Key Takeaways

- Fixed premiums vs flexible premiums

- Guaranteed vs market-linked growth

- Higher cost vs lower start

- Stability vs investment risk

- Predictability vs growth potential

You were standing at the crossroads with your life insurance decision, and your agent mentioned both whole life insurance and indexed universal life, but the terms made your head spin for a while about what to choose. The truth is, these two permanent insurance products look similar on the surface, but they work very differently in your pocket. Understanding the real differences could save you thousands in premiums or leave you with significantly better coverage.

Whole Life Insurance vs Indexed Universal Life: The Core Difference

Whole life insurance offers fixed premiums and guaranteed cash value growth, while indexed universal life ties cash value returns to stock market indexed but with lower premiums and more flexibility.

Think of your whole life as the steady , predictable option that your premium never changes, your death benefit is locked in, and your cash value grows at the guaranteed rate set by your insurance company that is 2 to 4% annually as of 2025. indexed universal life insurance, on the other hand, lets you cash value ride on the performance of indexes like S&P 500, offering higher up-side potential but no guaranteed floor.

These fundamental differences shape everything else about these products.

What is Whole Life Insurance?

Whole life insurance is a permanent life insurance policy with fixed premiums, guaranteed death benefits and cash value that will grow at the pre-determined rates regardless of market performance.

With whole life insurance, your insurance company takes the investment risk. You pay the same premium every month for life, whether you are 35 or 75. A portion of each premium funds your benefit and the rest builds cash value in your policy. This cash value is guaranteed to grow at the rate your policy states, typically locked in when you purchase.

You can borrow against this cash value and any policy loans reduce your death benefit until you repay them.

Real-world numbers from 2025-2026 data:

- The average whole life premiums for a $500,000 death benefit, age 45 is $300-$500 per month

- The guaranteed cash value growth rate is 2 to 4% annually

- Surrender charges are typically phased out after 15 to 20 years.

What is Indexed Universal Life Insurance?

Indexed Universal life Insurance is a permanent policy where cash value returns are linked to the stock market index, with flexible premiums and benefit options.

IUL gives you more control. You choose how much to pay in premiums each month, and your insurance company adjusts your death benefit accordingly. Your casual does not earn a fixed rate, instead it tracks the performance of an index, usually capped at maximum return of an 8 to 12% annually.

Here is the catch, there is typically a floor of 0%, which means that if the market crashes, you do not lose money, but you also earned nothing that year. This will balance the upside without downside sounds perfect until you realise the caps limit you gained.

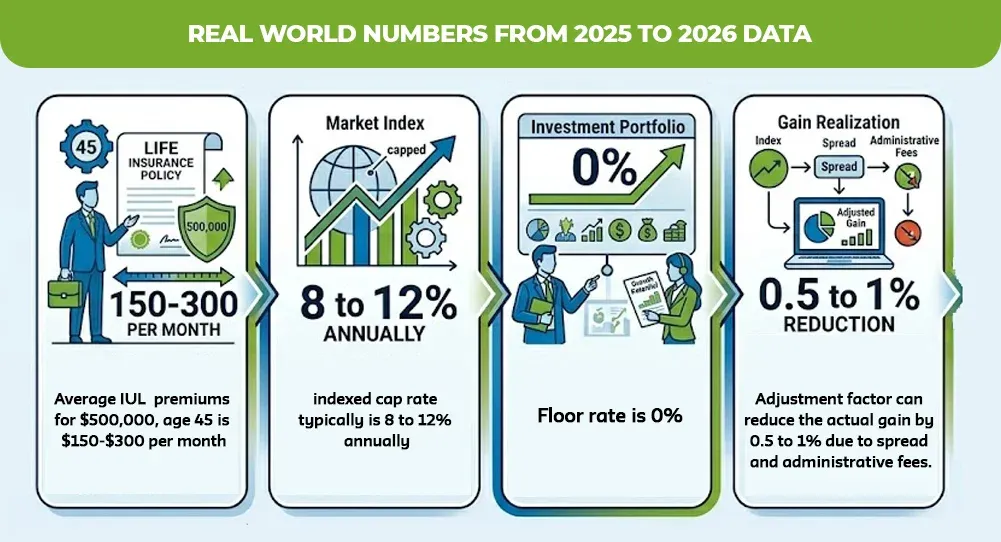

Real world numbers from 2025 to 2026 data

- Average IUL premiums for $500,000, age 45 is $150-$300 per month

- indexed cap rate typically is 8 to 12% annually

- Floor rate is 0%

- Adjustment factor can reduce the actual gain by 0.5 to 1% due to spread and administrative fees.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.