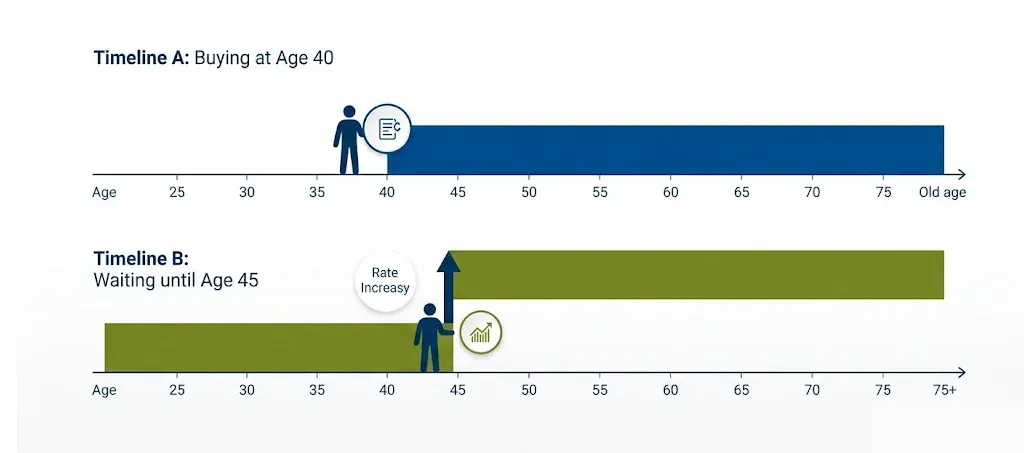

Most people searching for whole life insurance rates by age chart are about to make a decision that will cost them thousands over a lifetime. The mistake is not picking the wrong company. It is waiting too long to buy.

Every year you delay, your premium locks in at a higher age. A 40-year-old who waits five years does not just pay five more years of premiums at 40. They pay a 45-year-old’s rate for the rest of their life. That is a permanent cost increase for a temporary delay.

Here are the real numbers for 2026, laid out clearly so you can make the right call today.

Whole Life Insurance Cost by Age: The 2026 Rate Chart

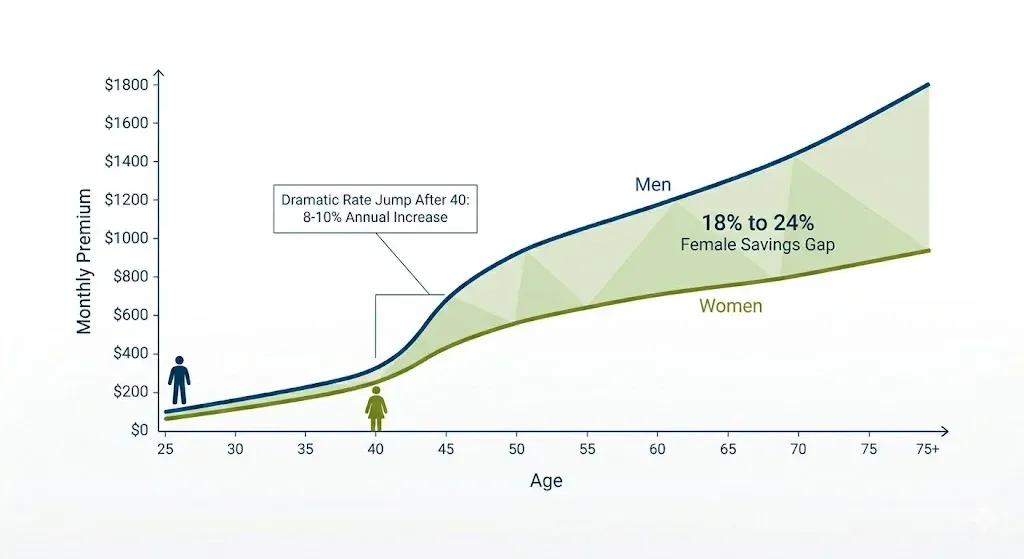

Premiums are fixed the moment your policy is issued. The rate you lock in at 35 years age is the rate you have to pay at 75. According to MoneyGeek’s 2026 analysis, rates range from $238 per month at age 20 to $4,519 per month at age 80 for a woman with the coverage of $500,000.

The table below shows the average monthly whole life insurance premiums for the healthy, non smoking people for the coverage of $250,000:

| Age | Male (Monthly) | Female (Monthly) |

| 25 | $175 | $148 |

| 30 | $210 | $178 |

| 35 | $260 | $218 |

| 40 | $325 | $272 |

| 45 | $415 | $345 |

| 50 | $535 | $445 |

| 55 | $695 | $575 |

| 60 | $910 | $748 |

| 65 | $1,190 | $975 |

| 70 | $1,560 | $1,270 |

Rates are representative market averages for Preferred Non-Smoker applicants, sourced from publicly available 2026 illustrations from top rated carriers. Individual results vary by carrier, health classification, and state.

Two things stand out quickly. Women have to pay roughly 18 to 24 percent less as compared to the men at every age, due to the longer life expectancy. And premiums rise by approximately 8 to 10 percent per year after age 40, according to RetirementLiving.com’s 2026 rate analysis.

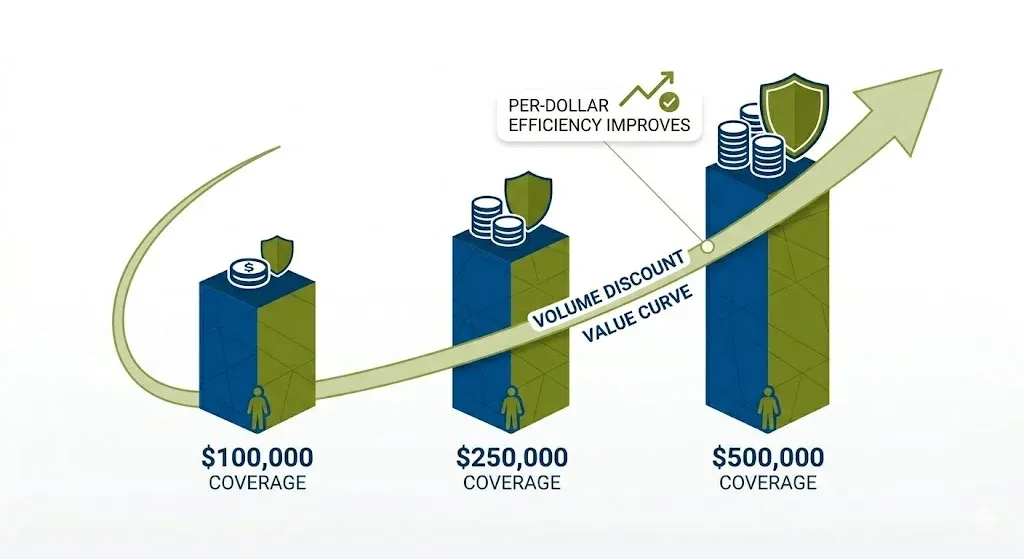

Whole Life Insurance Rates for Different Coverage Amounts

Coverage amount matters, but not in a straight line. Going from $100,000 to $250,000 does not double your premium. Larger policies spread fixed carrier costs across more coverage, so the per-dollar cost often decreases slightly.

Lets have a look at the monthly premiums cost breakdown for a 45 year old man, non smoker in the all three coverage levels

| Coverage Amount | Monthly Premium (Male, Age 45) | Monthly Premium (Female, Age 45) |

| $100,000 | $175 | $145 |

| $250,000 | $415 | $345 |

| $500,000 | $780 | $645 |

| $1,000,000 | $1,490 | $1,220 |

Representative figures based on 2026 carrier illustrations. Health classification and carrier selection will shift these numbers.

Whole Life Insurance Rates for Seniors: What Changes After 60

Whole life insurance for seniors operates differently than it does at younger ages. By the time most people reach 60 or older, the focus shifts from income replacement to final expenses, debt elimination, and leaving something behind for family.

For a 70-year-old woman, a $100,000 whole life policy averages $499 per month, while a man of the same age pays around $533 per month, according to MoneyGeek’s 2026 senior coverage analysis. That is not cheap, but the premium never increases and the death benefit is guaranteed.

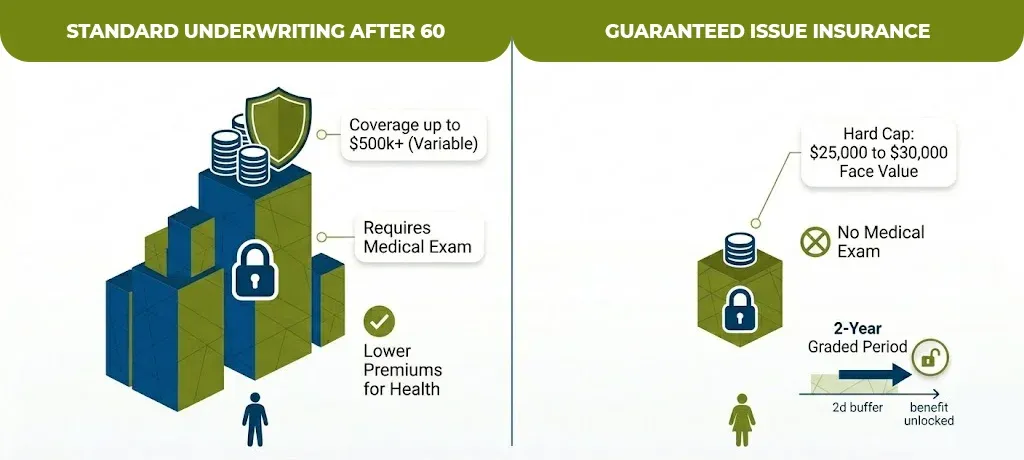

Seniors who face health issues that prevent standard underwriting have another option: guaranteed issue whole life insurance.

What Is Guaranteed Issue Whole Life Insurance and Who Needs It?

Guaranteed issue whole life insurance requires no medical exam and asks no health questions. Approval is guaranteed for applicants typically between ages 50 and 85, depending on the carrier.

The trade offs are real because the coverage is capped at $25,000 to $30,000 in most cases, and the premiums are the highest per dollar of any whole life plan. There are so many policies that also carry a graded death benefit, it means that if the insured passes away from natural causes within the first two years, the beneficiary receives a return of premiums paid plus interest rather than the full death benefit.

This product is designed for one purpose: final expense coverage. Funeral costs average $8,000 to $12,000. Medical bills and outstanding debts add more. A $15,000 to $25,000 policy covers that gap without leaving family members scrambling.

Female vs. Male Whole Life Insurance Rates – The Real Difference

Women consistently pay less for whole life insurance at every age. The reason is actuarial: women live an average of five to six years longer than men, according to CDC data on life expectancy. Longer life expectancy means the insurer has more time to collect premiums before paying a claim.

The average saving for women is roughly 18 to 24 percent at most ages. Over a 30-year policy, that difference compounds significantly. A woman who locks in at 40 and pays $272 per month (versus a man’s $325) saves over $19,000 in total premiums by age 70, assuming no rate changes.

What Factors Affect Your Whole Life Insurance Premium?

The chart gives you a baseline. But your actual rate depends on several factors the chart cannot show.

- Age at application

- Gender

- Health classification

- Smoking status

- Policy structure

- Coverage amount

How to Get the Best Whole Life Insurance Rates by Age Chart

The best rate at any age is not found by picking the most familiar name. It is found by comparing multiple carriers at the same coverage level and health classification, then applying as early as health allows.

Three things consistently lower your lifetime cost:

- Apply early

- Improve your health classification before applying

- Match coverage to actual need

Ready to See Your Actual Rate?

The chart above shows you where the market sits. Your actual rate depends on your specific age, health, and coverage goals.

At Mlife Insurance, we help people find the right whole life policy without the pressure of being pushed toward the most expensive option. If you want a clear picture of what you would actually pay today, explore your options with Mlife Insurance and get a quote that reflects your real situation, no guesswork, no hard sell.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.