Are you wondering how being diagnosed with dementia impacts your life insurance options? It’s a common concern about life insurance for dementia patients, and the answers might be simpler than you think. Whether you’re worried about higher costs or just finding a policy that fits your needs, there’s plenty to unpack. Let’s dive into what you need to know about securing life insurance if you or a loved one is facing dementia.

What is dementia?

Dementia results in a decrease or deterioration in the brain’s functional capabilities. Individuals with dementia often face challenges in several areas, including:

- Thinking processes

- Solving problems

- Logical reasoning

- Recalling memories

Communicating verbally about Alzheimer’s disease represents a particular form of dementia and is its most prevalent cause.

Does Legal & General life insurance cover dementia?

Yes, dementia is covered by Legal & General life insurance. You are insured if you had a policy with them before receiving a dementia diagnosis. You’ll be good to go as long as you remember to make your premium payments on time.

It’s more difficult for anyone seeking a new policy after being diagnosed with dementia. Coverage is conceivable, but conditions and expenses may vary. Depending on your circumstances, it’s a good idea to speak with Legal & General or an insurance broker directly to acquire the details. They can guide you through the choices to identify the ideal match. It’s always helpful to have a support system for life insurance for dementia patients.

Will a life insurance provider consider my family’s history of dementia?

Yes, a life insurance company may consider your circle of relatives records of dementia when you apply for a policy. It’s like when you tell a mechanic your vehicle’s been making a weird noise; they’ll take a closer look to figure out what’s up.

If dementia runs in your circle of relatives, insurers see it as a bit of a chance flag. They might ask you some questions about your family health history to get a clearer photo. This does not suggest you may not get insurance, but it would affect your costs or the kind of coverage they provide.

The nice technique is to open all of your relatives’ records from the beginning. This facilitates the insurance parents’ finding the best alternative for you—sort of like making sure you get the proper length shoes from the get-go!

What Types of Coverage Are Available for Dementia Patients?

Choosing a life insurance plan can be similar to exploring a new city without a guide when you or a loved one has dementia. To make it easier, let’s dissect it.

Guaranteed Issue Life Insurance

The good news is that having Alzheimer’s or dementia does not prevent you from being eligible for guaranteed issue life insurance. This kind of insurance allows anyone to enter, much like an open-door policy.

What is life insurance with guaranteed acceptance?

Guaranteed acceptance policies live up to their name; they are frequently referred to as no-questions life insurance. When you apply, no medical questions are asked—no tests, no physicals, nothing. It’s as simple as subscribing to a newsletter.

Who Are These Policies For?

These policies are designed specifically for folks with high-risk conditions like dementia. They’re a safety net, ensuring that you have some level of insurance coverage, even with a serious pre-existing condition. It’s like having a backup plan that’s ready to go, no matter what.

Can You Get Life Insurance if You Have Dementia?

It can be difficult to obtain life insurance for dementia patients, but it is still achievable. Imagine it like getting a ticket to a well-known film on opening day; it takes work, but you can pull it off.

It’s fantastic if you had life insurance before being diagnosed with dementia! That policy should remain in effect because it is your best bet.

It will be more difficult to find a new policy after a diagnosis. Insurance companies frequently consider dementia a high-risk condition. However, there are still some accessible choices. Medical exam-free policies might be more appropriate, but they might also cost more.

In short, it’s about shopping around. Think of it as trying to find a good pair of shoes on sale. It takes patience and a bit of luck, but it’s not impossible. And hey, having the right information and expectations can make all the difference. Keep your chin up, and don’t hesitate to ask for help from insurance experts about life insurance for dementia patients. They can often find something you might have missed!

Qualifying for Life Insurance for Seniors with Dementia

Getting life insurance for seniors with dementia may seem like a tricky puzzle, but it is definitely doable.

It all depends on the type of insurance.

How Much Does Life Isurance Cost?

The key is to look at the right settings. Guaranteed-issue life insurance is your best bet here. Think of it as a supermarket expressway—it’s designed to move through quickly and hassle-free.

How does Guaranteed Issue Life Insurance work?

This insurance does not ask for health information or require a medical exam. You apply, and you’re almost guaranteed to get it. It’s easy and stress-free. Imagine buying tickets to a concert where everyone gets seats, no questions asked.

Details in Keep in Mind

While guaranteed life insurance is easier to obtain, it tends to be more lucrative and slightly more expensive. Also, many of these plans have a waiting period (usually two years) before benefits are paid in full. If the policyholder dies during this period, the payment may simply be a refund of the premium, sometimes plus some interest.

Why Consider This Option?

For the elderly with dementia, such a program ensures some financial security without worrying about rejection. It’s like a safety net that keeps you and your family at peace.

Traditional life insurance is required for dementia.

For dementia, traditional life insurance can be difficult to navigate. Here’s what you need to know.

Why do traditional carriers often underestimate patients with dementia?

Traditional life insurance requires a thorough health check, called underwriting. Insurance companies see a higher risk when you have dementia because the condition often leads to higher medical costs and a shorter life expectancy. It’s like trying to insure a car that already has engine problems.

What Happens in the Application Process?

You will have a medical examination and respond to inquiries about your health upon request. It will be similar to a doctor’s exam but with additional documentation requesting your medical history. Your insurance provider will closely examine your dementia diagnosis, including its nature, severity, and management strategies.

Reality Check

It is similar to a tightrope walker working without a net—not much wrong—because most typical policies are not designed to manage high-risk illnesses like dementia by not imposing numerous higher premiums or having restrictions that limit coverage.

What can you do about it?

Speak with an insurance broker about whether this is the course you want to take. They function similarly to insurance-based wilderness guides. They can offer suggestions that might be the best fit for your circumstances or assist you in locating carriers who are likely to charge you a fee.

Who qualifies for guaranteed issue life insurance?

When you apply for guaranteed life insurance, the requirements are straightforward:

- It would help if you were a U.S. citizen.

- Your age should be between 40 and 85.

- It would help if you lived in a state where the product is available.

- You must understand what you’re buying and be able to sign the application.

That’s it! Yes, it really is that simple. Policies with no questions asked are the easiest way to get life insurance coverage.

Benefits of Guaranteed Life Insurance for seniors with Dementia:

Here are the key features and benefits of a guaranteed issue life insurance policy:

- No medical questions or exams are required.

- Acceptance is guaranteed.

- Monthly premiums are fixed and won’t change.

- Death benefits are guaranteed.

- The policy accumulates cash value over time.

- There’s no expiration date; the policy lasts for life.

- There is a mandatory waiting period before full benefits apply.

This type of policy is a solid choice for people with dementia. However, while these points outline the main benefits, it’s wise to dig a little deeper. We recommend doing some research and consulting with an insurance expert to get a complete understanding.

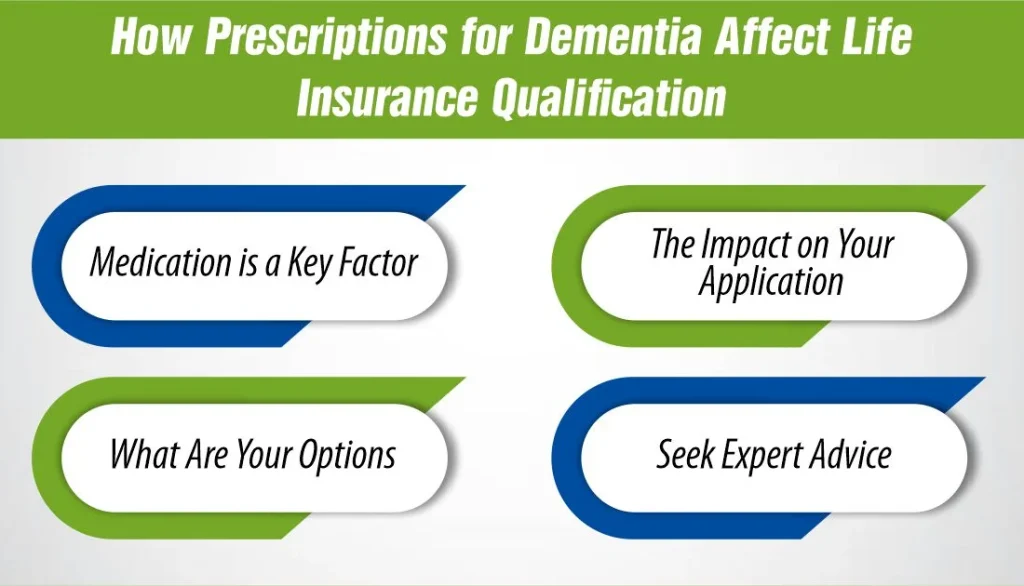

How Prescriptions for Dementia Affect Life Insurance Qualification:

How Prescriptions for Dementia Affect Life Insurance Qualification:

Applying for life insurance means your health gets put under the microscope—especially if you’re taking medication for dementia.

Medication is a Key Factor

When insurers see prescriptions for dementia on your application, they tune in closely. This isn’t just idle curiosity; it’s because these medications signal ongoing health issues, which can affect your insurance costs and eligibility.

The Impact on Your Application

So, what does this mean for you? Typically, having a prescription for dementia makes it tougher to qualify for traditional life insurance. It’s like trying to get a loan with a less-than-perfect credit score; you might face higher rates or even get declined.

What Are Your Options?

But here’s a bit of good news: not all doors are closed. Guaranteed issue life insurance doesn’t ask about medications at all. Think of it as the friendly neighbor who doesn’t fuss about what’s in your medicine cabinet.

Seek Expert Advice

It’s smart to chat with an insurance expert. They’re like navigators for the tricky waters of insurance policies. They can help you find a path that works for your situation, ensuring you get all the benefits you need.

Applying for Life Insurance Coverage with Dementia

Getting life insurance with dementia might sound daunting, but it’s doable. Here’s how to tackle the application process.

Start Simple

First, look into guaranteed issue life insurance. It’s the easiest route. There are no medical exams or health questions. It’s like signing up for an online service—quick and straightforward.

Know the Basics

You’ll need to meet a few basic requirements like age and residency. Make sure you have all your personal details handy—just like filling out a form for a new app or service.

Understand the Terms

Read the terms carefully. Know what you’re signing up for, especially things like the waiting period before benefits kick in. It’s like checking the return policy when you shop online.

Get Help if Needed

If the options seem confusing, don’t sweat it. Talk to an insurance expert. Think of them as your personal shopper for insurance. They can help you navigate the options and find the best fit for your needs.

Submit Your Application

Fill out your application for life insurance for dementia patients. Double-check your information, sign it, and send it off. Now, you’re all set. It’s a bit like ordering a pizza—all you have to do is wait for a confirmation.

Applying for life insurance with dementia doesn’t have to be a headache. With the right information and some guidance, you can get the money you need.

If I develop dementia or Alzheimer’s disease, how will my life insurance values be affected?

If you develop dementia or Alzheimer’s disease, your life insurance rates can be affected. Here’s what you need to know.

Impact on capacity and insurance costs

Dementia and Alzheimer’s can wreak havoc on your mental and physical abilities. If you find out you are insured after applying for insurance, you may see your premiums go up. This is because insurers consider increased health risks more liability.

Choosing the Right Policy

For those diagnosed with these conditions, guaranteed-issue life insurance policies are an option. These don’t require a medical exam, but they generally cost more than standard policies. Think of it as paying extra for convenience and certainty in coverage.

By understanding these impacts and options, you can better navigate the costs associated with life insurance in the face of such diagnoses.

Conclusion

As we wrap up life insurance for dementia patients, remember that navigating life insurance with dementia doesn’t have to be a headache. Options like Guaranteed Issue Life Insurance make it easy to get coverage even after a diagnosis. Remember, understanding your choices helps you secure peace of mind for the future. So, have you thought about how you’ll protect your loved ones with the right policy?

References:

https://www.legalandgeneral.com/insurance/life-insurance/health/life-insurance-and-dementia/

https://protectyourwealth.ca/life-insurance-dementia-alzheimers/

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.