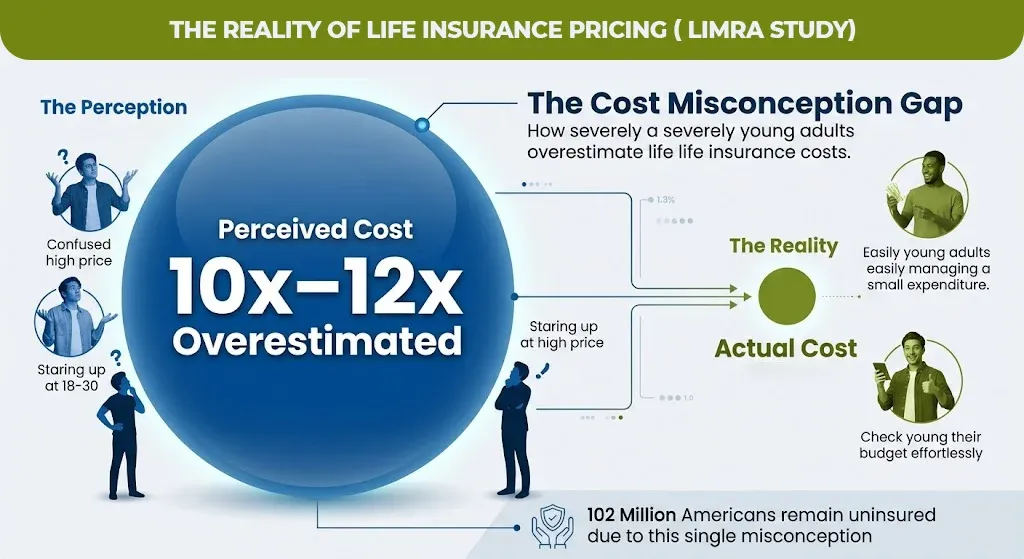

Most people guess what life insurance costs. According to the 2025 LIMRA Insurance Barometer Study, healthy adults aged 18 to 30 overestimate the price of a $250,000 term policy by 10 to 12 times its actual cost. That single misconception is why approximately 102 million Americans are either uninsured or underinsured today.

The risk is not that life insurance is expensive. The risk is that you never got an accurate life insurance quotation, made an assumption, and moved on leaving your family exposed to a financial gap that no amount of regret fixes after the fact.

Here is exactly what a quote costs, what shapes it, and how to get one without giving away more information than you need to.

What Is a Life Insurance Quotation and What Does It Actually Show You?

A life insurance quotation is a personalized premium estimate based on your age, health, coverage amount, and policy type. It is not a contract and not a commitment. It is a number the insurer calculates based on your risk profile to tell you what you would pay monthly or annually for a specific policy.

The quote reflects two things simultaneously: how much the insurer thinks you might cost them, and how competitive they are against other carriers for your profile. That is why the same person can get quotes ranging from $28 to $54 per month for identical coverage just by approaching different companies, a finding confirmed by InsuranceGeek’s 2026 data on rate class differences.

Getting a quote is the only way to know that what is your actual number. Estimate from the friends, calculator and the industry averages will give you a ballpark. A personalized quotation will give you a decision ready figure.

Term Life vs. Whole Life: What Your Quotation Will Look Like

The single biggest factor in what your quotation returns is policy type. Most buyers are surprised by the gap.

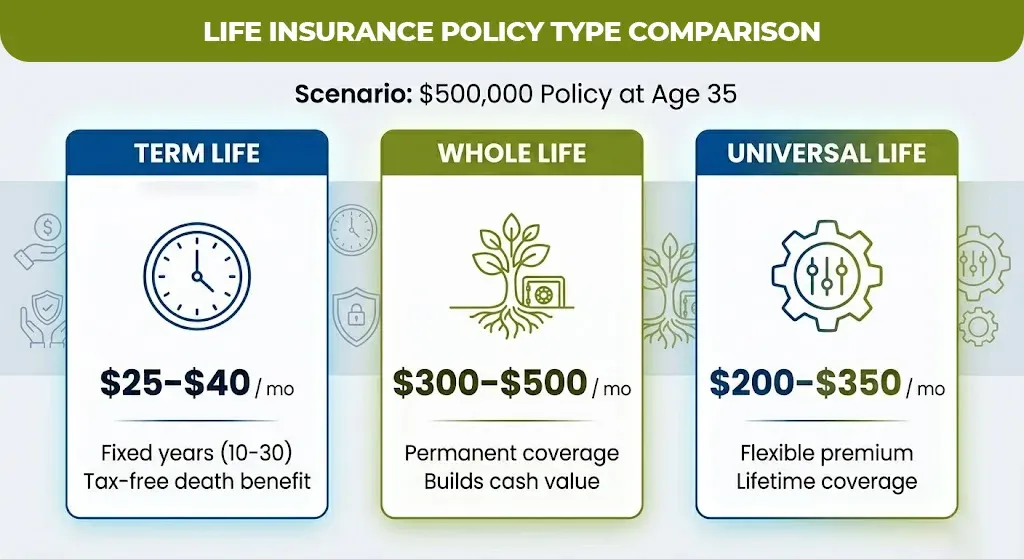

| Policy Type | Coverage Amount | Age 35 (Monthly) | Age 45 (Monthly) | Age 55 (Monthly) |

| 20-Year Term Life | $500,000 | $25–$40 | $69–$110 | $150–$250 |

| Whole Life | $500,000 | $300–$500 | $500–$800 | $900–$1,300 |

| Universal Life | $500,000 | $200–$350 | $400–$650 | $765–$930 |

Term insurance is considered as the more state forward option. You have to pay the fixed monthly premiums for a certain number of years that are 10, 20 or even 30 and when you die within that time, your beneficiaries will receive the full death benefit tax free.

Whole life insurance is the permanent coverage that can also builds cash value over time. It costs you more, MoneyGeek’s 2026 analysis shows that the whole life running roughly 10 times more than a comparable term policy at age 20, narrowing to about 4 times more by age 60.

For most people shopping for financial protection for their family or mortgage, term life is the right starting point. Whole life makes sense when you have already maximized other tax-advantaged savings vehicles and want a forced savings component in your coverage.

What Factors Change Your Term Life Insurance Quotation the Most?

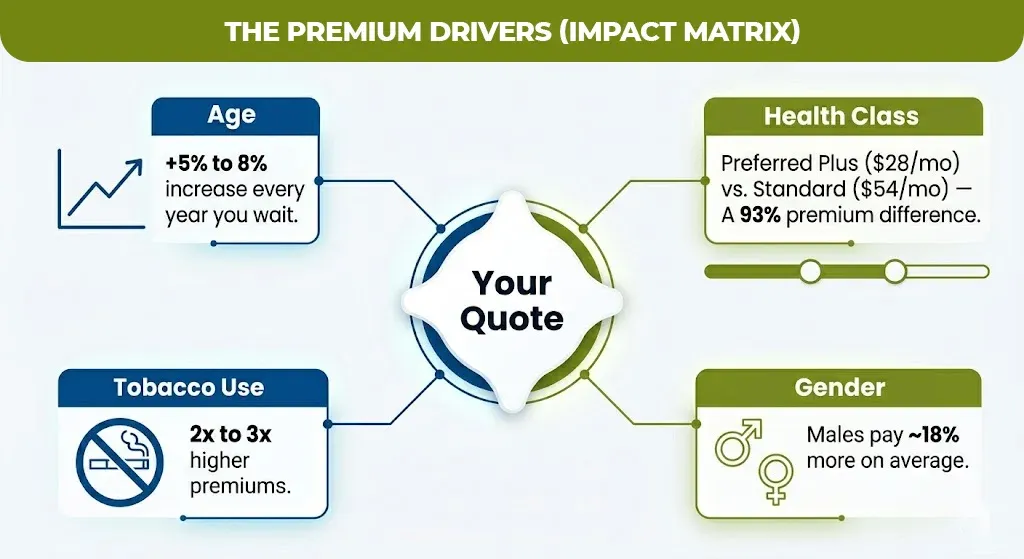

Your quote is not random. Every number has a driver. Knowing these in advance means no surprises when your actual application comes back.

Age is the single most powerful variable. The same $500,000, 20-year term policy that costs around $30 per month at age 35 can exceed $150 per month at age 50. InsuranceGeek’s 2026 data shows premiums increase roughly 5 to 8 percent for every year you wait.

Health classification creates the widest spread in quotes. A 40-year-old male at Preferred Plus best health tier that pays $28.03 per month for a $500,000, 20-year term policy. The same man at Standard (average health tier) pays $54.08 per month. That is a 93% premium difference for identical coverage.

Tobacco use typically doubles or triples your premium compared to a non-smoker rate. Even if you quit recently, most insurers require 12 months of verified non-use before reclassifying your risk tier.

Gender plays a smaller but real role. Males pay approximately 18% more than females at the same age and health tier because of actuarial differences in life expectancy.

Coverage amount increases your premium proportionally, but not always dramatically. Moving from $500,000 to $1,000,000 in coverage rarely doubles the cost, the per-dollar rate often improves slightly at higher face amounts.

How to Get an Online Life Insurance Quotation Without Giving Everything Away

Many people avoid getting a quote because they expect to be asked for everything upfront. That is no longer how most online life insurance quotation tools work.

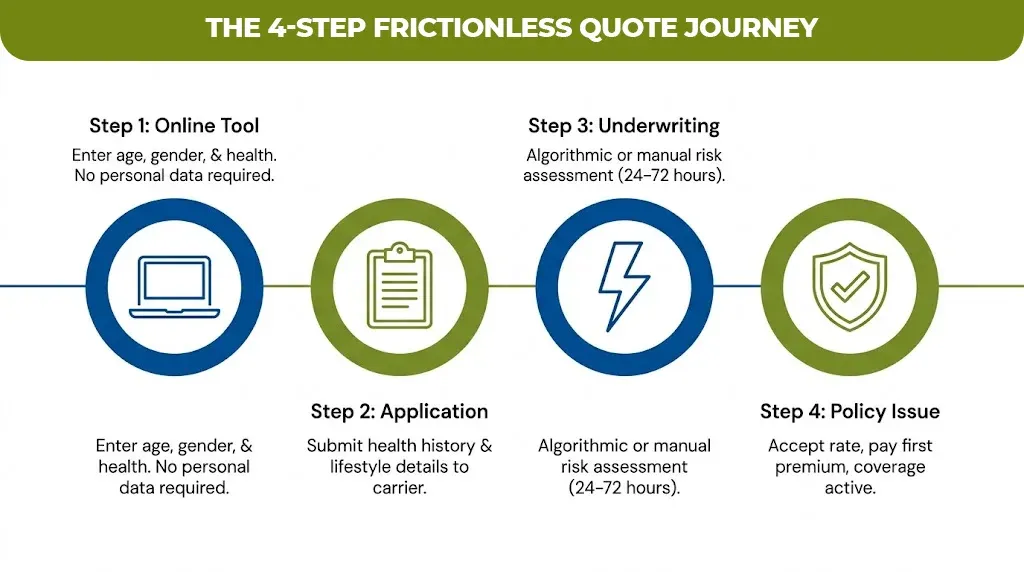

You can get a term life insurance quotation without personal information in the early stages of comparison. Preliminary quote engines typically ask only for age, gender, health category (excellent, good, average), and desired coverage amount. No Social Security number. No medical records. No agent call required.

That quote is accurate enough to compare the providers meaningfully. When you move to the formal application the underwriting process will be depends, medical history questions and sometimes a detailed paramedical exam and this will all depend on the provider and the coverage amount.

Here is the realistic quote journey:

- Online comparison tool: Enter basic details, get 5 to 10 carrier quotes in seconds. No commitment, no personal data.

- Carrier application: Submit health history, lifestyle questions, beneficiary details. This triggers formal underwriting.

- Underwriting decision: The carrier assigns your rate class and confirms or adjusts the quote. Most decisions return within 24 to 72 hours for accelerated underwriting programs.

- Policy issue: You accept the offer, pay your first premium, and coverage begins.

For no-medical exam life insurance, the process is even faster. Most carriers cap these policies at $1 to $2 million and use algorithmic underwriting based on your application data and third-party records rather than a physical exam.

Mortgage Life Insurance Quotation: What It Is and When You Need It

A mortgage life insurance quotation is a specialized quote for a policy tied to your outstanding home loan balance. Unlike standard term life, where the death benefit stays level, mortgage life insurance typically has a decreasing benefit that mirrors your remaining loan balance.

The purpose is narrow so that it pays off the mortgage so your family keeps the home if you die during the repayment period.

| Feature | Mortgage Life Insurance | Standard Term Life |

| Death benefit | Decreasing (mirrors loan balance) | Fixed (set at policy issue) |

| Beneficiary | Lender (pays off loan directly) | Your named beneficiary |

| Flexibility | Low | High (beneficiary uses funds freely) |

| Cost | Generally higher per dollar of coverage | Lower cost per dollar of coverage |

| Portability | Tied to specific mortgage | Independent of any debt |

Most financial advisors recommend a standard term life policy over dedicated mortgage life insurance for one reason: flexibility. If your family receives a $500,000 death benefit rather than a lender receiving a decreasing payoff, they can decide how to use those funds pay off the mortgage, cover living expenses, fund education, or invest. A mortgage life policy removes that choice entirely.

The one scenario where mortgage life insurance makes sense is when someone cannot qualify for standard term coverage due to health conditions, and the lender requires coverage as a condition of the loan.

What Affects Senior Life Insurance Quotes Differently

For buyers over 60, the quotation process, product options, and cost structure all shift meaningfully.

Term life becomes increasingly expensive and shorter in duration. Most carriers cap term life at 10 or 15 years for applicants over 65, which limits the coverage window precisely when many seniors need it most. Whole life and guaranteed universal life become more competitive comparisons at this stage.

Guaranteed issue life insurance is available without any health questions for buyers typically between ages 50 and 85. The tradeoff is a higher cost per dollar of coverage and a graded benefit period, meaning the full death benefit only pays if you survive two to three years after policy issue.

MoneyGeek’s 2026 rate data shows universal life averaging $765 to $930 per month for a 60 year old seeking $500,000 in coverage, significantly less than whole life at $1,308 to $1,443 per month for the same coverage. For cost-sensitive senior buyers who want permanent coverage, universal life is the more practical option.

Ready to See Your Actual Number?

If you have been putting off getting a life insurance quotation because you assumed it would be expensive, complicated, or invasive, the process is significantly simpler than most people expect.

MLife Insurance offers personalized life insurance quotations with no pressure and no junk mail. If you are evaluating coverage for the first time, comparing your current policy against newer rates, or planning coverage around a mortgage or growing family, a real quote takes minutes and gives you a number you can actually build a decision around.

The right time to get a life insurance quotation is always earlier than you think. The cost difference between getting covered at 35 versus 45 is not small and unlike most financial decisions, this one only gets more expensive the longer you wait.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.