When someone passes at a young age and has a mortgage left, has kids going to kindergarten, and a wife who relies on him. An instant thought comes to your mind. What will happen to my family when I die? Then you start planning to buy life insurance. Among so many options available, 15-year term life insurance would be the best option for you. In this guide, we’ll explain everything about 15-year term life insurance, including its benefits, cost, rates, and how it compares with other term lengths. We’ll also touch on the best options for seniors.

What is a 15-Year Term Life Insurance Policy?

You can clearly understand by its name that the 15-year term life insurance will cover you for a fixed time period that is 15 years. The insurance company will pay a death benefit to the family. If the policyholder passes away within 15 years of the policy. If the person is still alive after 15 years, the policy will automatically expire, and there will be no payout. For that, you have to renew or convert the policy.Is a 15-Year Term Life Insurance Policy Right for You?

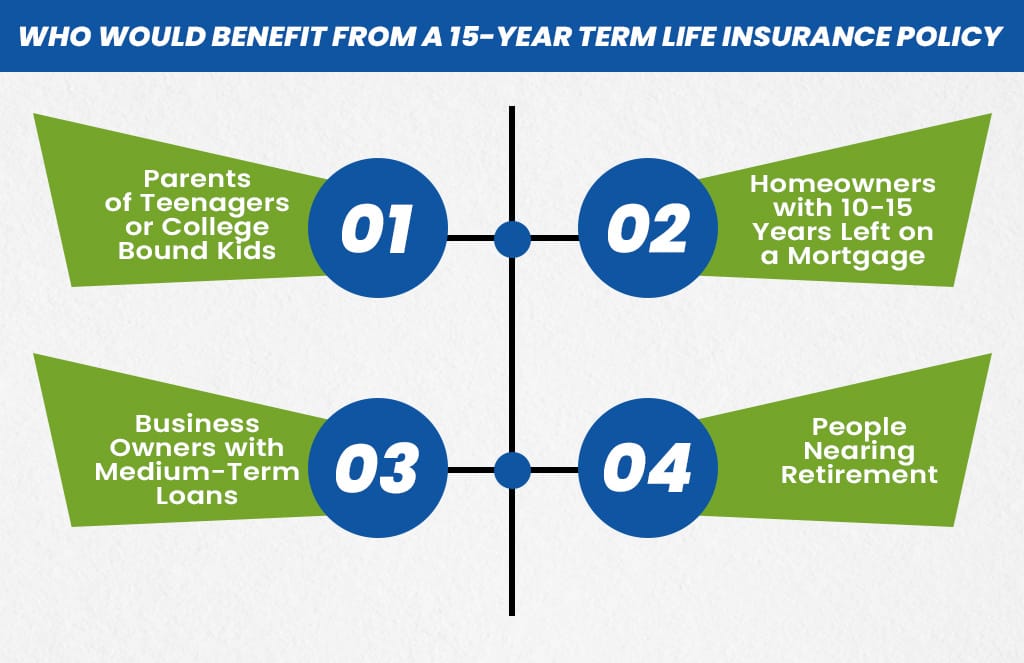

When buying a 15-year term life insurance policy, you must ask yourself some questions like:How much debt do you currently have?When will your children become financially independent? Will my family struggle financially if I pass away in the next 15 years? These thoughts will help you to make a better decision on whether a 15-year term is best for you or not.Who would benefit from a 15-year term life insurance policy?

Most people buy 15-year term life insurance when they are in their 40s or 50s. This insurance policy will cover most of the financial responsibilities, like paying bills, rent or mortgage, loans, and supporting family members.A couple in their 40s, both doing jobs to cover the daily expenses, having kids, their education, and paying the mortgage. All these expenses are relying on their two jobs. Now they don’t need any lifelong insurance coverage. They just want to protect their kids and expenses during this important time. A 15-year term life insurance is the best option for them, offering them stress-free life, covering the mortgage, living expenses, and kids’ education. If one of them passes away unexpectedly. This insurance will provide focused financial security. Other than this, some age groups also benefit from 15-year term life insurance

1. Parents of Teenagers or College-Bound Kids

15-year term life insurance is best to protect your family’s money during the years of your child’s education2. Homeowners with 10-15 Years Left on a Mortgage

This insurance will make sure that your mortgage is paid off if something happens to you before the term ends.3. Business Owners with Medium-Term Loans

Life insurance can cover a business loan or act as a key person policy for business continuity.4. People Nearing Retirement

A 15-year term will provide you with extra protection until you reach retirement age.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.