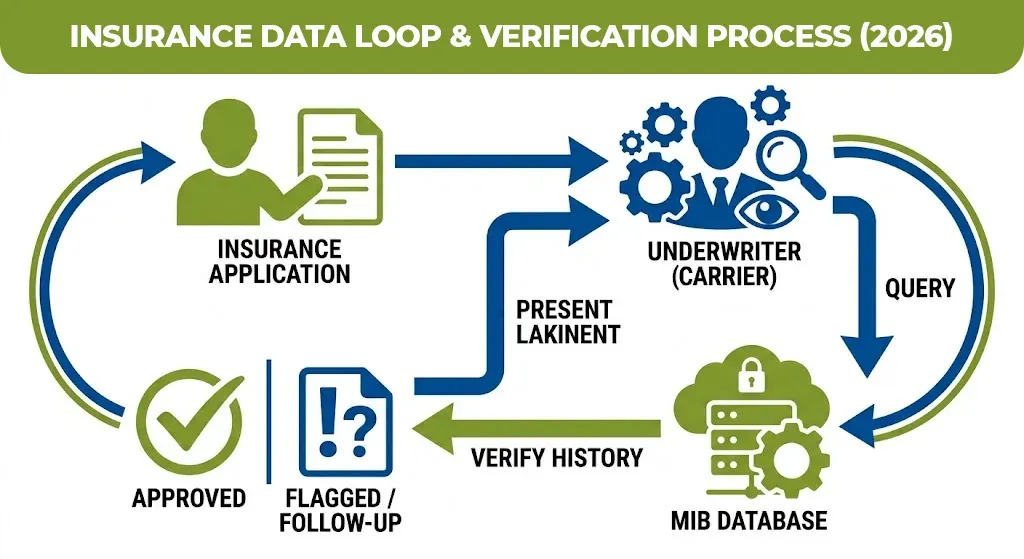

You sit down to apply for life insurance. You answer every question honestly. And the underwriter still flags something you didn’t expect.

It probably came from a report you have never seen, like filed by a company you have never heard of, and it is based on insurance applications you made years ago.

That organization is the Medical Information Bureau, and it may already have a file on you.

What Is the Medical Information Bureau – and Why Does It Matter?

The Medical Information Bureau MIB is a nonprofit organization that has operated since 1902. It maintains the coded database of health and lifestyle information that is pulled from previous insurance applications across the U.S. and Canada.

When you apply for individual life, health, disability, critical illness, or long term care insurance, your insurer doesn’t just take your word for it. They query the MIB to verify whether what you are telling them today matches what you told other insurers in the past.

Think of it as a credit bureau, except instead of tracking debt, it tracks your medical history as it relates to insurance. The Federal Trade Commission confirms it is regulated under the Fair Credit Reporting Act (FCRA), which gives it the same legal weight as a credit report.

Who Makes Up the Medical Information Bureau?

The MIB is owned and funded by its member insurance companies, like currently around 430 carriers in the U.S. and Canada. These are not the small players.

According to the Federal Trade Commission, MIB member companies account for 99% of individual life insurance policies and 80% of all health and disability policies issued across the U.S. and Canada. In practical terms. If you are applying for individual coverage anywhere in North America, the underwriter almost certainly has access to the MIB system.

Coverage Type | % of Market Covered by MIB Members |

Individual Life Insurance | 99% |

Health & Disability Insurance | 80% |

Long-Term Care Insurance | Majority of underwritten policies |

Group / Employer Plans | Not included |

The MIB is not a government agency. It is a private, member owned corporation headquartered in Braintree, Massachusetts. Its members share the information with each other, like coded, not raw, so the underwriters can cross check your current application against your history.

What’s Actually In Your Mib Medical Information Bureau Report?

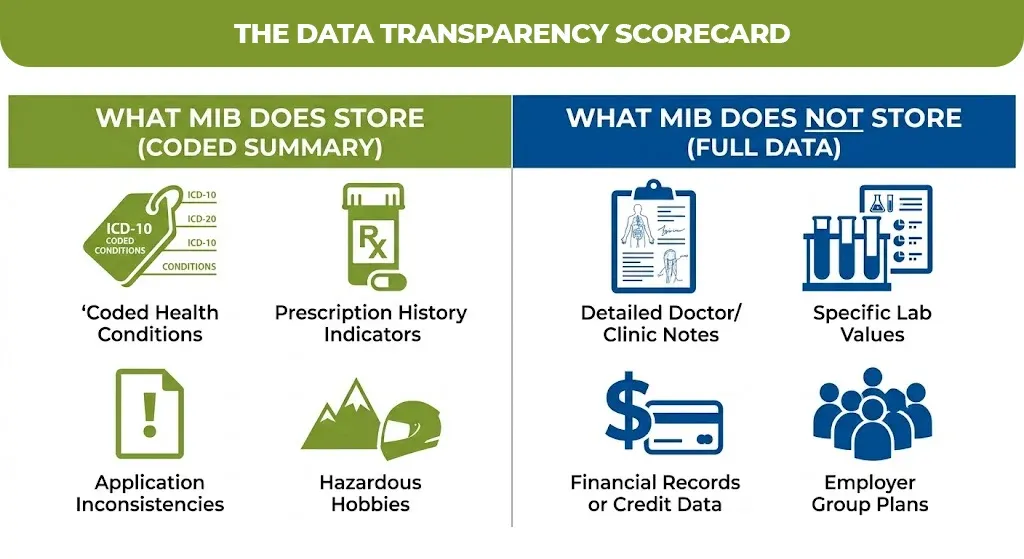

This is where most people get it wrong. Your MIB report is not a copy of your medical records. Doctors’ notes, lab results, and hospital charts are not in it.

What The MIB Does Store

- Coded summaries of health conditions that are disclosed on the past insurance applications

- Hazardous hobbies or any occupations that is flagged during underwriting

- Prescription drug history indicators in coordination with pharmacy databases

- Inconsistencies between applications, such as a condition disclosed in 2020 that disappeared from your 2024 application.

The information is coded using a proprietary system to protect your identity. Your name and address are stripped from what’s shared between the insurance companies, though MIB holds identifying information to connect codes to the right person.

What’s Not In Your MIB Report

- Actual physician notes or diagnoses

- Lab or test results

- Financial records or credit data

- Information from employer group plans.

How to Get Your Free MIB Report in 2026

You have a legal right to request your MIB consumer file once every 12 months at no cost, under the Fair Credit Reporting Act. You are also entitled to a free copy if an insurer takes adverse action against your application, such as a denial or rate increase, within the last 60 days.

How to request it

- Visit mib.com and use the online request form

- Or call MIB directly at 1-866-692-6901

- You will need to verify your identity , then MIB cross checks with other consumer reporting agencies

What to Do If Your MIB Report Has an Error

Errors happen and on an MIB report, even a small coding mistake can trigger the higher premium or added underwriting scrutiny.

Under the FCRA, you have the right to dispute inaccurate information. MIB is legally required to investigate within 30 days and correct any errors it confirms. If it finds the information accurate but you still disagree, you can add a consumer statement to your file explaining your position.

Errors worth disputing include:

- A health condition listed that you’ve never been diagnosed with

- A flagged application that isn’t yours identity mix-up

- Outdated information on a resolved condition

- A condition listed under the wrong dates

Does the MIB Report Determine If You’re Approved or Denied?

No, and this is one of the most misunderstood points.

Insurance companies cannot deny the coverage based solely on your MIB report. The MIB report is one input in the underwriting process. It prompts follow up the questions, not automatic rejection.

What can happen

- The underwriter requests an attending physician statement APS

- You’re asked to take a medical exam

- Coverage is offered at a higher premium rated policy

- A specific condition is excluded from coverage

The MIB’s own data shows that January 2026 recorded the highest year-over-year growth in life insurance application activity for any January on record, up 9.5% as compared to the prior year. More people are applying. More MIB queries are being run. Understanding how the system works is no longer optional if you want the best rate.

Pros And Cons

Pros

- Helps detect insurance fraud

- Speeds up policy reviews

- Finds application mismatches

- Protects insurers from risk

Cons

- Errors may affect approval

- Old data causes confusion

- Consumers rarely know details

- Can increase insurance costs

The Bottom Line: Check Before You Apply

The Medical Information Bureau is not working against you. It exists to keep insurance pricing fair, like catching the fraud so that honest applicants do not have to pay for other people’s deceptions.

But if there is an error in your file, or if your previous applications created a flag you are not aware of, you could walk into your next insurance application at a disadvantage.

If you are navigating life insurance and want clear, no-pressure guidance, the team at M-life Insurance can walk you through what your MIB report means for your coverage options, and help you find the right policy without surprises.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.