By the wrong type of life insurance policy, one of two things will happen. Either you overpay for decades on the coverage that you did not need or your family find out at the worst possible moment that the cheap policy you bought expires years before you die.

Both mistakes are very common and both come from the same route problem and that is agent often lead with the policy that will pay them the highest commissions, not the one that will fit your actual situation. Understanding the real differences between the policy types will take about 10 minutes and it can save thousands of dollars over the life of the policy.

What Are the Main Types of Life Insurance?

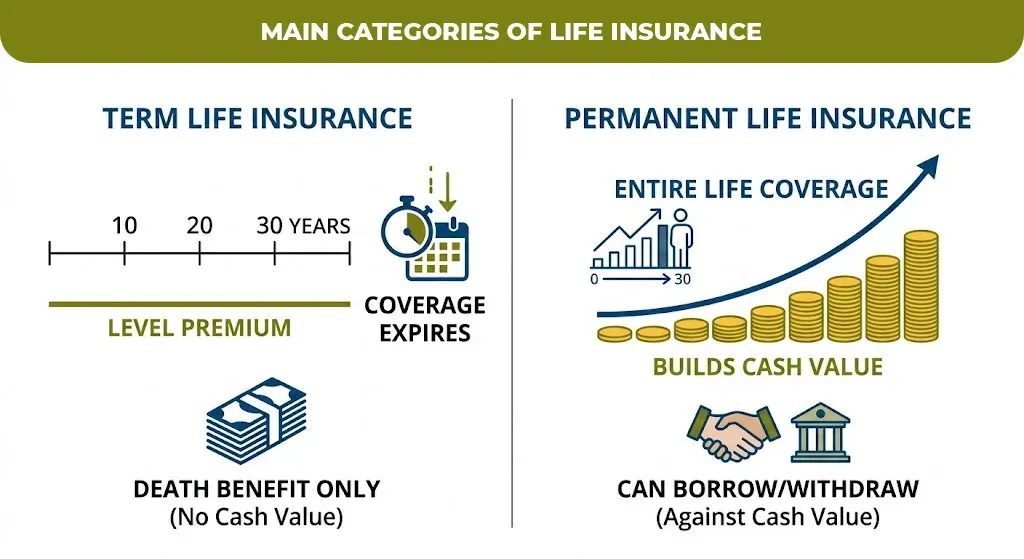

There are two important categories like the one is term life insurance and the other is permanent life insurance. Everything else, universal, variable, financial expense, is the variation within one of those two buckets.

Term life insurance cover for a fixed that is used 10, 20 or 30 years and it pays nothing if you outlive the term. The permanent life insurance on the other hand covers you for your entire life as long as you are paying your premiums and also it builds cash value you can borrow against withdrawal. If our policy sounds complicated then it is almost always a valuation of permanent coverage like term life insurance is intentionally simple.

Term Life Insurance: The Default for Most Families

Term life insurance is a very right starting point for most of the people because it delivers the highest death benefit for the lowest monthly cost. You can pick a term then that is often, 20, 30 years and the coverage amount then the premium stays level for that entire time.

That disadvantages the coverage ends when the term ends. If you still need protection at that point then a new policy at your older age can cost you more and some health conditions make you uninsurable at the standard rates.

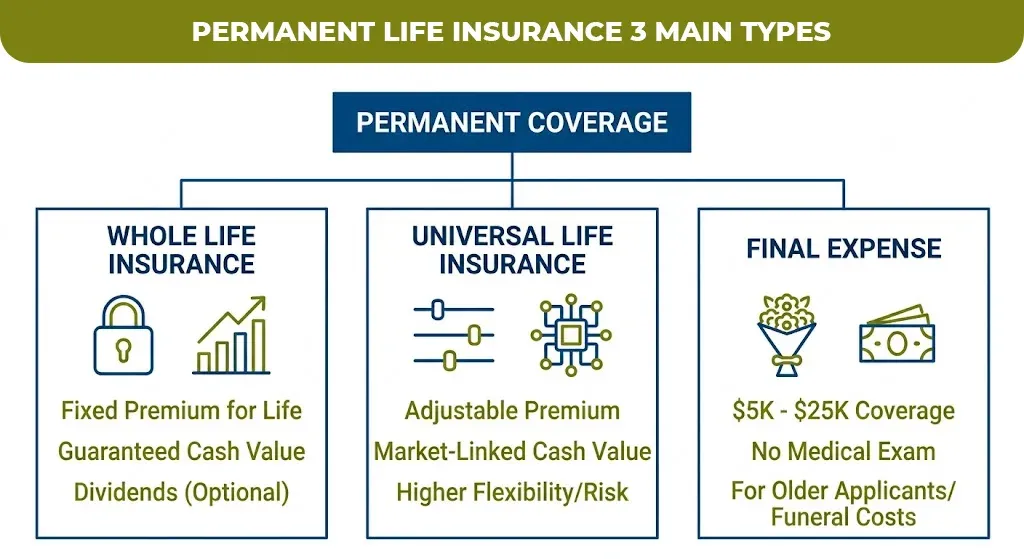

Whole Life Insurance: Lifetime Coverage With a Savings Component

Whole life insurance is the type of life insurance policy that never expires and it also bill guaranteed cash value overtime. You can borrow this against while you are alive. The premiums are fixed for life and so many policies paid dividends on the top of the guaranteed growth.

Whole life insurance makes sense for the permanent obligations and these are estate taxes, a special need dependent or a forced savings vehicle for someone who has already maxed out a retirement account. It is usually the wrong choice for a 30 year old who just need income replacement during their working years.

Universal Life Insurance: Flexible Premiums, More Risk

Universal life insurance is a permanent coverage with the adjustable premiums and a cash value account that can earn interest, giving you more control as compared to whole life but less predictability. The universal life ties growth to the market index with the downside protection while the variable life insurance invest the cash value directly in the market funds with no floor.

That flexibility cut both ways. If you fund the policy of the cash value account under performed, the policy and laps. It means that you lose coverage entirely and sometimes without much warning unlike the whole life guaranteed structure.

Final Expense and Group Life Insurance: The Smaller Categories

Final expense insurance is a small and simplified issue whole life insurance policy. It is generally $5000-$25,000 in coverage. The plan was especially designed to cover the funeral expenses and small debts often with no medical exam required. It is built for the older applicants who cannot qualify for the larger traditional policies.

Group life insurance is the coverage that is provided through an employer usually one or two times your annual salary at little or no cost to you. It is valuable but clearly sufficient on its own and it generally disappears the day you leave the job. Which is the single most overlooked gap in most of the people’s coverage.

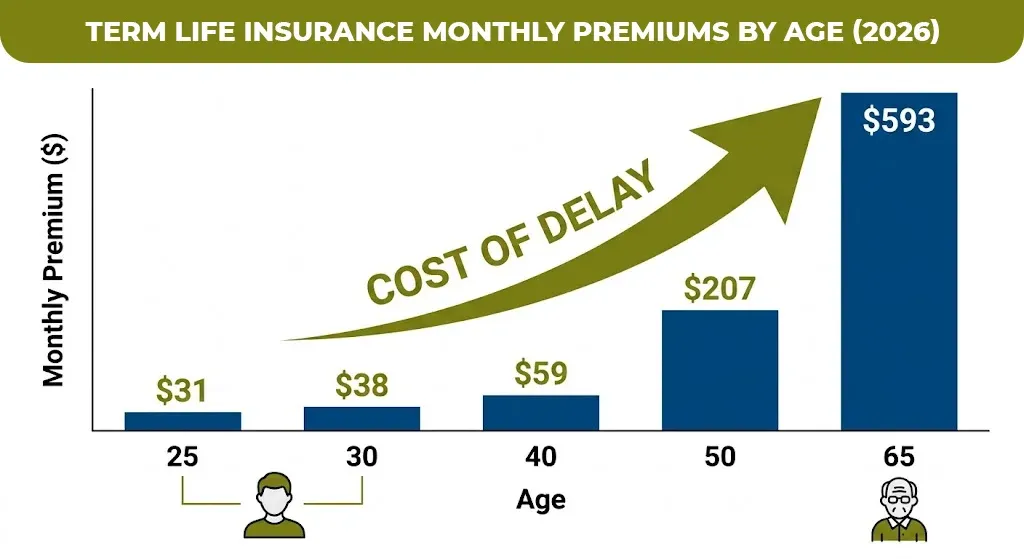

Term Life Insurance Rates by Age

Age is the single biggest factor in what you have paid. Which is why waiting to buy the term life insurance coverage is one of the more expensive delays in personal finance.

| Age | Monthly Premium (20-yr, $500K, nonsmoker) |

| 25 | $31 |

| 30 | $38 |

| 40 | $59 |

| 50 | $207 |

| 65 | $593 |

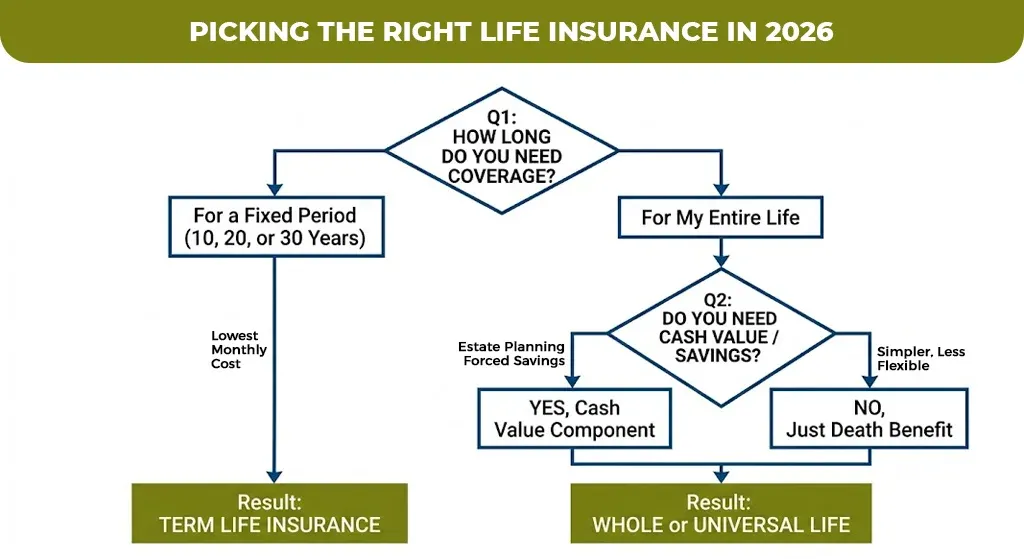

How to Choose the Right Type of Life Insurance

Start with the questions of policy needs to answer, not the product and agent is pushing. Make sure to ask three things one is how long do you actually need the coverage? Do you need the cash value feature or you are completing savings with insurance? And can you comfortably afford the premium for the full term without lapsing the policy?.

A Real-World Example: Choosing Between Term and Permanent

Marcus is 34, married, with two kids and a mortgage. His main financial risk is his family losing his income and struggling with the mortgage if he dies in the next 20 years, not a lifetime need for coverage.

A 20-year term policy for $750,000 covers exactly that risk window at roughly $45 to $55 a month, matching the mortgage payoff timeline. Buying a whole life policy instead would cost him several hundred dollars more per month for a death benefit he doesn’t need past retirement, money that could otherwise go toward his 401(k) or his kids’ education fund.

His situation would change if he had a permanent dependent or a large estate tax. That’s when permanent coverage starts to make sense over term.

Every family’s situation is different, and the right policy type depends on your age, dependents, and how long you actually need coverage to last. If you’d like help comparing term and permanent options side by side for your specific situation, Mlife insurance can walk you through real 2026 quotes with no obligation to buy.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.