Your child’s future is precious and the thought of losing them is unimaginable. But here is something most parents never consider. Life insurance for kids is not about preparing for the worst, it is all about financial protection and building wealth for the best.

There are so many parents who assume that life insurance is just for income owners. The reality? A child’s death can create devastating financial burdens, funeral costs averaging $7000-$12,000 and also lost earning potential and emotional strain. This is why thousands of parents now secure life insurance policies for kids before their children turn 18 and lock in guaranteed rates in building cash value for their future. Let’s explore whether this protection makes sense for your family

Can You Get Life Insurance for Kids? Yes—And Easier Than You Think

Yes you can absolutely get life insurance for kids and it is more accessible than many parents realize . Children as young as newborn can qualify for the coverage and the policies remain active into adulthood if you keep paying premiums.

The insurance companies offer several options specifically that are designed for children including term and permanent plans. The key difference? Most of the insurance companies do not require children to undergo medical exams making the application process very simple and quick. Parents or guardians apply on the child’s behalf and coverage is typically approved within days.

Types of Life Insurance for Kids: Understanding Your Options

When shopping for a life insurance policy for kids, you will encounter two main categories that are term life insurance and permanent life insurance.

Term Life Insurance for Kids

Term life insurance for kids provides coverage for a specific time that is typically 10, 20 or 30 years. This is the most affordable option and it offers straightforward protection without cash value accumulation. In the coverage and when the term expires, though, so many policies include a conversion option for your child to switch to permanent coverage later without a medical exam.

Whole Life Insurance for Kids

Whole life insurance for kids is a permanent insurance that will last for lifetime and also builds cash value over time. A portion of each premium goes into a savings component that grows tax deferred which your child can borrow against or access later.

Best whole life insurance for kids policies are ideal if you want lifetime protection and a way to fund future needs, college, downpayment on a home or business. So many families view this as a forced saving tool combined with protection.

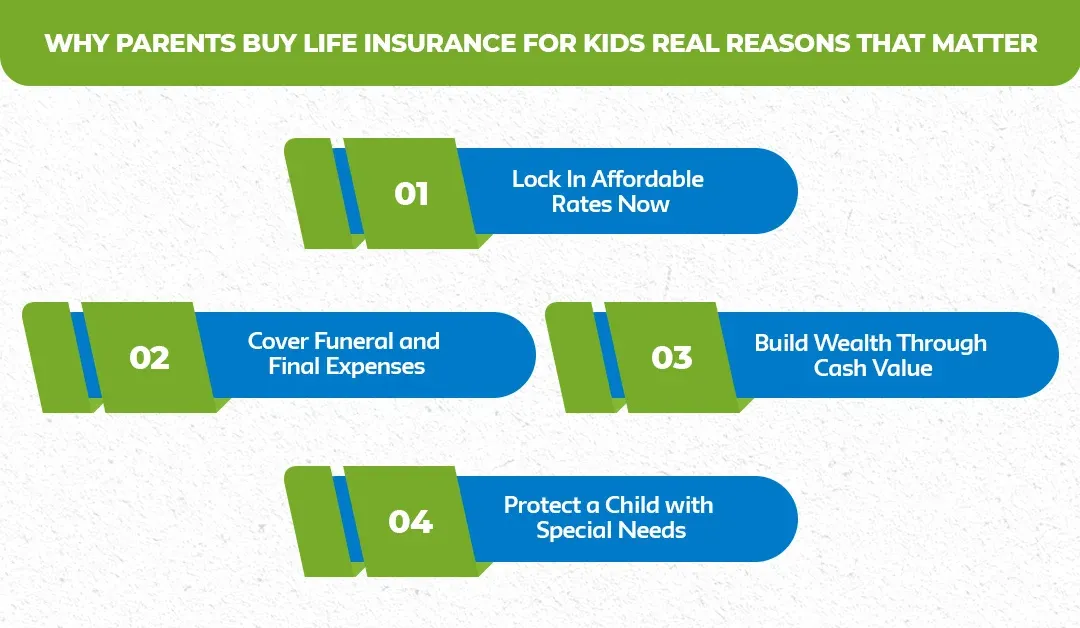

Why Parents Buy Life Insurance for Kids: Real Reasons That Matter

You might wonder why I would insure my child’s life? Here is what my parents understand

Lock In Affordable Rates Now

A healthy child is priced at the lowest possible rates. Life insurance premiums are based on age and health status at the time of application. By securing the coverage today you lock in those rates for life even if your child develops self conditions later. If your child is diagnosed with asthma, diabetes or any chronic illness at age 25 then they will still be at the same rate they secured as a child.

Cover Funeral and Final Expenses

The average funeral cost in the United States is $7000-$12,000 according to the national funeral directors association. A modest life insurance policy for kids even $10,000-$25,000 eliminates this financial burden from parents and allow the family to focus on healing rather than debts

Build Wealth Through Cash Value

Whole life policies accumulate guaranteed cash value over decades. If your child takes out a policy at age 5 by age 25 they could have $10,000-$50,000 in accessible cash value depending on the policy and premium paid. This will become a financial tool for life milestone without requiring a new application or health exam

Protect a Child with Special Needs

Children with disabilities or chronic conditions are often uninsurable as it is. Kids with autism, cerebral palsy or other conditions frequently purchase the coverage to make sure that the protection will be there when the private insurance becomes unavailable.

Real-World Example: The Martinez Family

Sara Martinez made the best decision when she secured a whole life insurance policy for kids for age. She paid $50 per month per child starting at age 4 and six. Today at age 35 and 37 children each have $65,000 in cash value without paying a single additional premium for the last decade. My daughter recently borrowed $15,000 against the policy to find an MBA, repaying it interest free to herself. Her son kept the policy active and now has permanent coverage his family relies on, all because of a decision that is made when they were young.

How Much Does Life Insurance for Kids Cost?

Life insurance for kids is based on the coverage type, amount, child’s age. Here is what you can expect

Term Life Insurance Pricing

A 10 year term life insurance policy providing $100,000 coverage typically costs $10-$25 per month for a healthy child depending on the insurance company. A 20 year term for the same coverage runs $15-$35 monthly. These rates lock in and do not increase even if your child develops health issues.

Whole Life Insurance Pricing

The whole life insurance policy for kids is higher upfront but includes cash value. A $50,000 policy costs $40-$80 per month for a young child while the $100,000 policy runs $80 to $50 monthly. The popular options like Gerber Life Insurance and nationwide offers affordable entry level plans.

Cost Comparison Table

| Coverage Type | Coverage Amount | Child Age | Monthly Cost | Cash Value After 20 Years |

| Term Life (20-year) | $100,000 | 5 | $18–$28 | $0 |

| Whole Life | $50,000 | 5 | $45–$65 | $12,000–$18,000 |

| Whole Life | $100,000 | 5 | $85–$120 | $28,000–$40,000 |

| Term Life (30-year) | $250,000 | 10 | $35–$50 | $0 |

Best Life Insurance for Kids: How to Choose

Selecting the best type of insurance for kids depends on three factors that are your budget, coverage duration needs and financial goals.

If You Want Affordability

Choose a term life insurance for kids policy. This will provide substantial coverage, often $250,000-$500,000 at the monthly cost of $20-$50 this is best if your primary concern is covering the funeral expenses and temporary financial gaps

If You Want Lifetime Protection and Cash Value

A whole life insurance for kids policy builds wealth while protecting your child’s insurability. The higher premium $50-$150 per month includes a savings component that grows throughout their life.

Best Life Insurance Providers for Kids (2026)

| Insurance Company | Best For | Starting Monthly Cost |

| Gerber Life | Affordability and simplicity | $9–$15 |

| Nationwide | Whole life cash value options | $40–$70 |

| MetLife | Large coverage amounts and conversion | $20–$40 |

| State Farm | Bundling with family coverage | $18–$35 |

| Globe Life | Specialized child plans | $12–$25 |

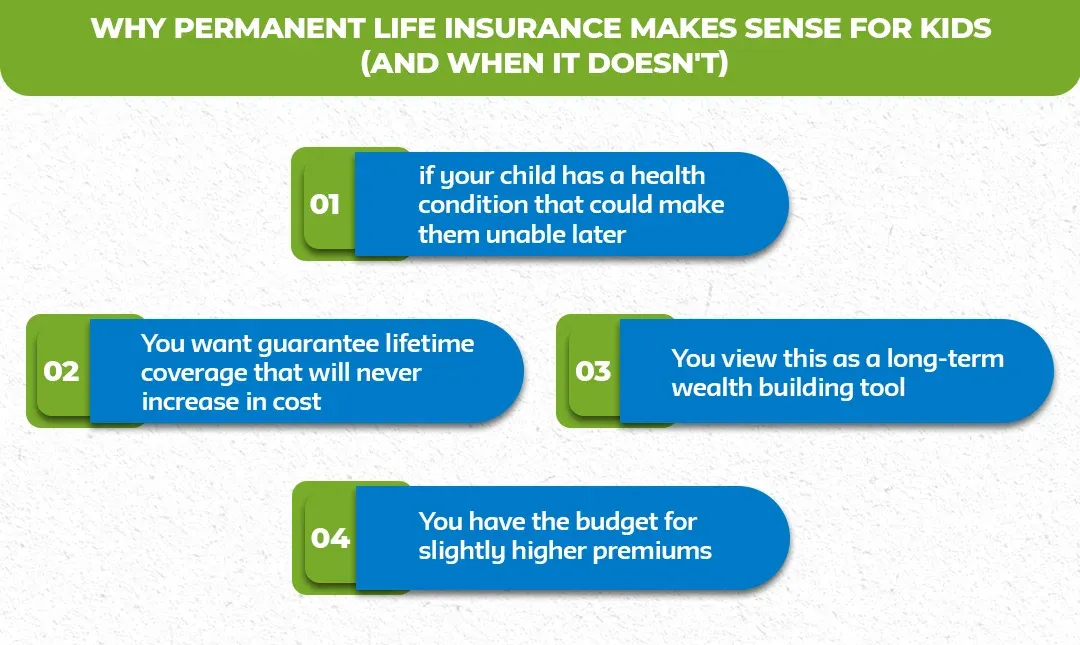

Why Permanent Life Insurance Makes Sense for Kids (And When It Doesn’t)

A whole life insurance worth it for kids? This depends on your financial strategy.

It will make sense

- if your child has a health condition that could make them unable later

- You want guarantee lifetime coverage that will never increase in cost

- You view this as a long-term wealth building tool

- You have the budget for slightly higher premiums

It does not make sense if

- Your only goal is covering the funeral expenses term life insurance is cheaper

- Your child is imperfect health and will likely qualify for competitive rates as an adult

- You cannot comfortably afford the premiums

Special Considerations: Life Insurance for Kids with Disabilities

Children with life insurance for kids with autism, cerebral palsy, sickle cell disease or other conditions face the reduction or extremely high rate from the insurance companies when they reach adulthood. The proactive parent secured coverage while their children are young and healthy guaranteeing protection when they need it.

Some of the insurance companies offer a specialised program with simplified underwriting for children with disabilities. The premiums are reasonable because the child is young, even though a future diagnosis might make coverage unavailable elsewhere.

Life Insurance Options for Single Parents

Single parents often face unique financial pressure. If something happens to you, your child loses income and parental support. Life insurance options for single parents to protect kids strategy typically includes adequate life insurance on your own, a modest policy on your child’s life and a will or trust designating guardianship and financial Resources.

The Bottom Line: Should Your Family Get Life Insurance for Kids?

Life insurance for kids is not a must have for every family, but it is a smart financial decision for most. The combination of low premiums, guarantee rates and long-term protection make it particularly valuable for the families who want to cover funeral costs without that, parents of children with hand conditions, families who are pursuing permanent whole life policies for wealth building and any parent who wants life wrong protection that is locked in now.

Ready to explore your options? Reach out to an independent life insurance agent who can compare the rates from multiple insurance companies for a specific situation. They will help you to understand whether the term, whole life or combination approach makes sense for your family. Without any pressure or commission driven recommendations Find out the quotes available At Mlife Insurance.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.