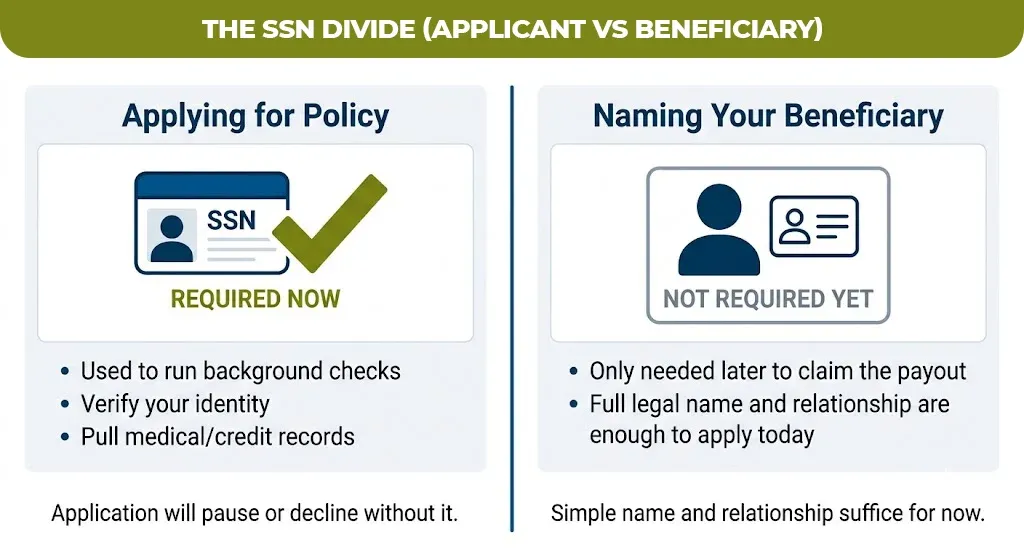

Skip the SSN Field on his life insurance application and most of the insurance companies will pause your file or decline it outright. But keep it on your beneficiary section and it usually will not matter at all. Confusing the two is the mistake that gets the application stuck in underwriting for weeks or gets a beneficiaries claim late after the death in the family.

Do you need a Social Security number for life insurance?

Yes, in almost every case. Most of the United States life insurance companies require the applicant’s SSN to verify the identity, credit report and check the medical information bureau database they will issue a policy. If you refuse to provide it then the insurance company legally declined your application, since no companies are obligated to offer you coverage.

There is an important exception that insurance companies accept an individual tax identification number, passport or the other government ID for applicants who do not have an SSN, including the non-citizens. The requirement is about verifying who are you, not about citizenship status, so the alternative ID can work if the carrier supports it.

Why do life insurance companies ask for your SSN in the first place?

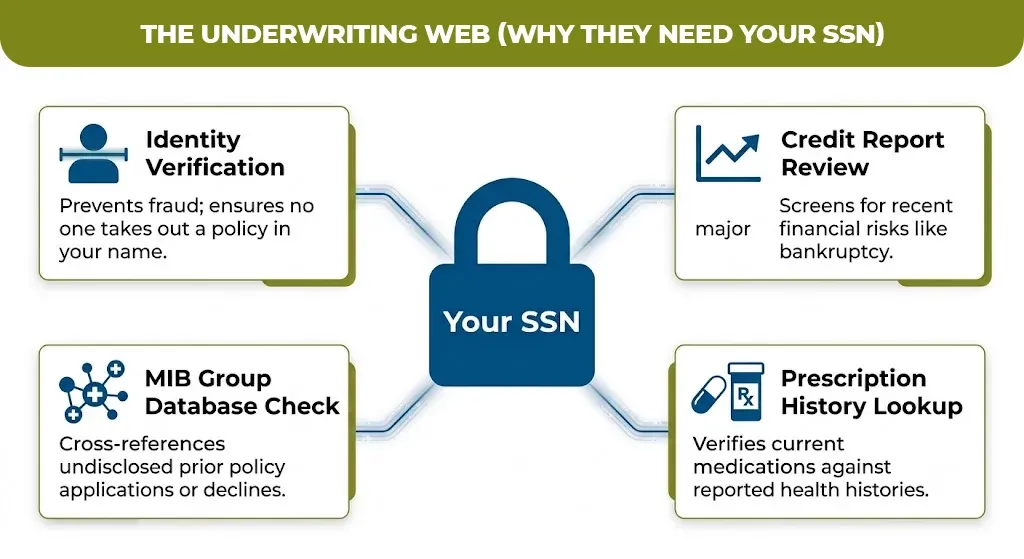

The insurance companies use your SSN for specific underwriting checks, not just the paperwork. Each would directly affect no matter if you are approved and you will pay.

Identity Verification

Confirming that you are the person named on the application, which will prevent someone else from taking out the policy in your name.

Credit Report Review

A recent bankruptcy or major credit event can affect how an underwriter classifies your risk.

Mib Group Check

The MIB keeps the shared history of life and health insurance applications across the member companies so the carriers can cash the undisclosed prior declines

Prescription Database Check

Your medication history can reveal the health condition that you may have forgotten to list on the application.

None of the above these checks were reliable without a unique identifier. Which is why most of the insurance companies treat the SSN as a non-negotiable part of the application rather than an optional field.

Do you need a beneficiary’s Social Security number for life insurance?

No, not at the time you apply. You can name a be beneficial using just their full legal name and relationship to you, and most of the insurance companies will not ask for their SSN during the application process.

The SSN becomes relevant later, when your beneficiary files a claim after your death. At that point, the insurance company generally asked for it to confirm the person filing the claims is the same person you named and the report that payout to the IRS if any portion of it is flexible. Life insurance benefits are not taxable income for the receipt so this is usually a formality rather than a tax bill.

If your named beneficiaries trust, charity or the business other than individual then NSS and will not apply at all, all those entries are identified by an EIN or tax ID instead.

What if you don’t have a Social Security number at all?

You can still get the coverage in so many cases but your options narrow and the process will take more documentation. The carriers that write non-SSN business will generally ask for one of the following in one piece of an SSN.

| Alternative ID | Who it’s typically for | What else the carrier may ask for |

| ITIN (Individual Taxpayer Identification Number) | Non-citizens with U.S. tax filings | Tax returns, proof of income |

| Foreign passport | Foreign nationals, visa holders | Visa status, U.S. residency proof |

| Green card | Permanent residents (often also have an SSN) | Standard underwriting applies |

| Employer group policy | Employees enrolled through work | Often skips SSN entirely for guaranteed-issue amounts |

life insurance time to be the most accessible option without an SSN, since it is the simple to underwrite then permanent coverage. Guaranteed issue policies are another route like this keep the medical underwriting and sometimes the SSN requirement too. Though they come with a lower coverage caps and higher per dollar cost.

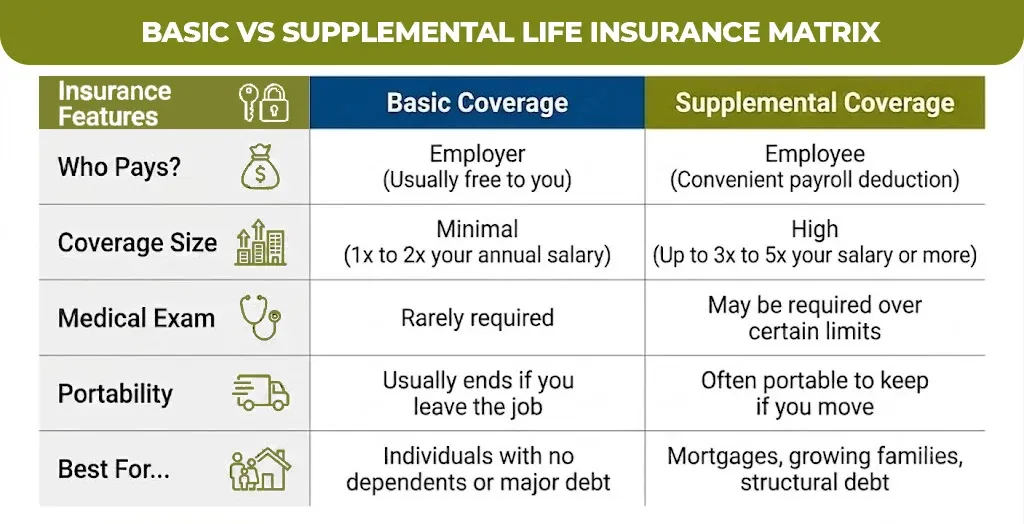

Basic life insurance vs. supplemental life insurance: does the SSN rule change?

No, the SSN requirement work the same way whether you are enrolling in the basic or supplemental coverage. But the two products are easy to confuse so it is worth knowing the difference between you decide how much you need.

| Feature | Basic life insurance | Supplemental life insurance |

| Who pays | Usually employer-paid, often free | Employee-paid, via payroll deduction |

| Typical coverage | 1–2x annual salary | Up to 3–5x salary, sometimes more |

| Medical exam | Rarely required | May be required above a guaranteed-issue limit |

| Portability | Often ends when you leave the job | Sometimes portable; check your plan |

| Best for | Minimal financial obligations | Mortgages, dependents, significant debt |

If you have no dependence and no major death, then the basic coverage to work can be enough on its own. If you have a mortgage, children or a spouse who relies on your income then supplemental coverage or a private term policy usually closes the gap that basic coverage loan cannot cover.

How to protect your SSN when applying for life insurance

Only share your SSN through the verified channel, your carrier’s official application portal, a licensed agent you contacted directly or secure paper form. If someone reaches out first and asks for your SSN over email or an unfamiliar phone number then verify their affiliation with the carrier before responding.

Legitimate insurance companies and the brokers will never pressure you to share the sensitive information immediately or to cancel a quote if you ask for a moment to verify them. If you suspect the fraud, then you can report it to the national Association of insurance commissioner or your state department of insurance.

Getting the right coverage without the guesswork

Whether you’re weighing basic versus supplemental coverage, or you’re not sure which carriers work with your specific ID situation, it helps to talk it through with someone who does this daily. Mlife Insurance can walk you through your options and match you with a policy that fits your situation, SSN or ITIN, no pressure either way.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.