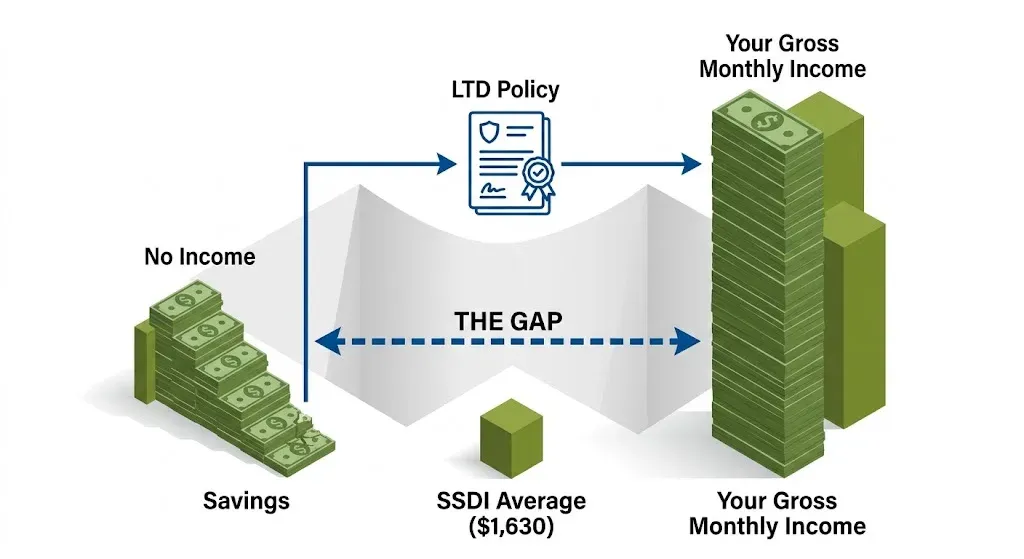

Most people think becoming disabled means two things: a hospital stay and a Workers’ Comp check. What actually happens is a lot quieter. You cannot work for six months. Then twelve. Your savings disappear faster than you planned, and the Social Security disability check, if you even get approved, averages $1,630 a month in 2026.

That is the gap that long term disability insurance is built to fill. And if you do not have it, or are not sure whether yours is enough, this is exactly what you need to read.

What Is Long Term Disability Insurance, and What Does It Actually Pay?

Long-term disability insurance plan that will replace a portion of your income that is 50 to 80% of your gross month salary. If a serious illness or injury keeps you out of work that you are not able to work for the extended period. The plan is not like short-term disability, which only covers you for a few months, long-term disability can cover you and give you benefits for two, five or 10 years or in some cases all the way until retirement age.

The most common causes for the long-term disability claims are not the dramatic accidents. According to the Council for Disability Awareness, diseases like musculoskeletal disorders, any type of cancer, mental health condition and cardiovascular disease reasons that people file for this plan.

Here is the key number to understand the stakes: the average long-term disability claim lasts 34.5 months, nearly three years without income. Even solid savings evaporate over that stretch, especially when medical costs rise at the same time.

Short Term vs Long Term Disability Insurance: Which One Do You Need?

The honest answer is most people need both, and they serve very different purposes.

| Feature | Short Term Disability | Long Term Disability Insurance |

| Benefit period | 3 to 6 months | 2 years to retirement age |

| Income replacement | 60 to 70% of salary | 50 to 80% of salary |

| Waiting period | 0 to 30 days | 90 to 180 days (elimination period) |

| Best for | Surgery recovery, pregnancy, short illness | Serious illness, injury, chronic condition |

| Cost (individual) | Similar to LTD: 1 to 3% of income | 1 to 4% of annual salary |

| Portability | Depends on employer plan | Individual policies travel with you |

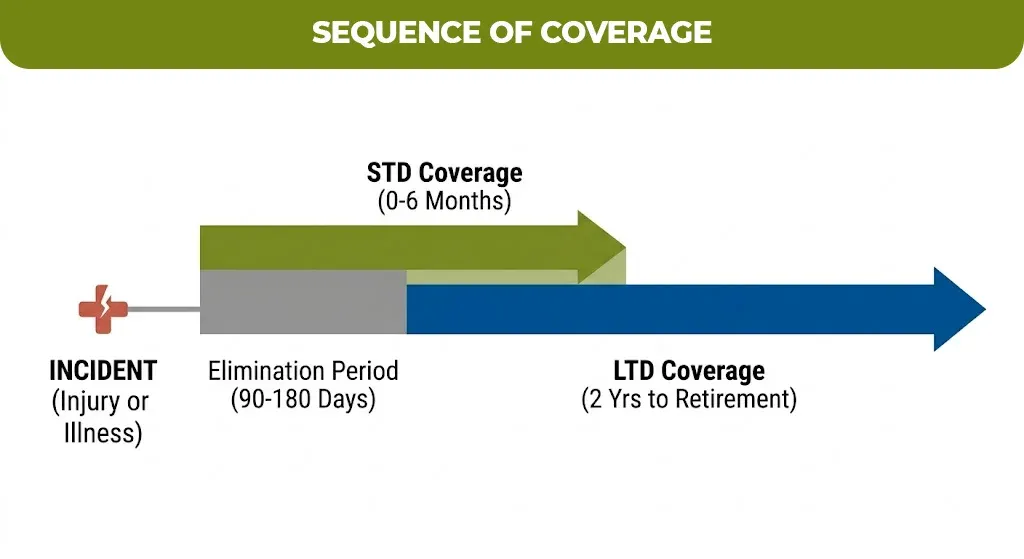

Short term disability insurance covers up to six months and replaces about 60% of your income. Long term disability insurance picks up where that ends. When employers offer both, they are designed to work in sequence, your short term policy bridges the elimination period of your long-term policy.

If your employer only offers one, or you have neither, the gap is entirely yours to fund from savings.

Long Term Disability Insurance Cost: What You Will Actually Pay

Cost is the question almost everyone starts with, and the answer depends on several factors, but there are clear benchmarks that give you a working range.

Long term disability insurance generally costs 1 to 3 percent of your annual salary. For someone earning $80,000 a year, that is roughly $67 to $200 per month. The average individual policy runs about $2,200 per year according to Policygenius, though your actual long term disability insurance quote will shift based on the factors below.

| Factor | How It Affects Your Premium |

| Age | Younger applicants pay significantly less |

| Gender | Women often pay 15% more due to higher claim rates |

| Occupation | Physical or high-risk jobs cost more to insure |

| Health history | Pre-existing conditions raise rates or limit coverage |

| Benefit period | A policy to age 65 costs more than a 5-year benefit |

| Elimination period | Choosing 180 days over 90 days lowers premiums |

| Own-occupation definition | More generous coverage costs more |

Employer-sponsored group disability insurance plans run $30 to $60 per month on average and are typically 15 percent cheaper than individual policies but they are tied to your job. If you leave, coverage ends. Individual long term disability insurance policies go with you regardless of where you work, which is a meaningful difference for anyone in a field with job mobility.

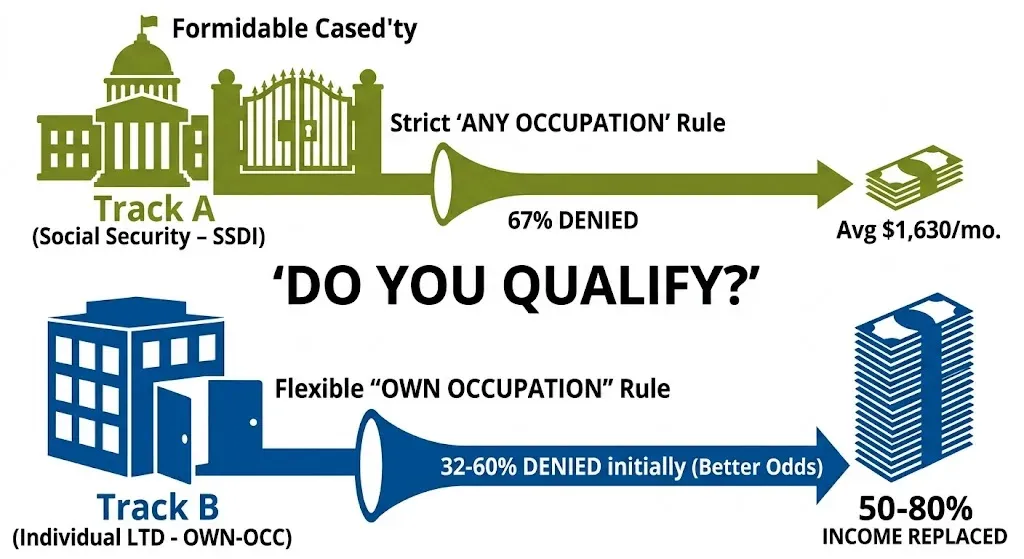

Do I Need Long Term Disability Insurance If I Have SSDI?

This is one of the most common and most costly misconceptions. Social Security Disability Insurance is not a reliable substitute for private long-term disability insurance for two reasons.

First, the average 2026 monthly SSDI benefit is $1,630, with a maximum of $4,152. For most working adults, that is a severe income cut. At $19,560 annually, it rarely covers mortgage payments, student loans, and basic living expenses at the same time.

Second, qualifying is far harder than most people expect. Social Security disability applications are denied about two-thirds of the time at the initial stage. Even private long-term disability insurance claim denial rates range between 32 and 60 percent initially, which is why having a good policy and understanding its terms matters so much before you ever need to file.

SSDI also requires a five-month waiting period before any benefits begin, and the definition of disability it uses is strict: you must be unable to perform any job at all, not just your own. A surgeon who can no longer operate but could theoretically work in an unrelated field would not qualify for SSDI. A good individual long term disability insurance policy with own-occupation coverage would pay.

Best Long Term Disability Insurance: What to Look for in a Policy

Not all policies are equal. Here is what separates the best long term disability insurance from coverage that sounds good but fails when you need it.

Own-occupation definition

This is the single most important feature. It pays benefits if you cannot do your specific job — not just any job. Without it, a carrier can deny your claim because you could theoretically work elsewhere.

Non-cancelable and guaranteed renewable

These terms mean your insurer cannot raise your premiums or cancel coverage as long as you pay. Without them, your rates can change at renewal.

Benefit period

Policies vary from two years to age 65. For anyone under 50, a benefit period to retirement age is worth the additional cost.

Elimination period

This is how long you must be disabled before benefits begin. Ninety days is common; 180 days lowers your premium but requires more savings to bridge the gap.

Residual or partial disability rider

If you return to work part-time or at reduced capacity, this rider pays a partial benefit rather than cutting you off entirely.

Leading long-term disability insurance providers in 2026 are guardian, principal, MassMutual, ameritas, and Northwestern mutual for individual policies. For the employer sponsored group plans the companies include CIGNA, MetLife, Hartford and Unum, and these companies are the most commonly used.

Long Term Disability Insurance in California and Employer Coverage Gaps

California is one of five states with a mandatory state disability program (SDI), which provides short-term income replacement for up to 52 weeks. It does not replace long-term disability insurance in California for extended disabilities. Once your state benefit period ends, you are on your own without private coverage.

This is a point that trips up many California workers who assume state SDI is sufficient. Employer-provided disability insurance ends when your employment ends, while individual plans belong to you regardless of where you work. If your California employer’s group plan is your only coverage, a career change or layoff during a health event could leave you with nothing.

Getting Quotes and Making the Right Decision

The best time to get long term disability insurance quotes is before you need coverage that is ideally in your 30s, when premiums are lowest and health conditions have not yet developed that could limit your options or raise your rates.

Getting a quote does not require any long paperwork, it just requires basic information like your age, your occupation, income, health history and benefit terms you want. Most of the individual long-term disability insurance policies are medically underwritten and it means that your health application determines your eligibility and your monthly premiums rate. Waiting until you have a diagnosis often means that you are being denied coverage or being excluded from your policy.

If your employer offers group disability insurance, enroll. It is subsidized and does not require medical underwriting. Then evaluate whether the coverage amount and benefit period are enough to protect your actual lifestyle if you were out of work for two or three years.

A Note on Finding the Right Coverage for Your Situation

Understanding how long term disability insurance works is one thing. Getting the right policy at the right price with terms that actually hold up when you file a claim , that is where most people need guidance.

The insurance shopping process can feel overwhelming, especially with policy language around “own-occupation” definitions, elimination periods, and riders that are easy to misread. That is where working with someone who knows the product makes a real difference.

If you are evaluating your coverage options or trying to understand what you currently have, Mlife Insurance works with individuals and families to match the right long term disability insurance policy to their income, occupation, and financial goals without the pressure of being sold something that does not fit.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.