You got a new job, they handed you a benefit packet and somewhere on page 4 it said AD&D insurance that you are enrolled in automatically. You probably nodded and moved on.

But here is the thing most people never stopped to ask, that is if you die tomorrow from a heart attack like the number one killer in the United States, responsible for 683, 491 deaths in 2024 according to the CDC, would that policy pay your family a single dollar?

The answer in most cases is no.

Understanding accidental death and dismemberment vs life insurance is not a technicality. It is a difference between your family receiving a payout and your family receiving nothing. This guide breaks it all down clearly, so you can stop guessing and make a decision that actually protects the family who depend on you.

What Is the Real Difference Between AD&D and Life Insurance?

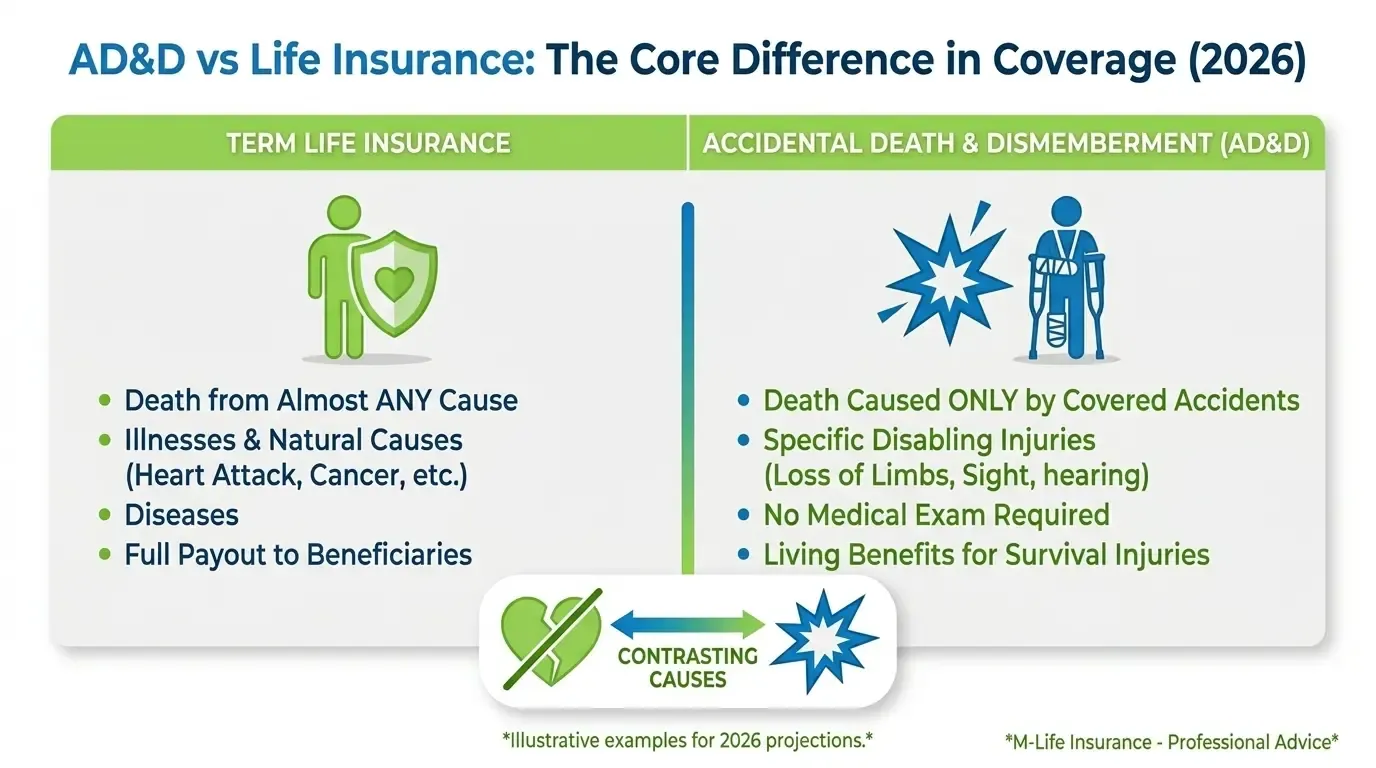

Life insurance pays your beneficiaries when you die from almost any cause. AD&D only pays if your death or injury was caused by a covered accident.

That single distinction is everything.

Life insurance covers death from any cause, whereas accidental death and dismemberment insurance is supplementary policy that only covers death or injury resulting from an accident.

So if you die from cancer, a stroke, diabetes or heart failure, conditions that count for the overwhelming majority of American deaths, your AD&D policy pays nothing. Your life insurance policy pays everything.

AD&D insurance costs less, but it covers only accidental death and injuries, leaving your family unprotected if you die from natural causes.

Think of AD&D as narrowly backup that is useful in the right context, but never substitute for proper life insurance coverage.

How AD&D Insurance Works Compared to Life Insurance

AD&D pay the benefit under two conditions like accidental death, or qualifying accidental injury. Life insurance pays a death benefit under nearly all conditions.

AD&D insurance pays benefits if the insured person dies in an accident such as a car crash, drowning, falling or suffers the loss of limbs, sight or speech. Death and injuries that occurred while the insured was committing a crime, driving under the influence, or participating in high risk activities like skydiving are typically excluded.

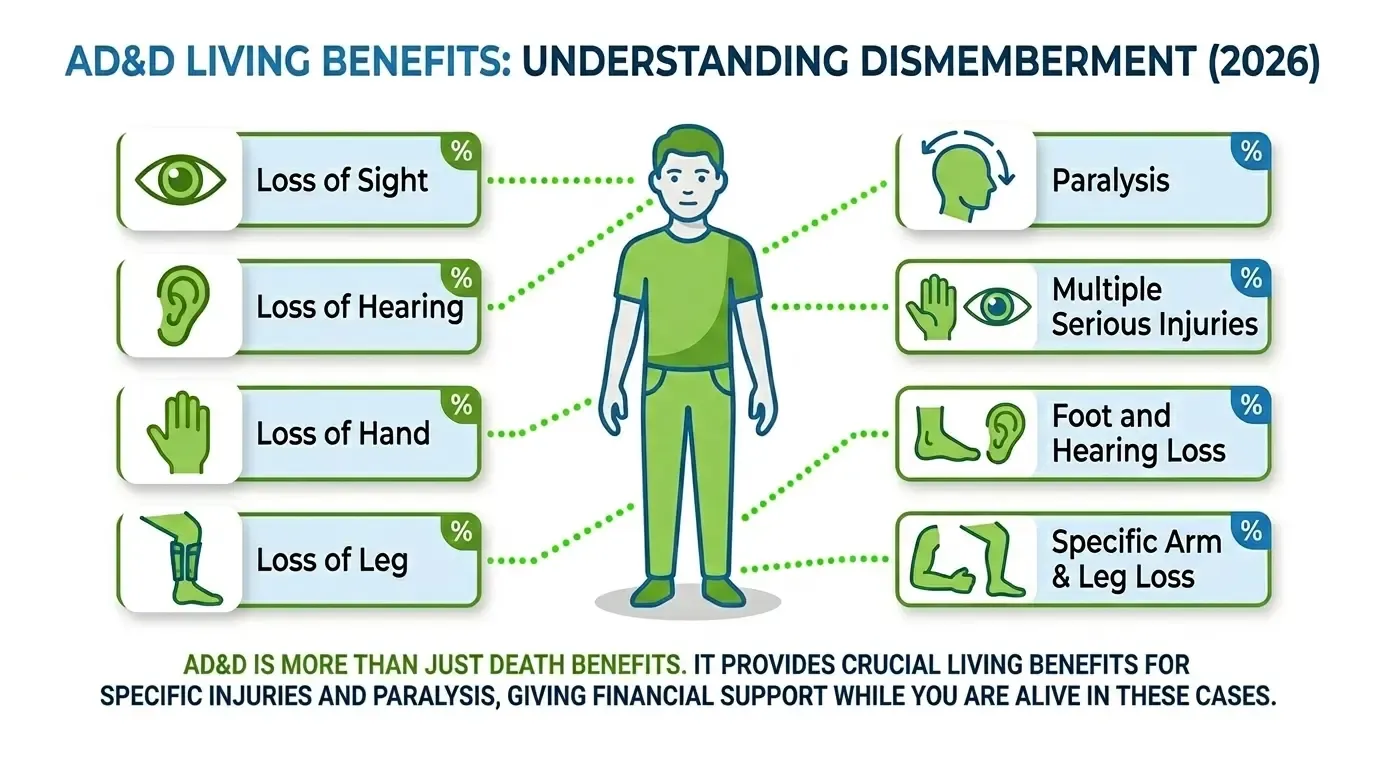

One important feature of AD&D that many people overlook is it provides a living benefit. If you survive an accident but lose a hand, your eyesight or your hearing, AD&D can pay you a percentage of the policy value based on the severity. Life insurance, by design, only pays out at death.

Term Life Insurance vs Accidental Death and Dismemberment: A Cost and Coverage Reality Check

Term life insurance costs more than AD&D, but it protects against the causes of death that are statistically far more likely to affect you.

Consider the numbers. According to the CDC 2024 provisional mortality report, the top three causes of death in the United States were heart disease diseases 683,037 deaths, cancer 619, 812 deaths and unintentional injury 196,488 deaths.

Unintentional injuries, the only category AD&D would broadly address, is ranked third, well behind disease. It means that if your only policy is AD&D, your family is unprotected against the two leading killers in America.

Premium Comparison Table (2026 Estimates)

| Policy Type | Coverage Amount | Monthly Premium (Healthy, Age 35) | What It Covers |

| Term Life (20-year) | $500,000 | $28–$55/month | Death from any cause |

| AD&D (standalone) | $250,000–$500,000 | $5–$15/month | Accidental death & injury only |

| AD&D as rider on life policy | Added to existing policy | $3–$7/month additional | Supplemental accidental benefit |

Supplemental Life Insurance vs AD&D: What Your Employer Actually Gives You

Most of the employers sponsored AD&D is a supplemental ad on, not a primary protection plan. Supplemental life insurance, by contrast, extends your core life coverage and it is a much stronger safety net.

Many employers offer both, and the language can get confusing fast. Here is the key distinction

Supplemental life insurance

Supplemental life insurance is additional term life coverage you can purchase through your employer on top of your basic life benefit. This plan covers death from any cause just like a standalone term life policy. You typically do not need a medical exam for modest coverage amounts.

Employer-sponsored AD&D

Employer sponsored AD&D is usually provided free or at very low cost but it only activates in accidental scenarios. Many employer sponsored AD&D policies end when you leave your job, making personal care decisions are more important than many people realise.

If your employer offers both, supplemental life insurance should be a priority. AD&D can be a smart, low cost addition on top of it not instead of it.

Pros and Cons of AD&D Insurance: Is It Worth Having?

AD&D is worth having as a supplement. It is not worth relying on exclusively.

Where AD&D earns its keep

- Very low monthly cost often five dollars to fifteen dollars per month or employer sponsored for free

- No medical exam is required

- Pay a living benefit for serious injuries, something Term Life cannot do

- Double the payment for your family if an accident causes your death and you also hold a life policy

Where AD&D falls short:

- There is nothing for death by illness, disease or natural causes

- In cases involving or underlying illness, many courts follow a substantial contribution standard; if an underlying medical condition such as diabetes contributed to injury, AD&D coverage may be denied.

- Coverage amounts are generally lower, AD&D coverage amount usually range from $10,000-$500,000, typically lower than what life insurance policies offer

- Policy can be lapsed when you change jobs if employers sponsored.

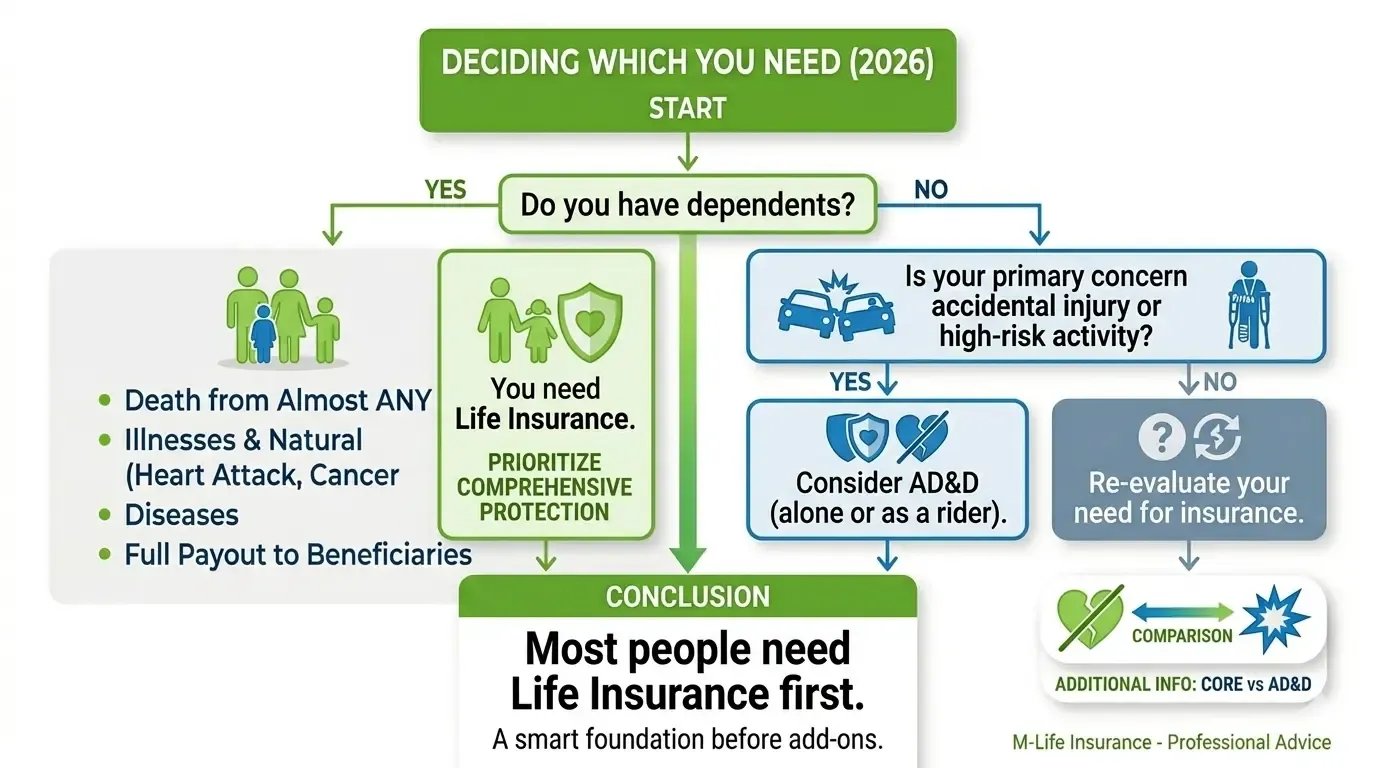

Which One Do You Actually Need? AD&D, Life Insurance, or Both?

If you have a dependent who relies on your income, you need life insurance first. AD&D is a smart affordable add-on never the primary plan.

Here is the simple decision framework

You need term life insurance if you have a spouse, children, or anyone who depends on your income. Also if you carry a mortgage or significant debt or you can’t guarantee coverage regardless of how you die.

AD&D alone may be sufficient only if you have no dependence and only need coverage for accidental injury, you are in a high risk occupation and additional accident specific protection on top of existing life insurance or you cannot qualify for the additional life insurance and need some coverage.

You should have both

- if you want to maximise your family payout in the event of an accidental death

- You want a living benefit protection AD&D provides for serious injuries

- You can afford the more additional premium for an AD&D rider

Final Thoughts: Don’t Let the Wrong Policy Leave Your Family Unprotected

You now know more about this topic than most people ever learned before buying coverage. The core principle is very simple, that is life insurance and AD&D serve different purposes and one cannot replace the other.

If you found this guide helpful and want to understand your coverage options better, the team at M-life Insurance can help you review your current policies and find the right combination of term life and AD&D coverage for your situation without any pressure to buy. Getting informed is the first step. Getting covered is the next one.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.