There are so many people who are always ending up over paying for the term coverage are they are waiting for weeks for the process they have gotten online in minutes. They are always picking a life insurance that is based on the brand name alone, not on the other things.

New York life is one of the most recognized life insurance names in the industry and that reputation is very well earned but it is not automatically the right fit for every buyer. Before you talk to an agent, this guy will help you to know exactly what you are getting and what it cost.

What Is New York Life Insurance Company?

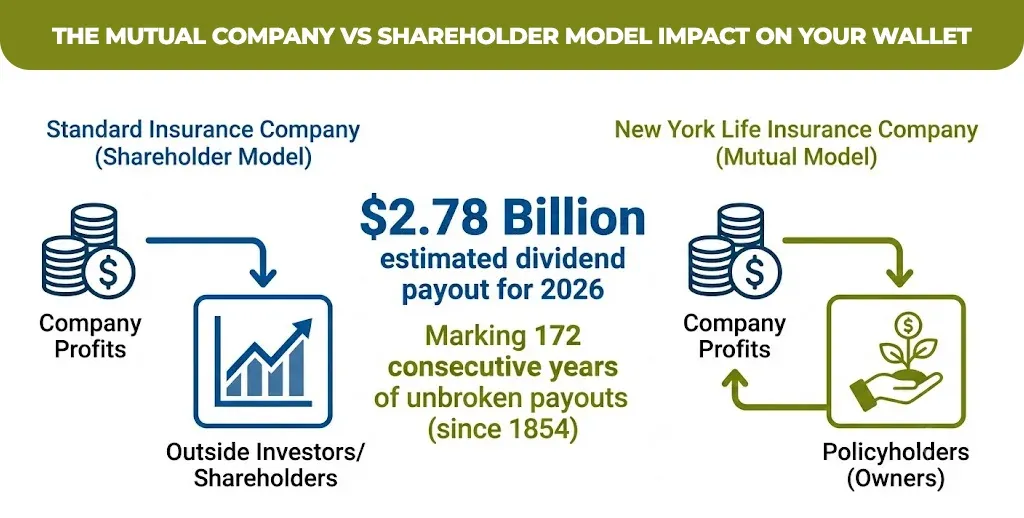

The New York life insurance company is the largest mutual life insurance company in the United States. The company is founded in 1845 and the headquarter is in New York City. As a mutual company, it has no shareholders. The policyholder effectively own it and the profits are returned to the annual dividend rather than paid out to the outside investor.

That structure matters because New York life insurance has paid a dividend to eligible policyholders every year since 1854, including through the great depression and both world war. For 2026, the company is confirmed and estimated $2.78 billion dividend payout and marketing its 172nd consecutive year of the dividends.

New York Life Insurance Reviews: What the Ratings Actually Say

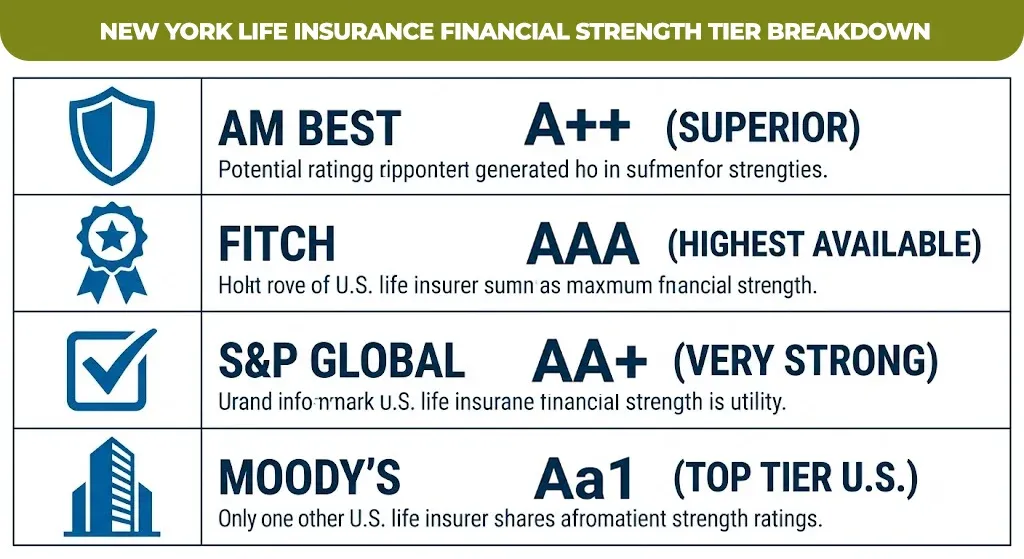

The New York life holds the highest financial strength rating that is available from every major rating agency at once. The distinction is only one other US insurance shares. That combination is very rare and it is worth understanding before you compare it to the cheaper alternative plans.

| Rating Agency | New York Life Rating | What It Means |

| AM Best | A++ (Superior) | Highest possible rating; strongest claims-paying ability |

| S&P Global | AA+ | Second-highest tier; very strong financial security |

| Moody’s | Aa1 | Among the highest ratings for a U.S. life insurer |

| Fitch Ratings | AAA | Highest available rating |

Talking about the consumer site, the New York life insurance reviews are generally strong but mixed on price. One 2026 industry survey found that the company earns a 3.94 out of five customer satisfaction score. With especially the high marks for the renewal loyalty and the trust, but noted it’s premium run above the average at lower coverage amount. All this data is according All this data is according to MoneyGeek’s 2026 New York Life review. It’s NAIC complaint index also sits well below the industry benchmark that is the solid sign of consistent claim handling.

New York Life Whole Life Insurance: How It Works

The New York life insurance whole life insurance plan build cash value that is on the tax deferred basis with a guaranteed level premium for as long as you are paying the premiums and on the policy. Because it’s participating the policy, it’s eligible for the annual dividend though those dividends are never guaranteed and also depending on the companies performance each year.

The company also offers limited pay whole life insurance options, letting you to finish all the premium payments in 10 or 20 years while keeping the lifetime coverage active. There’s appeals to buyers who paid off retirement even though the death benefit and the cashback your growth continue for life.

New York Term Life Insurance: Cost and Coverage Limits

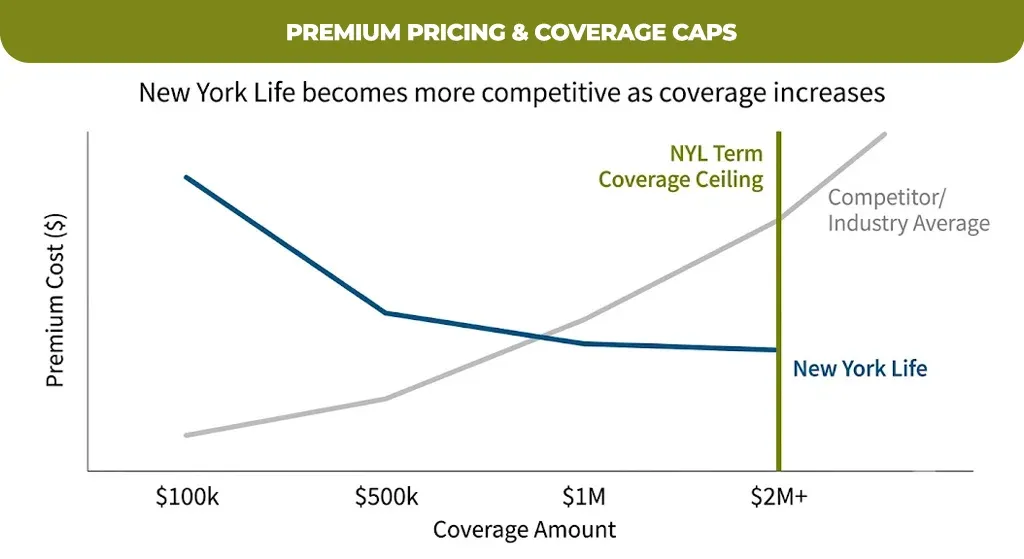

New York lifetime life insurance is priced above the market average at the lower coverage amount but becomes more competitive as the coverage increases. For a 40-year-old non-smoker in the average health who is buying a 20 year term policy with $500,000 in coverage, published 2026 rate data shows the following charges.

| Insurer | Monthly Rate (Female) | Monthly Rate (Male) |

| New York Life | $47 | $58 |

| Industry average (comparable insurers) | Lower at this coverage tier | Lower at this coverage tier |

The New York term life insurance caps out at two dollar million in the coverage and 20 year term lens. While the competitors offer up to $10 million and the terms as long as 40 years. If you need a large policy or the longer-term than ceiling is worth checking before you apply for the plan.

New York Life Insurance Policies Beyond Life Insurance

The New York life insurance policies extend well past whole and a life insurance coverage. The company also offers the following.

- The company offered New York life disability insurance that protect the income of illness or injury that prevent you from working.

- The long-term care instruction, is covering the extended care cost later in your life.

- The company gave you New York life health insurance products that are offered through affiliated subsidies.

- The annuities, these include the immediate and deferred income annuities that are backed by the same top tire financial reading.

- Can you wear the variable universal life for the buyers who won flexible premiums or the investment linked cash value growth.

How to Get a New York Life Insurance Quote

You cannot get a new York whole life insurance quote online through instant self service tools. Every policy is sold through the company network of carrier agent so getting the code means scheduling a conversation not filing out a five minute form.

This also means that underwriting is more thorough. Most of the policies above $100,000 require a full medical exam. That comes with a limited expectations for the certain simplified issue products that are offered in partnership with AARP.

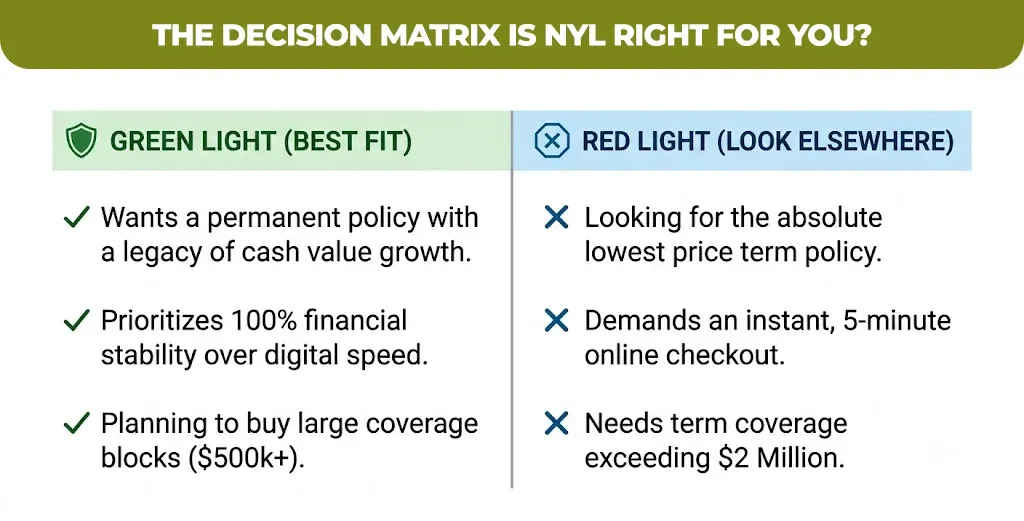

Who New York Life Insurance Is Actually Best For

New York life insurance is a strong fit if you want to buy the permanent coverage, this is the company with an unbroken dividend history so it is better if you want to purchase a large policy where it’s great to become more competitive. It’s a weaker option if you want the cheapest possible term policy, and online only buying experience or the coverage that is above it’s $2 million term cap.

Choosing a legacy mutual insurance company and the faster digital option totally depends on what you value most like the price, speed and long-term stability. If you want to see how New York life rates and the policy structure stack up against other insurance companies for your specific age and the covering then the team at Mlife Insurance can pull the real court side-by-side so you are comparing the actual number is not just a brand name.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.