Most seniors shopping for life insurance make one of two mistakes like they assume they can not qualify, so they don’t bother. Or they buy whatever comes up first, and overpay by hundreds of dollars a year.

The truth sits right in the middle. Term life insurance for seniors is available, it is also affordable, and sometimes the smartest financial move you will make in your 60s. But the window closes faster than most people realize, and the wrong policy at the wrong age can be a very expensive lesson.

Here’s what you actually need to know before you sign anything.

Can Seniors Actually Get Term Life Insurance?

Yes, but the rules change significantly after 60, 70, and 80.

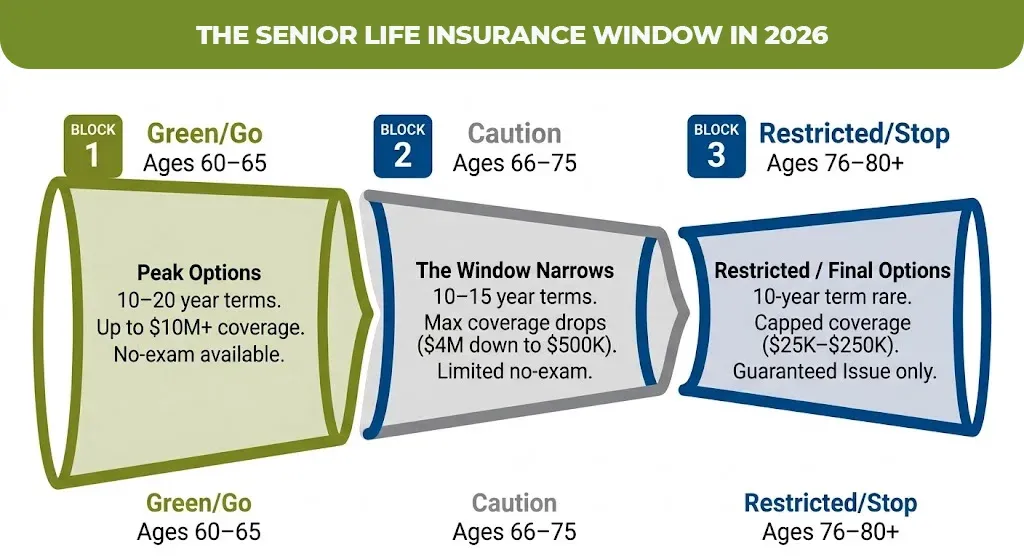

Most of the insurance companies offer term life insurance to seniors through age 70 to 75. A smaller number accepts the applicants up to age 80, but the available term lengths shrink and premiums rise sharply. A 60 year old still gets the good options like term life insurance for seniors over 60 for 10, 15, and even 20 year terms are accessible as . By 75, you are typically looking at 10-year terms only if you qualify at all.

One insurance broker explained it simply like the best time to lock in life insurance is usually between ages 60 and 70. If people wait too long, like until 68 or older, the prices can go up a lot and fewer long term policy options will be available.

If you are in your early 60s and putting this off, that delay has a real dollar cost. Here’s the short version of what age does to your options:

| Age | Available Terms | No-Exam Options | Max Coverage (Typical) |

| 60–65 | 10, 15, 20 years | Yes | Up to $10M+ |

| 66–70 | 10, 15 years | Yes (lower caps) | Up to $4M |

| 71–75 | 10 years | Limited | Up to $500K |

| 76–80 | 10 years (rare) | Rare | Up to $250K |

| 80+ | Term rarely available | Guaranteed issue only | $25K–$50K |

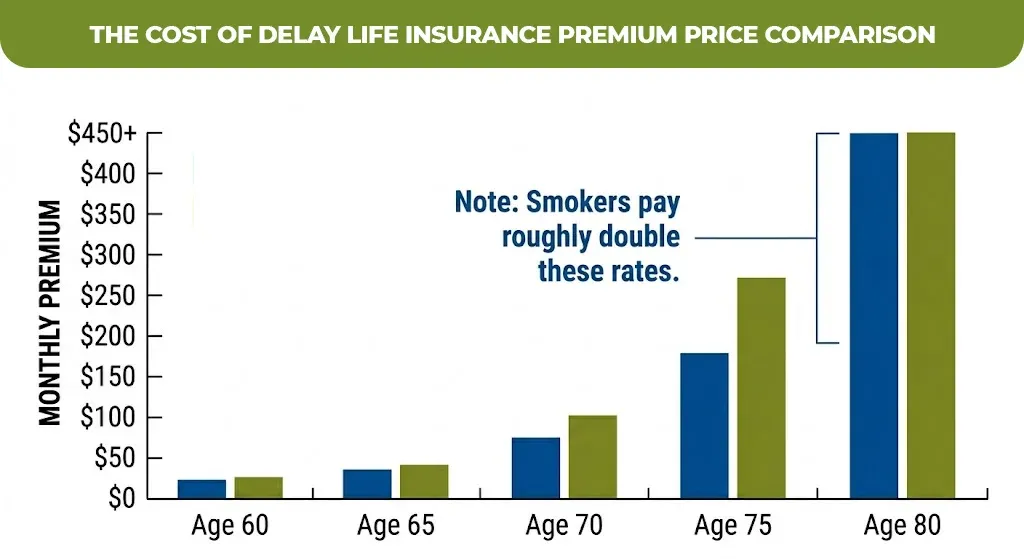

Term Life Insurance Rates for Seniors in 2026 – Actual Numbers

Rates can be different and it will be depending on age, gender, health class, and coverage amount. Below is a realistic look at what a $250,000, 10-year term policy costs for nonsmoking seniors in average health.

Monthly Premium — $250,000 For 10-Year Term For Nonsmoker – Average Health

| Age | Women (est.) | Men (est.) | Cheapest Provider |

| 60 | $42–$50/mo | $60–$75/mo | Penn Mutual |

| 65 | $72–$84/mo | $110–$119/mo | Penn Mutual / Pacific Life |

| 70 | $97–$130/m | $132–$165/mo | John Hancock |

| 75 | $200–$272/mo | $300–$412/mo | John Hancock / Protective |

| 80 | $272+/mo | $412+/mo | Protective / Mutual of Omaha |

A few things this table doesn’t show: smokers pay roughly double these rates. Seniors with health conditions like diabetes, hypertension, prior cancer in remission can still qualify for standard rates through the right carrier, but that depends heavily on how you shop.

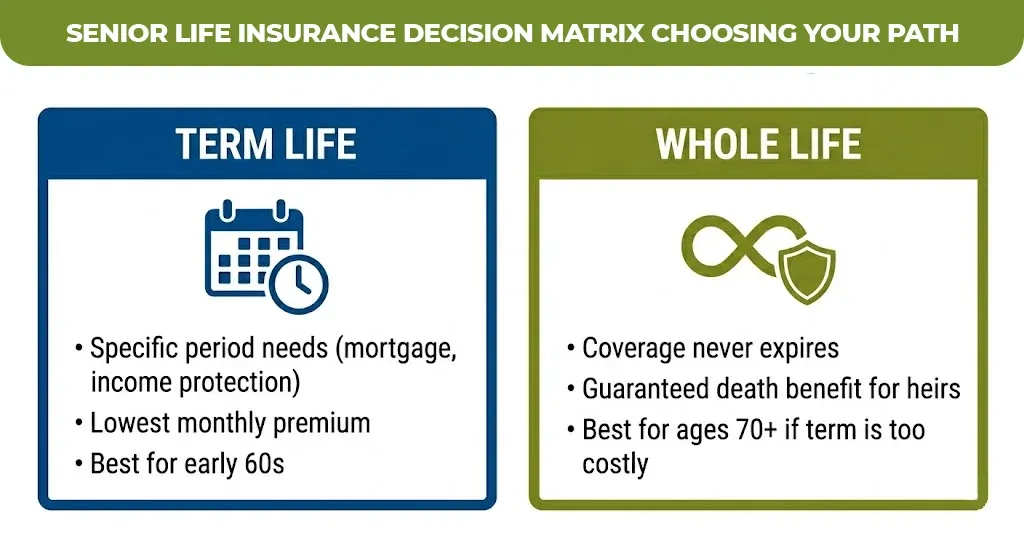

Term or Whole Life Insurance for Seniors – Which One Makes Sense?

This is the question most articles dodge. Here’s the honest answer: it depends on why you are buying coverage.

Choose Term Life If

- You need coverage for a specific period like paying off a mortgage, protecting a spouse’s income through retirement, or covering a business obligation

- You want the lowest possible monthly premium

- You’re in your early 60s and in reasonable health

Choose Whole Life (Or Guaranteed Universal Life) If:

- You want coverage that never expires, regardless of age.

- You are focused on leaving a guaranteed death benefit to heirs.

- You’re 70+ and term options are either unavailable or unaffordable for your need.

Best Term Life Insurance Companies for Seniors in 2026

Not all carriers serve seniors equally. Here’s how the top options compare for the things that actually matter:

| Company | Max Issue Age | No-Exam Option | Best For | AM Best Rating |

| Penn Mutual | 75 | Yes (up to $10M) | Lowest rates at 60–70 | A+ |

| Banner Life | 70 | Yes (up to $4M) | Conversion to permanent | A+ |

| Pacific Life | 80 | Yes | Older seniors, high coverage | A+ |

| John Hancock | 75 | Yes | Best rates for men over 70 | A+ |

| Protective | 80 (whole) | No for term | Highest death benefit option | A+ |

| Mutual of Omaha | 80 | Yes (guaranteed issue) | Yes (guaranteed issue)No-exam guaranteed coverage | A+ |

A note on Mutual of Omaha term life insurance for seniors like its is one of the most recognized names in senior coverage and holds an A+ BBB rating. It’s particularly strong for guaranteed issue policies like no medical exam required) and for seniors who need coverage but have health conditions that make traditional underwriting difficult.

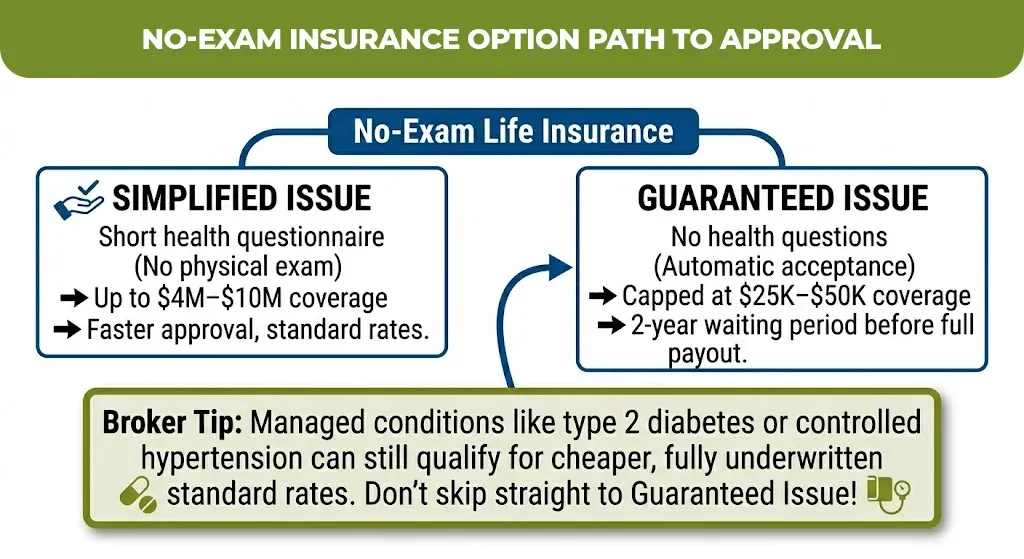

Term Life Insurance for Seniors Without a Medical Exam: What’s Available

Many seniors assume health issues disqualify them entirely. They don’t, but the path is different.

Best term life insurance for seniors without medical exam typically falls into two categories:

Simplified Issue

A short health questionnaire, no physical exam. Approval is faster, premiums are slightly higher than fully underwritten policies. Coverage caps are usually $500,000 to $4 million depending on the carrier. Penn Mutual and Banner Life offer no-exam options up to $4M–$10M.

Guaranteed Issue

No health questions, no exam, automatic acceptance. Premiums are higher per dollar of the coverage, and there is typically a 2 year waiting period before full death benefits are paid. Coverage is capped, usually $25,000 to $50,000. Mutual of Omaha and Physicians Mutual are the strong options here.

Guaranteed Term Life Insurance

Guaranteed term life insurance of the no-exam variety is particularly useful for seniors over 75 or those with conditions like COPD, recent cardiac events, or uncontrolled diabetes who can’t pass standard underwriting.

Important Caution

Don’t assume that guaranteed issue is your only option before getting the fully underwritten quote. There are so many seniors with managed conditions like controlled hypertension or type 2 diabetes still qualify for the standard or preferred rates through the right carrier. According to Ethos, even seniors with diabetes, hypertension, or prior cancer in remission can qualify for the competitive rates when working with a broker who shops multiple carriers.

How to Get the Cheapest Term Life Insurance for Seniors

Getting cheap term life insurance for seniors comes down to five decisions more than anything else.

- Apply before your next birthday.

- Buy more than you think you need, now.

- Choose the shortest term that covers your actual need.

- Shop multiple carriers, don’t quote just one.

- Consider a conversion rider if you’re unsure about future needs.

What Seniors Over 70 and 80 Should Actually Consider

Term life insurance for seniors over 70 is still possible, but the cost math shifts. At 70, a 10-year term covering $100,000 for a male nonsmoker runs roughly $130–$165/month. That’s $15,600–$19,800 over the full term, for a $100,000 benefit.

Whether that’s worth it depends on why you’re buying: income replacement, debt coverage, or final expenses. For pure final expense needs (funeral costs average $8,000–$12,000 in 2026, per Wealthvieu), a smaller whole life or guaranteed issue policy often delivers better value at this age.

Term life insurance for seniors over 80 is largely unavailable through traditional carriers. Pacific Life and Protective are among the few that accept applicants up to 80, but coverage is restricted and premiums are significant. At this stage, guaranteed universal life or final expense whole life policies are usually the more practical path.

Thinking Through Your Options? Here’s a Sensible Next Step

If you’re in your 60s and haven’t locked in coverage yet, this is the moment that actually matters, not some future date when it “feels right.”

The team at Mlife Insurance works with seniors across all health profiles to compare term life quotes from multiple carriers. No pressure, no single-carrier pitch, just a clear look at what you qualify for and what it costs.

If you want to see what your numbers look like, start with a quote at Mlife Insurance. It takes a few minutes and costs nothing. The information you walk away with is worth having regardless of what you decide.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.