Senior Term Life Insurance Rates – Why 60+ Gets Expensive

Once you hit 60, a term life insurance economics. Most of the insurance companies begin more rigorous medical underwriting, molarity is before statistics steeper.

A 65 year old looking at a 20 year term policy $500,000 will pay $165-$210 per month roughly 7 to 8 times a healthy 30 year old. At this age, many people reconsider coverage needs, mortgages are paid off, kids are independent, retirement savings become a focus.

This is where aarp term life insurance rate chart by age marketed policies and issue protection into the picture. These require no medical exam approved by nearly anyone, but they reflect the high risk of $3 to $5 per month for $1000 of coverage. $500,000 AARP policy is equal to $150-$250 per month comparable with standard underwriting but without the underwriting process itself. For seniors, the real decision is not about finding the cheapest rate, it is all about whether you need the coverage at all, given a shortened benefit period.

What Affects Your Rate Beyond Age: How to Beat the Chart

Age sets the baseline, but your actual rate depends on several factors you can control

- Health and medical history, non-smoker pay 30% to 50% less than smokers. Recent surgeries, diabetes or health conditions at high rates.

- Occupation and hobbies, dangerous jobs or extreme hobbies increase the premiums. Desk jobs get preferred rates.

- Prescription medications, being on multiple prescriptions, especially for hypertension or mental health conditions, increase underwriting scrutiny. A clean medication list helps.

- Lifestyle, drinking heavily, poor driving report or criminal history also move into risk brackets.

The practical takeaway is that a 45 year old in excellent health with no smoking history might qualify for dates closer to a healthy 40 years old, sometimes by 10 to 20%. A 40 year old smoker pays like 50 years or worse.

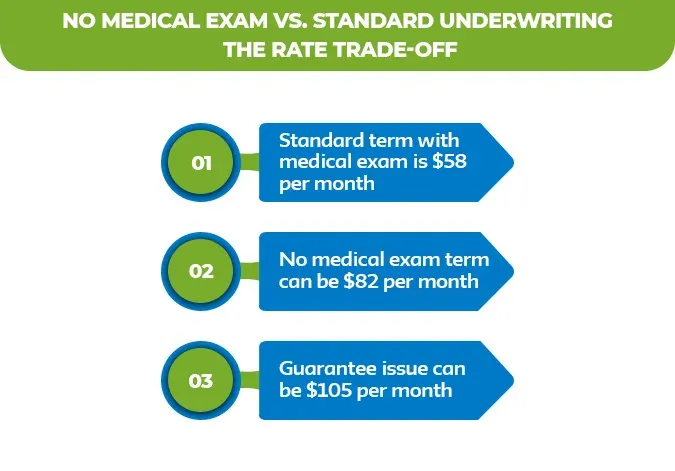

No Medical Exam vs. Standard Underwriting: The Rate Trade-Off

Guaranteed issues or simplified policies kept the medical exam but you will pay for that convenience. Expect to pay 20% to 40% more monthly compared to standard underwriting policy.

For example, a 50-year-old looking $300,000

- Standard term with medical exam is $58 per month

- No medical exam term can be $82 per month

- Guarantee issue can be $105 per month

The trade of his deal, speed uncertainty versus cost. If you are in good health and can’t wait to do three weeks for underwriting, the standard term is almost always a smarter financial choice.

Some employers offer term life insurance through plans with the medical exam required; these are usually the past rates available, regardless of health status. If you employers offer coverage that is often your cheapest option at any age

Take the Next Step: Find Your Actual Rate

He determines your baseline, but only a quote from an actual insurance company reveals what you will pay. Health, job and lifestyle details as much as the birthday on your drivers license.

At M-life Insurance, you can compare your quotes from triple carriers in minutes. There is no commitment, no medical exam required upfront. See what the term life insurance rates by age chart looks like when plugged in with your actual information.

Getting a quote takes 10 minutes. Waiting another year costs thousands. The match is straightforward.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.