It is not easy to determine the appropriate amount of life insurance. What amount is required? What kind of policy should you buy? What are the guidelines for choosing the type and level of insurance that are suitable for you and your loved ones? You may use a life insurance needs chart to understand what you should do in your circumstances. The chart is based on aspects such as your age, income, dependents, debts, and so on to recommend the right coverage for life insurance. So when it comes to life insurance, developing an organized point-form chart can help make the decision. Let’s discuss in detail what a life insurance build chart is.

What Is A Life Insurance Build chart?

A build chart is a table that serves as a guideline for the maximum and minimum weight per height that life insurance companies will accept. For example, if you’re only 5’4″, your weight limit will be lower than someone 5’9″.

Every life insurance company has its build chart, and some companies even have no build chart at all.

Life Insurance Build chart or height, and weight tables determine the applicants’ rating class when applying for a life insurance policy. Your build is a significant factor in determining your premium.

According to the company’s build chart, if you are in perfect health but weigh too much, you may end up paying a higher premium or being denied coverage.

Some life insurance companies have very lenient build charts. Being 20-50 pounds overweight doesn’t prevent you from qualifying for the company’s best-rate class. Some even provide additional weight allowances for men and women applying after age 60. This is helpful if you are on the heavier side of the chart.

If your only issue is being overweight, you will still qualify for the best life insurance rates with some companies. Even if you have a high BMI and are generally obese, you can still get great-priced burial insurance as there are life insurance companies with no build chart.

It is usually mobility issues and weight-related complications such as diabetes or heart disease that may cause you to receive a poor rating or a higher premium. It is important to shop around with the help of an independent life insurance agency like Funeral Funds to see which company will offer you the lowest rate for your height and weight.

Burial Insurance And Build Chart Underwriting

The primary objective of insurance underwriting is to assess your overall medical risk level. Obesity is known to cause many diseases and this poses the life companies insurance risk of paying out the benefit earlier than expected.

Life insurance companies base the rates on the risk or probability that the insurance company has assessed that you will die while the policy is active.

The Centers for Disease Control and Prevention reports that being overweight increases your mortality risk for:

- Stroke

- Heart disease

- Cancer

- Diabetes

- High cholesterol

- High blood pressure

- Liver disease

- Kidney disease

- Osteoarthritis

- Sleep apnea

Although you may not have developed any of these medical conditions, the insurance providers won’t offer you the best rate if you fall outside their recommended weight limits because being overweight can increase your chances of having medical problems later in life.

Burial Insurance And Build Chart

Most insurance companies have a Life Insurance Build chart to determine the maximum weight for each rating category. Some companies use a unisex weight chart. This is more favorable to overweight women since men have a higher range of acceptable height-to-weight ratios.

Burial insurance companies that have built charts generally have lenient height and weight requirements as they are designed for more elderly individuals (and we tend to get heavier as we get older).

Some burial insurance or final expense insurance companies have no build chart at all. With these companies, you can be overweight, which does not matter. They won’t care whether you are overweight or underweight, which will not impact your rate.

Burial Insurance For Overweight

The only way being overweight could become an issue with most life insurance companies is if you have mobility issues. If you are too heavy that you need help in activities of daily living, your application for traditional life insurance will be declined, but you still have other options.

How Much Does Life Isurance Cost?

By answering six activities that you do daily, life insurance or funeral insurance companies assess your mobility, and you will find out whether you will have immediate coverage or not.

- Consumption – the act of taking food in through a cup, a plate, a spoon, or a fork, through a feeding tube, or intravenously.

- Mobility – how well you can move around in your home, whether you need a walker, cane, or wheelchair. Bathing your entire body with the use of a basin, a shower, or a tub.

- Getting dressed – removing the clothing and wearing it. Other activities that involve dressing are putting on and taking off fasteners, braces, and prostheses.

- Toileting – your mobility and physical strength to use the toilet and do all that is required in this process.

- Transferring— also called positioning or repositioning, which involves the physical movement of a patient between bed, chair, or wheelchair. It encompasses entering and exiting vehicles.

However, if you are morbidly obese and require assistance in these activities, then even the companies that do not necessarily provide a build chart, will not consider you for level death benefit. The right choice for you is to get guaranteed issue life insurance. We can assist you in obtaining an affordably priced policy.

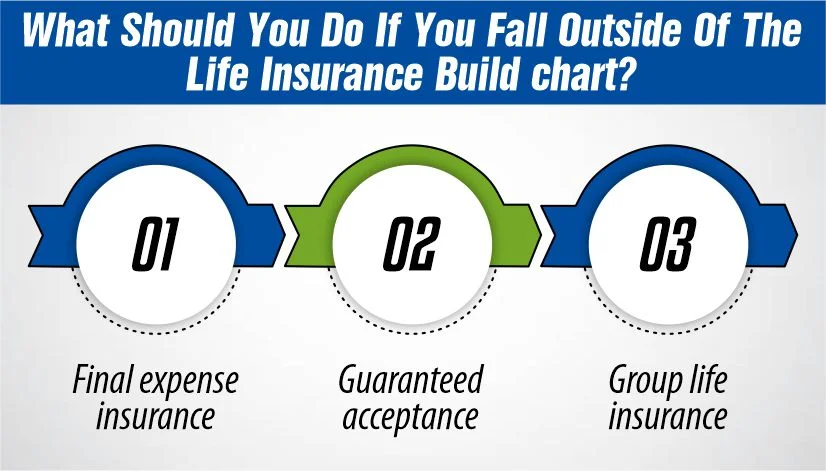

What Should You Do If You Fall Outside Of The Life Insurance Build chart?

Given your height, being too heavy could result in a decline or a much higher price. The obvious solution is to lose weight and apply for coverage later, but that can take many months or even years.

If you need coverage now and your build is an issue, here are some options you can pursue today.

– Final expense insurance

Final expense insurance, often known as burial or funeral insurance, is a form of whole-life simplified issue insurance product designed solely to offer a fast payout for your funeral and burial. Still, it is a type of life insurance, meaning that the net outcome is going to be cash and tax-free money that will be delivered to your family. It means that money can be used for anything.

Another interesting aspect of a burial insurance policy is that it does not have strict requirements for approval. The maximum height and weight limitations of these products allow for a fairly large degree of tolerance. It is also possible to apply for this program even if the candidate is significantly obese.

– Guaranteed acceptance

Guaranteed issue life insurance is a form of whole life insurance with no questions asked about the individual’s health. It is called guaranteed acceptance because, well, you are guaranteed acceptance there. There is no need to worry because you can be given a new policy especially if you are short and if you are fat. However, there are two major disadvantages of these no health plans. First, they are more expensive since the insurer has no information about your health status. Second, there is a requirement that there should be a waiting period of two years before the death of the deceased person.

This policy only pays out the cash back plus roughly 10% interest in the first two years of passing and nothing later. You must have lived for more than 24 months before you can benefit from the full death benefit payout.

– Group life insurance

This is an insurance product in which a group, especially an employer, buys the policy. Companies don’t need to provide their employees with group life insurance, but it is a common practice among them. The first advantage of group life insurance is that you do not need to qualify for the coverage as an individual. The good thing is that everyone in a group bears equal risk hence your factors of insurability are not taken into consideration.

In most cases, there are no qualified criteria that control the offering of group life insurance plans. So if based on height-to-weight ratio exclusion you cannot afford the type of life insurance that you desire, you should consult your employer to know if you can be provided with any form of life insurance. The only important thing you should bear in mind is that reliance on group life insurance is highly unwise.

Most of the group life insurance policies rarely follow you when you change your job or organization. Whether it is retirement, when you are fired, or if you quit, generally any life insurance that you had through an employer will end with your employment. That’s why every person should have the life insurance purchased on his own, without the group ones.

Conclusion

Investing in life insurance is not just about securing your financial future; it’s about providing peace of mind for you and your loved ones. With the right Life Insurance Build chart, you can protect your family’s financial well-being, ensuring they are supported no matter what life throws your way. Ready to take the next step in safeguarding your future? How would you feel knowing that your family’s security is guaranteed?

FAQs

1. What is a Life Insurance Build chart?

A build chart is an insurance underwriting tool that considers an applicant’s height and weight when determining insurability and premium rates.

2. Why is a build chart important?

This is important because it helps to determine an insurance company’s risk in insuring an individual. It also helps set premiums commensurate with the risk being assumed.

3. What factors are considered in a build chart?

Some factors are considered in a build chart. These include height, weight, age, gender, health history, and family health history.

References:

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.