Most seniors searching for small life insurance coverage make one costly mistake right out of the gate like they assume a $5,000 policy isn’t worth the hassle, or they grab the first TV ad they see without comparing anything.

Here is the truth. A best $5,000 life insurance for seniors policy can be one of the smartest, and also the most affordable moves you make right now. But only if you pick the right type, from the right company, before your age or health closes that window.

This guide gives you the real numbers, clear comparisons, and a straight answer, and there is no fluff, no pressure.

What Is a $5,000 Life Insurance Policy for Seniors, Really?

A $5,000 life insurance policy is the most commonly a final expense whole life policy that is also called burial insurance or funeral insurance. This is the permanent policy designed to cover end of life costs so your family is not left scrambling for cash at the worst possible moment.

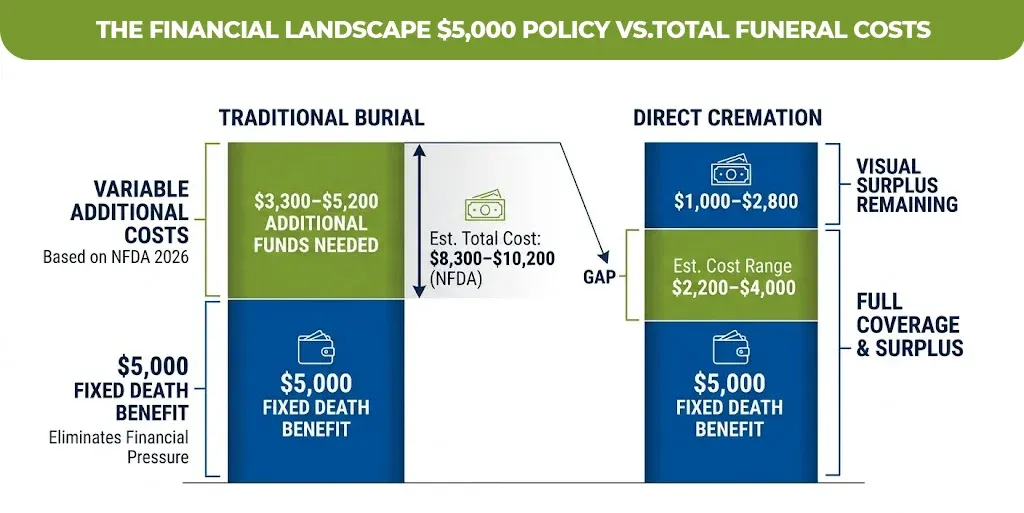

According to National Funeral Directors Association NFDA, in 2026 the average price of the funeral with the burial is around $8,300 to $10,200, and this will be depending on your region and the state you live in. A $5,000 policy will not cover all of the expenses, but it can eliminate the most financial pressure.

Who is this policy designed for?

- Seniors aged 50 to 85 who want affordable, permanent coverage

- Those on a fixed income who can’t afford $100+ monthly premiums

- People who just want to cover a funeral or final medical bills

- Individuals who may not qualify for larger policies due to age or health

Unlike a 5,000 term life insurance policy which expires, a final expense whole life policy never runs out. Your rate is locked in the day you buy it and will never increase.

How Much Does a $5,000 Life Insurance Policy Cost Per Month?

This is the question everyone actually wants answered, so here it is.

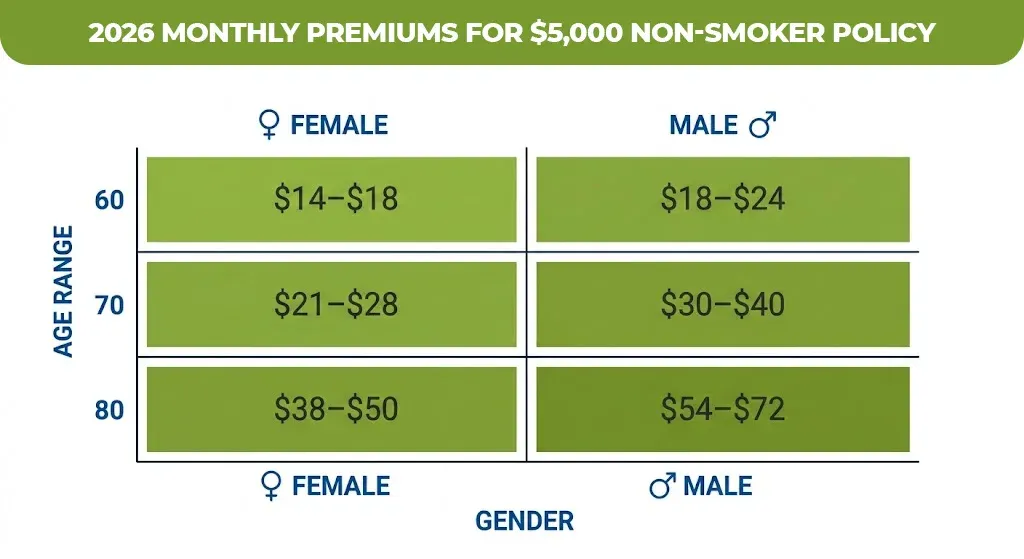

The Monthly costs for a 5000 life insurance policy can be different depending on the age, gender, health, and the type of underwriting. Below are the realistic 2026 sample rates that are are based on the industry data from top providers like Mutual of Omaha and Gerber Life

Sample Monthly Premiums for a $5,000 Final Expense Policy (2026)

| Age | Female (Non-Smoker) | Male (Non-Smoker) | Female (Smoker) | Male (Smoker) |

| 60 | $14–$18/mo | $18–$24/mo | $22–$28/mo | $28–$36/mo |

| 65 | $17–$22/mo | $23–$30/mo | $26–$34/mo | $34–$44/mo |

| 70 | $21–$28/mo | $30–$40/mo | $32–$42/mo | $44–$58/mo |

| 75 | $28–$36/mo | $40–$54/mo | $42–$56/mo | $58–$76/mo |

| 80 | $38–$50 per mo | $54–$72/mo | $56–$74/mo | $72–$95/mo |

At age 65, a healthy woman can expect to pay roughly $17–$22 per month for a $5,000 policy. That is actually less than a Netflix subscription with coverage that lasts for life.

Pros And Cons

Pros

- Low monthly cost

- Easy approval process

- No medical exam

- Lifetime fixed coverage

- Helps funeral expenses

Cons

- Low coverage amount

- Higher cost per dollar

- Waiting period applies

- Limited payout value

- Not for large needs

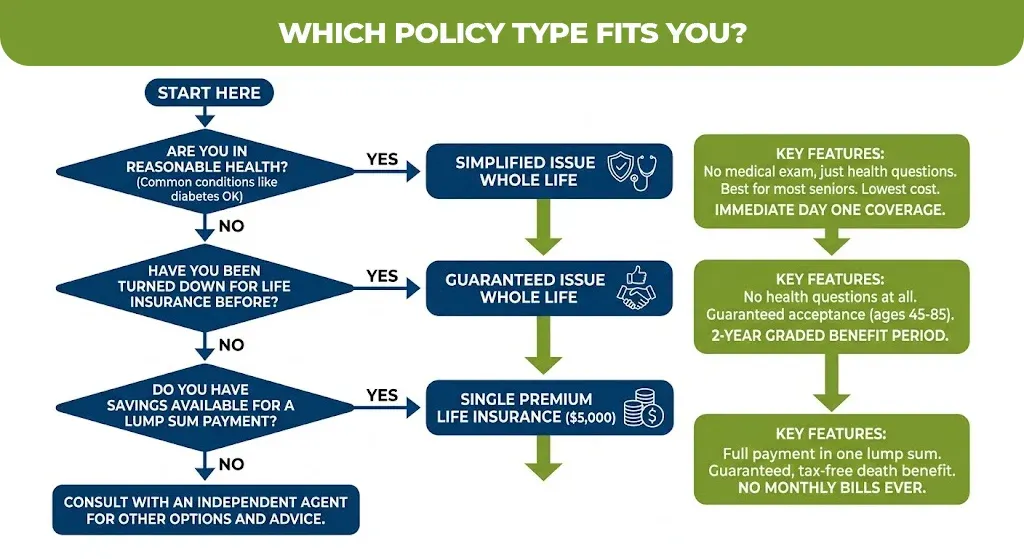

5,000 Life Insurance Policies for the Elderly: Which Type Should You Choose?

There are three main policy types seniors should know about. Choosing the wrong one can mean paying more than necessary or ending up with coverage that doesn’t pay out when it should.

Simplified Issue Whole Life – Best for Most Seniors

In this plan no medical exam is required, you just have to give answers to the few health questions. Most seniors with common conditions like high blood pressure or diabetes qualify. This is typically the lowest cost option with immediate day one coverage and fixed premiums for life.

Guaranteed Issue Whole Life

You will get no health questions at all. Anyone aged 45 to 85 qualifies. The trade-off is a 2-year graded benefit period for natural death, and higher premiums for the same coverage amount. Best for seniors with serious pre-existing conditions.

Single Premium Life Insurance ($5,000)

A single premium life insurance $5,000 policy lets you pay the full amount in one lump sum like no monthly bills ever. This will work well for seniors with some savings who want a guaranteed, tax-free death benefit without ongoing premium risk. Carriers like Lincoln Benefit Life and some mutual companies offer these.

Which should you pick?

If you are in reasonable health, go to the simplified issue. If you have been turned down before, try the guaranteed issue. If you have a lump sum available and hate monthly bills, explore single premium options with an independent agent.

Best Companies for $5,000 Life Insurance for Seniors in 2026

Not every carrier is worth your time. Below are the most consistently recommended companies based on price, underwriting flexibility, financial strength ratings, and customer satisfaction data from J.D. Power 2025 Life Insurance Study.

Top Carriers for $5,000 Senior Life Insurance Policies (2026)

| Company | Best For | AM Best Rating | Waiting Period |

| Mutual of Omaha | Overall best value, lowest prices | A+ | None (simplified issue) |

| Gerber Life | Guaranteed acceptance, no questions | A+ | 2 years (graded) |

| Aetna / CVS Health | Competitive guaranteed issue rates | A | 2 years |

| Physicians Mutual | No exam, good for health conditions | A+ | None (most applicants) |

| AARP / New York Life | AARP members, no medical exam | A++ | Varies by plan |

| Transamerica | Fast approval, no-exam options | A | None (simplified) |

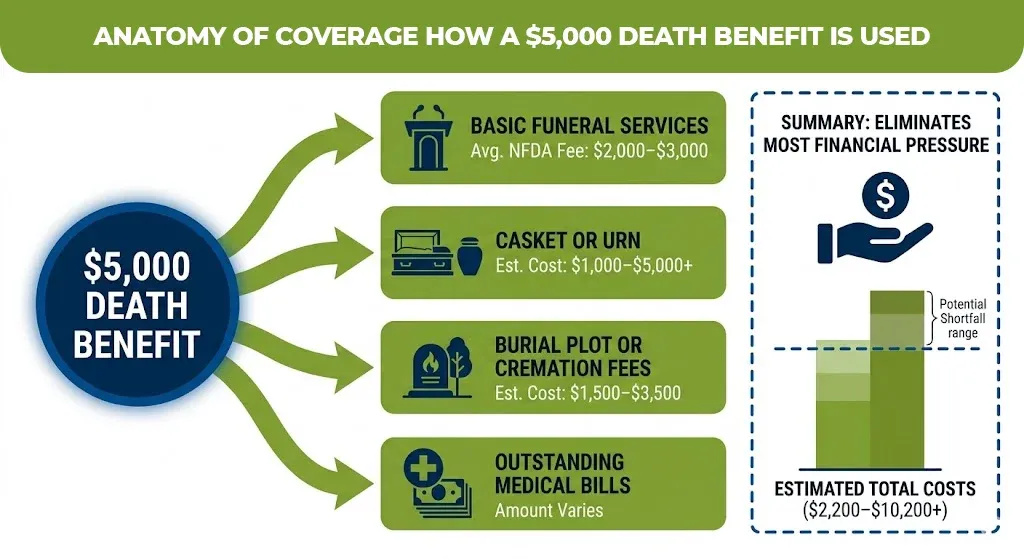

What Does a $5,000 Policy Actually Cover?

The death benefit from a 5000 life insurance policy is directly paid to the beneficiary and this is tax free. They can use it for anything, but here is who most families spend this money:

- Funeral home basic services fee can be $2,000–$3,000

- Casket or urn can cost $1,000–$5,000+

- Burial plot or cremation fees, $1,500–$3,500

- Death certificates (multiple copies) can be $100–$300

- Outstanding medical bills

- Credit card balances

- Transportation and flower

According to NFDA data and 2026 projections, even a direct cremation that is the simplest option, can average $2,200–$4,000 nationally. A $5,000 policy can cover that in full, leaving something left over.

What to Watch Out For: 3 Mistakes Seniors Make

- Buying from TV without comparing

- Choosing accidental death only policies

- Skipping comparison shopping

How to Get Right $5,000 Policy Without Overpaying

Here’s a simple framework

- Decide your goal first

- Check your health

- Compare at least 3 carriers

- Ask about the waiting period

- Lock in your rate now

Ready to Find Your Best Rate?

If you have read this far, you already know more than most seniors who walk into a bad policy. The next step is very simple, like comparing the real quotes from top-rated carriers based on your age, state, and health, with no pressure and no commitment.

M-Life Insurance works with independent advisors who shop multiple A-rated carriers to find your lowest rate for a $5,000 final expense policy. There is no medical exam required for most applicants, and you can see options in minutes.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.