There are so many people who assume that what is available is more than enough for them. They sign one, be responsible and then move on.

Then they die and their family spends nine months in probate court, watching 3% to 8% of the state disappear into attorney fees and “cost. On a $500,000 estate, that is up to $40,000 gone before a single heir sees a dollar.

If you are trying to figure out the difference between a living trust vs well then you are already asking the right question. Here is everything you need to decide fast.

What Is the Real Difference Between a Living Trust and a Will?

A will is a legal document that says who will get your stuff after you die. Simple, cheap, and widely misunderstood. The catch is that it only works through the probate court, which is a public, time-consuming, and often expensive process.

A revocable living trust does the same job but without the court. You transfer your assets into the trust now, while you’re alive. When you die, your successor trustee distributes everything privately, often within weeks.

The core difference: A will goes through probate. A living trust doesn’t.

That single difference changes everything about how your estate settles the cost, the timeline, the privacy, and the stress on your family.

Living Will vs Living Trust: These Are Not the Same Thing

This is one of the most common mix ups in estate planning, and it can cost you.

Living Will

A living will, that is also called an advanced healthcare directive is the medical document. This medical document will tell the doctors that what to do if you are incapacitated and cannot speak for yourself no matter to use it for the life support. This document has nothing to do with the distributing assets.

Living Trust

A living trust is a financial and estate planning document. It controls what happens to your property, savings, and investments when you die or become incapacitated.

You may need both. But they do completely different jobs. Confusing them leads people to think they are covered when they’re not.

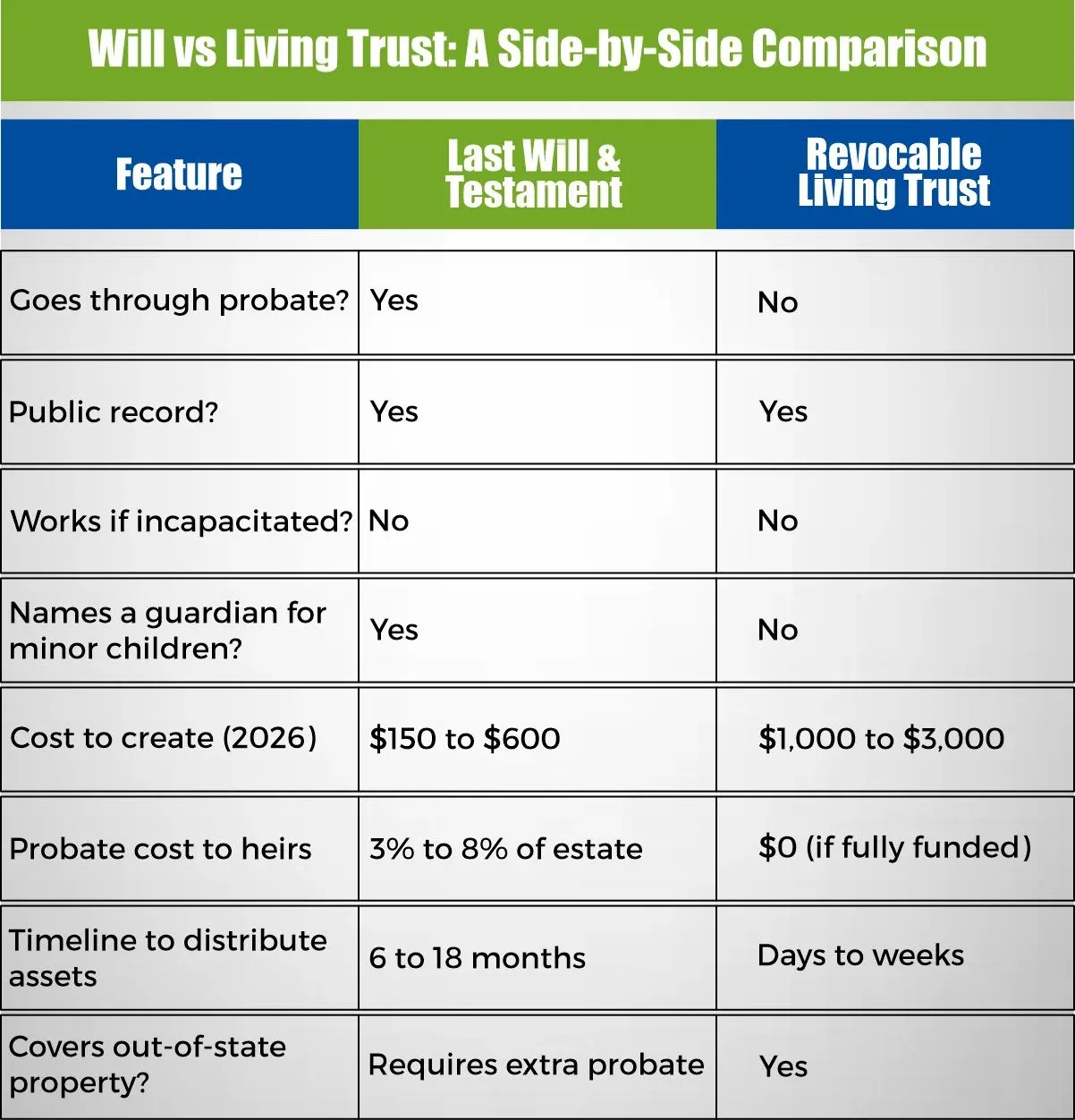

Will vs Living Trust: A Side-by-Side Comparison

| Feature | Last Will & Testament | Revocable Living Trust |

| Goes through probate? | Yes | No |

| Public record? | Yes | No |

| Works if incapacitated? | No | Yes |

| Names a guardian for minor children? | Yes | No |

| Cost to create (2026) | $150 to $600 | $1,000 to $3,000 |

| Probate cost to heirs | 3% to 8% of estate | $0 (if fully funded) |

| Timeline to distribute assets | 6 to 18 months | Days to weeks |

| Covers out-of-state property? | Requires extra probate | Yes |

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.