You found the term “max funded IUL” in a financial video, a sales presentation, or a Google search. Now your screen is full of confusing illustrations, insurance jargon, and agents who seem more excited than your accountant should ever be.

Before you sign anything or dismiss it entirely, here is what you actually need to know. A max funded IUL is not a scam and it is not a miracle. It is a specific funding strategy inside a permanent life insurance policy that, when structured correctly, can generate tax-free retirement income with zero market loss risk.

The problem is that most people encounter it in the worst possible way like through a sales pitch designed to close, not educate.

What Is a Max Funded IUL and How Does It Work?

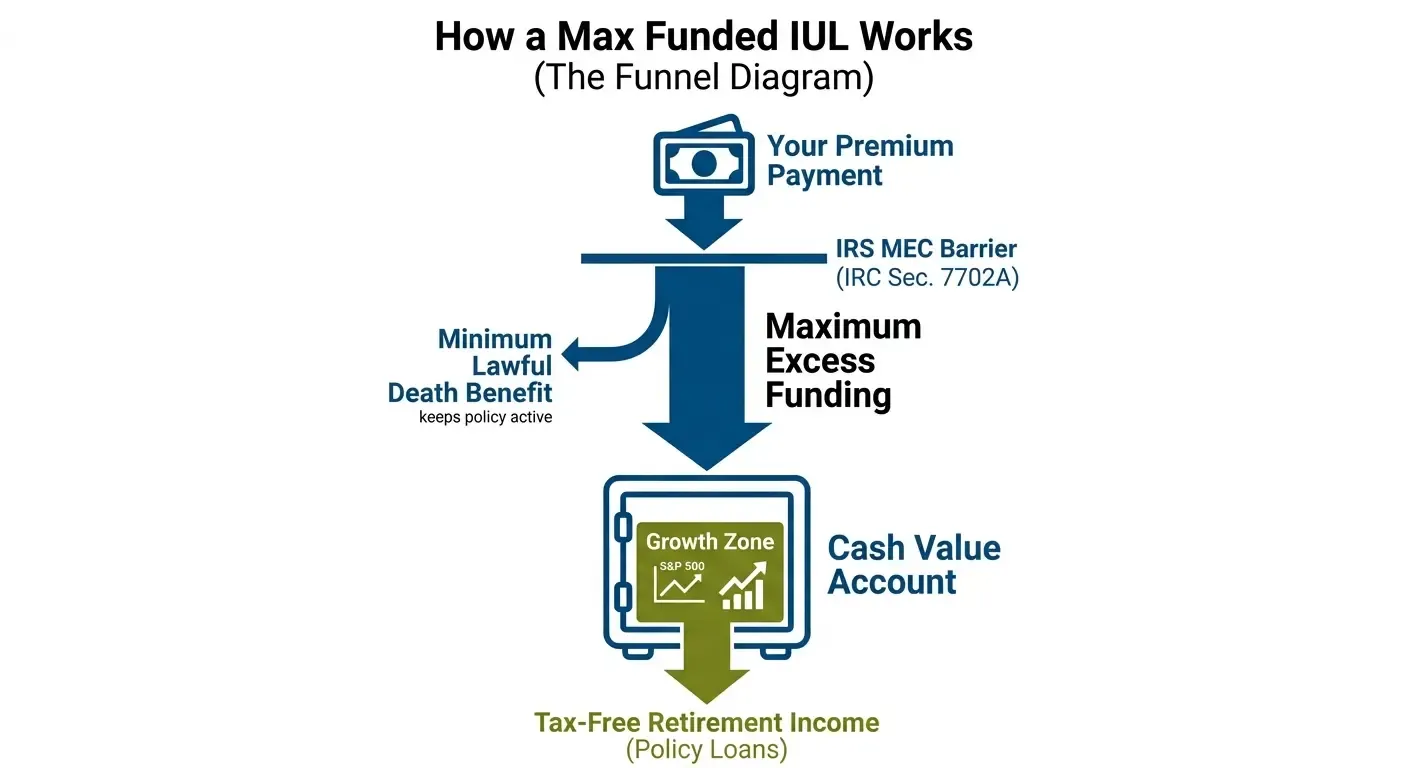

A max point IL is an index universal life insurance policy that is funded to the maximum amount the IRS allows without triggering what is called modified endorsement contract. The IRS governs this under IRC Section 7702A.

Here is the main idea. A standard life insurance policy asks you to pay the minimum needed to keep coverage active. A max funded IUL flips that completely. You pay the most the IRS will allow, with the least death benefit the law requires, so that the excess premium flows directly into a cash value account that grows tax-deferred.

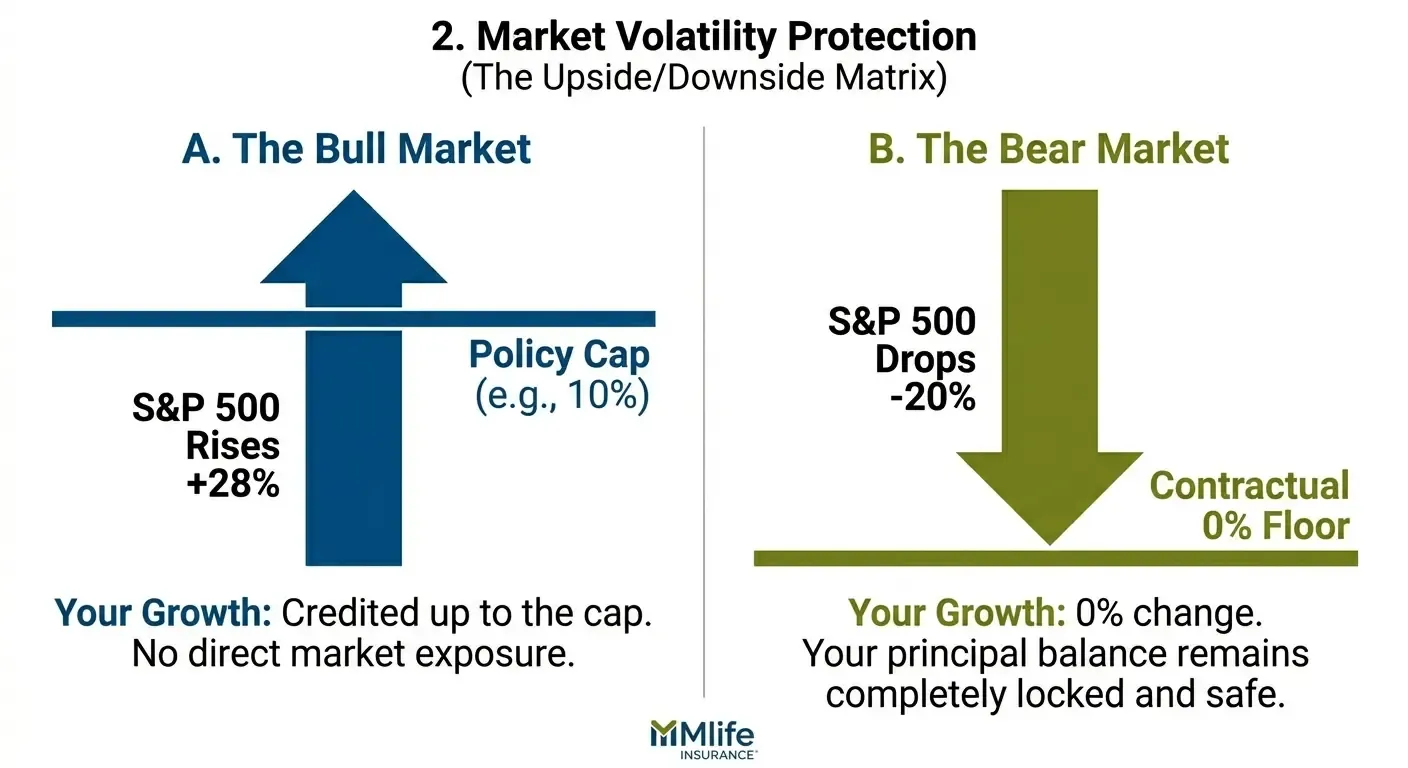

That cash value is linked to the performance of a stock market index, typically the S&P 500, but your money is never directly invested in the market. The insurance insurance company uses options contracts to credit interest based on index movement. When the index rises, your account is credited up to a cap that is commonly 9% to 11%. When the index falls, a contractual 0% floor protects your balance. You simply earn nothing that year instead of losing money.

The result over time is a cash value account that can be accessed through policy loans during retirement, which the IRS treats as income-tax-free.

Max Funded IUL vs 401k: Which Builds More Wealth?

Neither option wins in every situation. The right answer depends entirely on your income level, tax situation, and how close you are to retirement.

Here is a direct side-by-side comparison using 2026 numbers:

| Feature | Max Funded IUL | 401(k) |

| Annual contribution limit | No IRS cap (governed by MEC threshold) | $24,500 ($32,500 if 50+) per IRS 2026 limits |

| Tax on contributions | After-tax (no deduction) | $24,500 ($32,500 if 50+) per IRS 2026 limits |

| Tax on withdrawals | Tax-free via policy loans | Taxed as ordinary income |

| Required Minimum Distributions | None | Mandatory starting at age 73 |

| Market loss protection | 0% floor (no loss years) | Full market exposure |

| Employer match | No | Yes (if offered) |

| Access before 59.5 | Flexible (policy loans, no penalty) | 10% early withdrawal penalty |

| Estate benefit | Death benefit passes tax-free | Subject to income tax by heirs |

The case for a max funded IUL is strongest when you are a high earner who has already maxed out your 401(k) and Roth IRA. The 401(k) distributing $49,000 per year in retirement generates a tax bill at your ordinary income rate. At 24%, that is nearly $12,000 per year in taxes. The same amount distributed through policy loans from a properly structured IUL arrives tax-free, according to Insurance Geek’s 2026 IUL vs 401k analysis.

The case for the 401(k) is strongest when you get employer matching, your current tax rate is high, or you simply cannot commit to premium payments for 10 or more years.

Max Funded IUL Pros and Cons: The Honest List

Most articles on this topic lean one way or the other. Here is the full picture without the spin.

What works in your favor

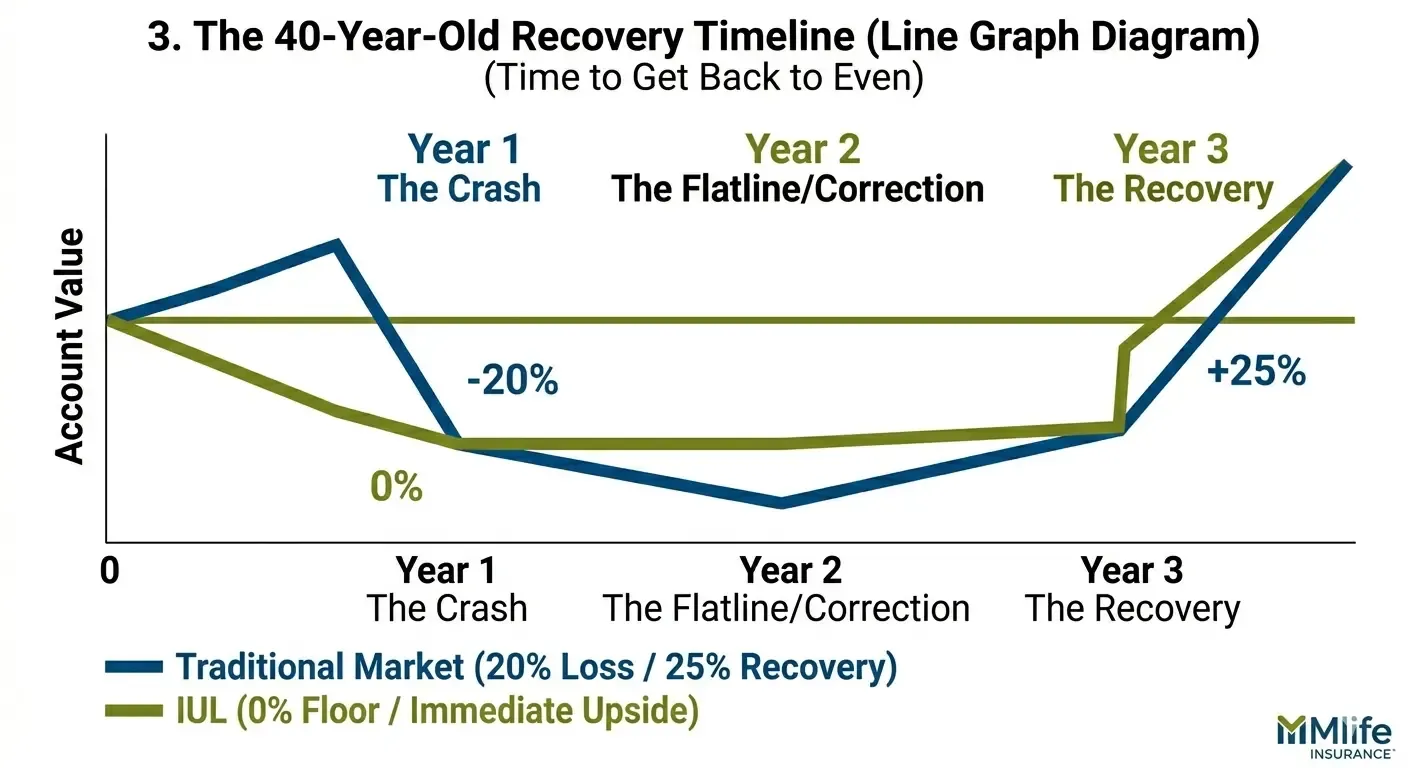

The 0% floor is a genuine structural advantage. In 2026, with persistent market volatility, the ability to never lose ground in a down year is worth something real. A 40-year-old who suffers a 20% market loss in a traditional account must recover 25% just to get back to even. In an IUL, that year is simply $0 gained, and growth continues from the same balance the following year.

There are no IRS contribution limits beyond the MEC threshold tied to your death benefit. For high earners blocked out of Roth IRA contributions, the income phase outs begin at $150,000 single / $236,000 married in 2026 per IRS Roth IRA guidelines, a max funded IUL is one of the few remaining tax-free accumulation vehicles available.

There are no required minimum distributions forcing taxable withdrawals in retirement.

What works against you

The internal cost of insurance increases as you age. In the early years of the policy, a meaningful portion of your premium covers insurance charges before it reaches the cash value account. These costs compound over time if the policy is not properly funded and monitored.

S&P 500 caps in the 9% to 11% range mean you miss out on strong bull market years. If the index returns 28%, your account is credited at the cap. Dividends from index funds, which historically account for roughly 1.5% to 2% of total returns annually, are also not included in IUL crediting.

Illustrations provided by agents are not guaranteed. They are projections based on assumed cap rates that carriers can and do adjust.

Max Funded IUL for Retirement: Who Should Actually Consider It?

A max funded IUL is not for everyone. It is a tool that fits a specific financial profile, and being honest about that profile matters.

You are a strong candidate if:

- You can earn $150,000 or more annually and these prices are locked out of direct Roth IRA contributions

- You have already maxed out your 401(k) and want additional tax advantaged accumulation

- You have a 10 to 20-plus year horizon before you need the income

- You can commit to consistent premium payments without financial strain

- You want retirement income that does not count against Social Security taxation thresholds or trigger Medicare premium surcharges

You are not a good candidate if:

- You have not yet maxed your 401(k) match (free employer money always comes first)

- Your income is below $100,000 (the cost structure makes it less efficient at lower funding levels)

- You may need access to the cash within the first five years (surrender charges apply)

- You are within 10 years of retirement (not enough time for cash value to outpace early costs)

According to Finance Fact Base’s 2026 guide on maximum funded IUL, the product is best suited for high-income earners who have already exhausted conventional tax-advantaged options, not as a replacement for them.

How a Max Funded IUL Calculator Works (and What to Watch For)

A max funded IUL calculator generates a policy illustration showing projected cash value growth, death benefit amounts, and potential loan income over time.

Before trusting any illustration, ask these three questions:

What credited rate is being assumed?

Many illustrations use 6% to 7.5%. That is not unreasonable historically, but carriers can lower caps at any time, which changes the actual credited rate. Ask to see illustrations at 4% and 5% as well.

What are the internal policy charges?

Cost of insurance, administrative fees, and premium load fees reduce the effective return. A policy with high internal costs at a 7% assumed rate may underperform a lower-cost policy at 6%.

Is the carrier’s cap history stable?

Some carriers have steadily lowered caps over the past decade. Others have maintained them. This is one of the most important due diligence questions to ask before selecting a policy.

Is a Max Funded IUL Worth It in 2026?

For the right person, yes. For the wrong person, it is an expensive, inflexible product that will frustrate you for 20 years.

The honest answer is that a max funded IUL works best as a third or fourth layer of a retirement strategy, not the foundation. Max your 401(k) match first, fund your Roth IRA if eligible, build an emergency fund, and then evaluate an IUL for supplemental tax-free income if you still have capacity to save above those thresholds.

If that description matches your situation and you want to understand exactly how this strategy would work with your specific numbers, the right next step is a policy illustration from a specialist who does not have a single-carrier agenda.

A Note From Mlife Insurance

If you are weighing whether a max funded IUL fits your retirement picture, an honest conversation with someone who has run these numbers across dozens of clients is worth more than any article.

At Mlife Insurance, we help people compare policy structures, understand real costs, and make decisions that actually match their financial goals, not just an agent’s quota. There is no pressure and no obligation.

Talk to a specialist at Mlife Insurance and get a personalized illustration

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.