What is a Beneficiary in Life Insurance?

Do you Need Social Security Number for Life Insurance Beneficiary?

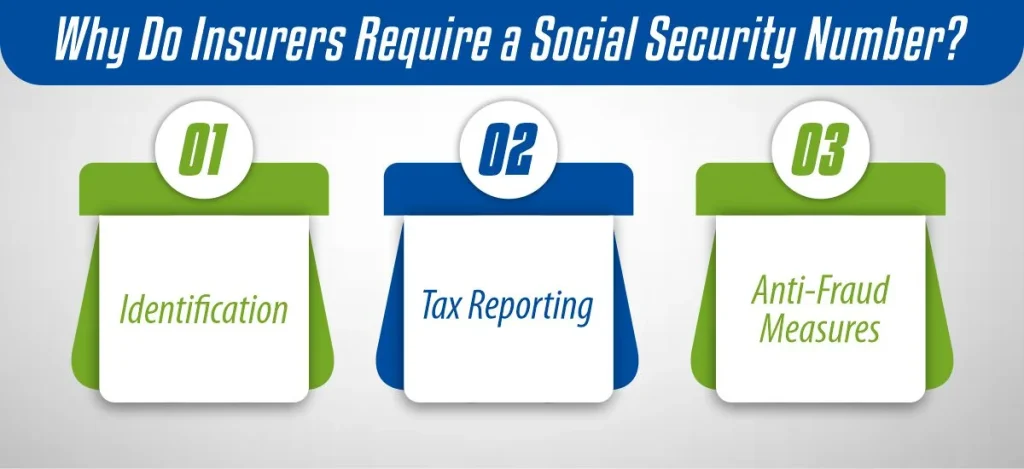

Why Do Insurers Require a Social Security Number?

1- Identification

The SSN serves as a unique identifier for individuals, ensuring that the correct beneficiary receives the policy’s proceeds. This helps prevent errors and ensures the smooth processing of claims.

2- Tax Reporting

3- Anti-Fraud Measures

Requiring the SSN helps insurers prevent fraud by verifying the identity of the beneficiary. It ensures that the beneficiary is a legitimate individual with a valid SSN, reducing the risk of fraudulent claims.

Requesting the SSN of a life insurance beneficiary helps insurers streamline administrative processes, comply with tax regulations, and safeguard against fraud, ultimately benefiting both policyholders and beneficiaries.

What Does The Life Insurance Company Do With Your Social Security Number?

The Social Security number (SSN) plays a crucial role for life insurance companies, enabling them to conduct various checks and assessments to ensure the accuracy and integrity of the insurance process. Here’s what life insurance companies typically do with your SSN:

- Confirmation

Verifying your identity is paramount for insurers to prevent fraud and ensure that the individual applying for coverage is indeed the person they claims to be.

- Credit Report

- Criminal Records

Your SSN enables insurers to conduct a background check on your criminal history, helping them assess your risk level as an applicant.

- Medical Information Bureau (MIB)

- Medication History

Insurers utilize a prescription drug or medication database during underwriting to evaluate your health status. Your SSN is necessary to access this database, allowing insurers to assess your risk class or health rating accurately.

In essence, the SSN serves as a tool for insurers to verify your identity, assess your risk profile, and make informed decisions during the underwriting process, ultimately ensuring fair and accurate insurance coverage for policyholders.

Is a Social Security Number Always Required?

Alternatives to Providing a Social Security Number

If you’re considering alternatives to providing a Social Security number (SSN) for a life insurance beneficiary, here are some options you may explore:

1- Taxpayer Identification Number (TIN)

2- Date of Birth

Some insurers may accept the beneficiary’s date of birth as an alternative to providing an SSN. This can help verify the identity of the beneficiary and ensure that the correct individual receives the policy proceeds.

3- Other Forms of Identification

Depending on the insurer’s policies, other forms of identification may be accepted in place of an SSN. This could include a driver’s license number, passport number, or other government-issued identification.

4- Legal Entity Information

Providing the entity’s legal documentation and tax identification number may be sufficient for beneficiaries that are legal entities such as trusts or charities.

It’s important to note that the acceptance of alternatives to providing an SSN can vary depending on the insurer and the specific circumstances of the policy. If you have concerns about providing an SSN for your beneficiary or if your beneficiary does not have an SSN, it’s advisable to consult with your insurance agent or financial advisor for guidance tailored to your situation.

Final Thoughts

Well! Many life insurance companies request the Social Security number of your beneficiary, but it’s not always mandatory. Providing the SSN helps with identification, tax reporting, and anti-fraud measures, but alternatives may be available. Hope you are now clear about “Do you need social security number for life insurance beneficiary?”

Moreover, by understanding the role of the Social Security number in life insurance beneficiary designations, you can make informed decisions when selecting and managing your life insurance policy.

Frequently Asked Questions (FAQs)

1- Are there any consequences if I don’t provide a Social Security number for my life insurance beneficiary?

While many insurers request the beneficiary’s SSN for various purposes, such as identification and tax reporting, not providing it may not necessarily have immediate consequences. However, it’s essential to check with your insurer to understand their specific requirements and any implications for your policy.

2- Can I designate a beneficiary who does not have a Social Security number?

Yes, you can designate a beneficiary who does not have a Social Security number, especially if they are a trust, charity, or other entity. In such cases, alternative forms of identification, such as a Taxpayer Identification Number (TIN) or date of birth, may be accepted by the insurer.

3- Will my beneficiary’s personal information be protected if I provide their Social Security number?

Yes, life insurance companies are required to adhere to strict privacy and confidentiality regulations to protect the personal information of their policyholders and beneficiaries. Before providing any sensitive information, it’s advisable to review the insurer’s privacy policy and ensure that appropriate safeguards are in place.

How Much Does Life Isurance Cost?

4- How can I ensure that my beneficiary’s personal information is kept secure?

You can take steps to safeguard your beneficiary’s personal information by providing it only to reputable and trusted insurers, ensuring secure communication channels, and regularly reviewing your policy documents for any unauthorized access or use of personal data.

5- What should I do if my beneficiary refuses to provide their Social Security number?

If your beneficiary refuses to provide their Social Security number, you should discuss their concerns and explore alternative forms of identification accepted by the insurer. It’s essential to ensure that your beneficiary’s wishes are respected while complying with the insurer’s requirements.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.