Is a Family Income Policy Suitable for Your Family’s Financial Protection?

In the case of paying off secured finance, it’s often not the case. Larger debts are best protected using a level-term policy, meaning it would pay out a fixed lump sum, regardless of the claim, other than any clauses in the policy.

Suitable situations for a Family Income Benefit Policy could be to cover the cost of living expenses for your family. It may be that you would want to know if they’d continue to have your wages coming into the household until at least your children were through college or university.

Or, if you have care costs, you have to factor them into your current outgoings to know that those costs would continue to be covered for a set period. A family income benefit is income protection, more than it is life insurance.

Who needs family income benefits?

If you have a family that you want to support then consider family income benefits. Here are a few key questions to ask yourself:

- If my family lost my income, would they be able to survive financially?

- Is there any extra cash, savings, or other financial resources that can be used to support the family if I am no longer alive?

- Is there a loan or some other large obligation that I would like to be paid off in the event of my death?

The last question is important because if it is debt that you would want to avoid and you would rather pay off everything then there are always other insurance products that could be ideal for you. Standard life insurance would be an example because the entire lump sum can be spent to meet your mortgage obligation. If, however, you would want your income replaced then family income benefit could be the ideal product for your family and you.

It is important to understand that there is not one type of insurance to cover as many different areas as possible, but there are many different insurance products. How about calling one of our friendly advisors who will listen to your situation and offer you a protection product suitable for you?

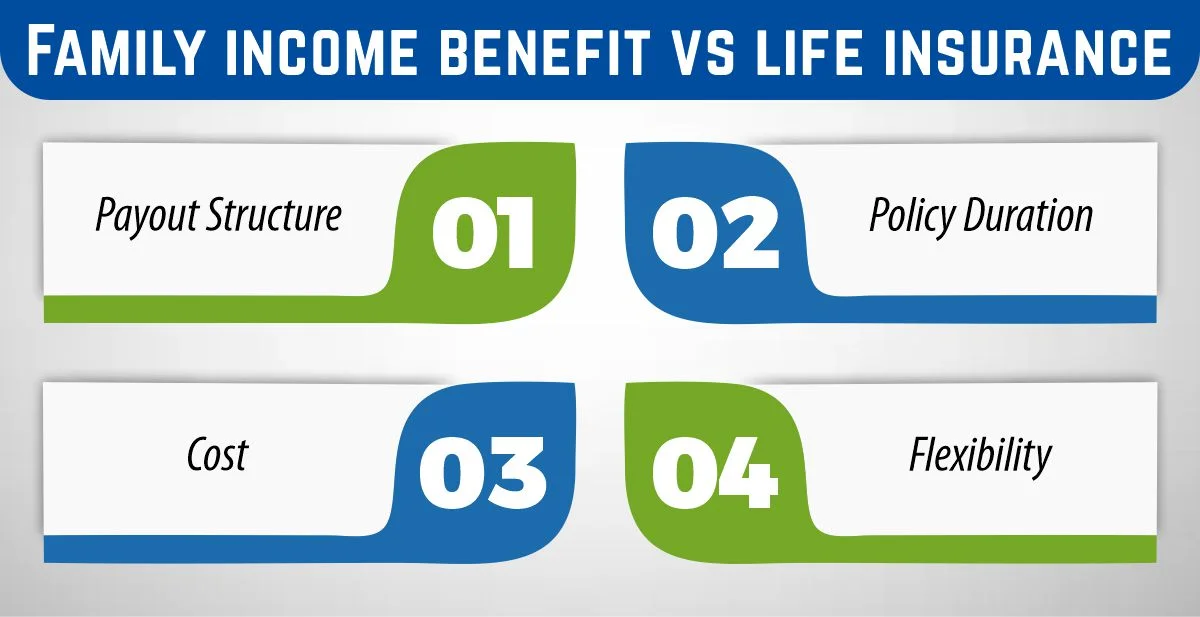

Family income benefit vs life insurance

It is crucial in comparing Family Income Benefit vs Life Insurance to note the differences that make each product suitable for various financial planning needs.

– Payout Structure

- Family Income Benefit Gives your family a predictable and steady monthly income for the agreed time if you die during the policy period. It is like a replacement income to cater for several expenses that you have in the family.

- Life Insurance makes a cash payment to your beneficiaries at your time of death. This money can be used for any need, whether it is for mortgage repayment, expenses for daily needs, or for saving and investing.

– Policy Duration

- In Family Income Benefit Death benefits are paid only for the remainder of the policy term if the person dies during the term. For instance, if you take a policy that has a coverage period of 20 years and pass it on in the tenth year, then your family shall continue to receive payments for the next 10 years.

- Life insurance is payable no matter when the policyholder dies within the term. If it is a term policy then the policy will pay if one dies within that term or the policy period. Depending on the policy type it is, be it a whole-life policy, it provides a payout whenever you die.

– Cost

- Family Income Benefit is generally more affordable because the overall amount can be smaller, depending on the timing of the policyholder’s death.

- In Life Insurance the costs may differ, depending on the type of the policy, and can be significantly higher with whole-life policies while term policies can be cheap, especially for young people.

– Flexibility

- Family Income Benefit: They tend to offer a fixed and more predictable income, but not as much flexibility regarding the payout structures.

- Life Insurance: This gives more flexibility since your beneficiaries will receive the benefits in cash form that they can manage as they wish.

Which Should You Choose: Family Income Benefit vs Life Insurance?

Family Income Benefit is Recommended for those who desire to make sure their family has an income source once they are dead, especially for families that have regular expenses like payment for rent or school fees. Life Insurance is Most suitable for people who wish to leave behind lots of money to cater for the major expenses or needs of the family.

Family income benefit vs life insurance – which is better for your family?

Unfortunately, the answer to this question is not quite as straightforward and depends on your specific family circumstances and insurance requirements. Here are some things to consider, however:

Family income benefits are truly for everyday expenditures, starting with rent and extending to power and water bills. If you have a mortgage that you would like to pay off, it may be more beneficial for you to look into family life insurance.

Family income benefits can sometimes be just a little cheaper than life insurance because the size of the payout is dependent on how within the term of the policy you die. Similarly, with level-term life insurance, whether you die on the very first day of the policy or the last day of the policy coverage, you will get the same amount of money in a lump sum.

It is recommended that if one can pay for both, or would like to take cover for things like monthly expenses while the kids are still young and dependent, and for a term-based plan like to pay off the mortgage or for funeral expenses among others, then take the family income benefit policy in addition to the other standard term life insurance policy.

References :

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.