and those who are willing to take them in return for the probability of achieving higher yields.

Additional Features and Benefits

- Loan Options: The cash value can be used to secure loans and these normally attract less interest than a personal loan or credit card.

- Accelerated Death Benefit Riders: Some policies provide options to the rider that allow the death benefit to be consumed early if you have a terminal disease.

- Living Benefits: The policies may have living assurance riders under which the client can receive a section of the full amount of death benefits for the medical expenses and or expenses of long-term care if required.

- Dividends: There are contractual permanent life insurance policies that are linked to the performance of the business, such as whole life and thus can offer policyholders dividends. They can be used to lower premium rates, expand coverage, or be cashed.

Cost Considerations

- Higher Premiums: Some variations are more expensive than others due to the lifetime coverage and added present cash value options of permanent life insurance.

- Value Over Time: In the long run, though, you are likely to spend more money for comparable coverage if it is a temporary policy or if your coverage is limited to a specified age or time frame. The ability to collect cash value while living also offsets the high starting cost of an entire life policy.

Alcoholism: Utilisation as an Estate Planning Strategy

- Wealth Transfer: Whole life insurance is particularly important in estate planning because it allows the heirs to pass property to the beneficiaries without incurring taxes.

- Funding Trusts or Charities: Now, some people prefer to use the money as a death benefit, to fund a trust, or to make charitable contributions, which will allow them to receive certain tax deductions.

- Legacy Planning: It assists in the leaving of a legacy in as much as it offers your family a source of income and possibly helps to lower the taxes on the estate.

What is a Roth IRA?

It is an Individual Retirement Account that taxes its earnings differently so that the money withdrawn in retirement also does not attract taxes provided that certain conditions have been met. Unlike other retirement accounts where what is invested is determined after a tax is done on it, the Roth IRA is funded with money that has already been taxed. The main benefit of a Roth IRA is that distributions taken later in life can be made with no taxes owed on them.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.