Here’s the mistake people make: they assume the disability coverage their employer provides is enough, until they file a claim, get denied, and realize they signed up for an ERISA-governed group plan with almost no legal recourse.

Or the opposite, they overpay for a private individual policy without understanding what it actually protects against, what’s excluded, and whether their pre-existing condition quietly voids their coverage.

Individual disability insurance is one of the most misunderstood financial products available. This guide cuts through the confusion.

What Is Individual Disability Insurance Policy — and Who Actually Needs It?

Individual disability insurance is a private plan and you can purchase this plan directly from an insurance company. This plan is specially made to replace the portion of your income if you cannot work because of any illness or injury, you own this policy and it will follow you regardless of where you work.

According to the Council for Disability Awareness, over 26% of working Americans will face a disability lasting longer than 90 days during their career. Yet only 40% of working-age individuals currently carry any disability coverage, according to industry data.

The income protection gap is real. And it hits hardest for self-employed professionals, high earners, business owners, and anyone whose employer-sponsored plan caps benefits at a number that wouldn’t cover their actual expenses.

Who needs to prioritize this

- Self-employed professionals with no employer plan

- High-income earners whose group plan caps fall well short of their salary

- Anyone in a specialized occupation like physicians, attorneys, engineers who needs “own occupation” protection

- Employees who want coverage that won’t disappear when they change jobs

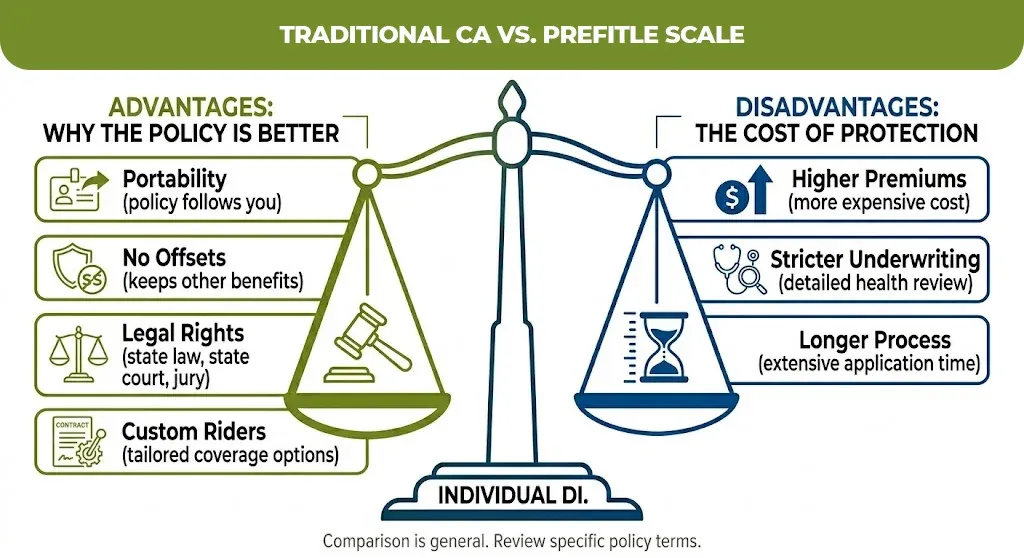

The Honest Pros and Cons of Individual Disability Insurance

Most articles present this as a clear win. The reality is more nuanced.

Advantages

- Portability

- Better definitions of disability

- Tax-free benefits

- Legal protections

- Customizable riders

Disadvantages

- Higher premiums

- Stricter underwriting

- Longer application process.

Group vs. Individual Disability Insurance: The Comparison That Actually Matters

Don’t just look at cost. Look at what happens when you need to use it.

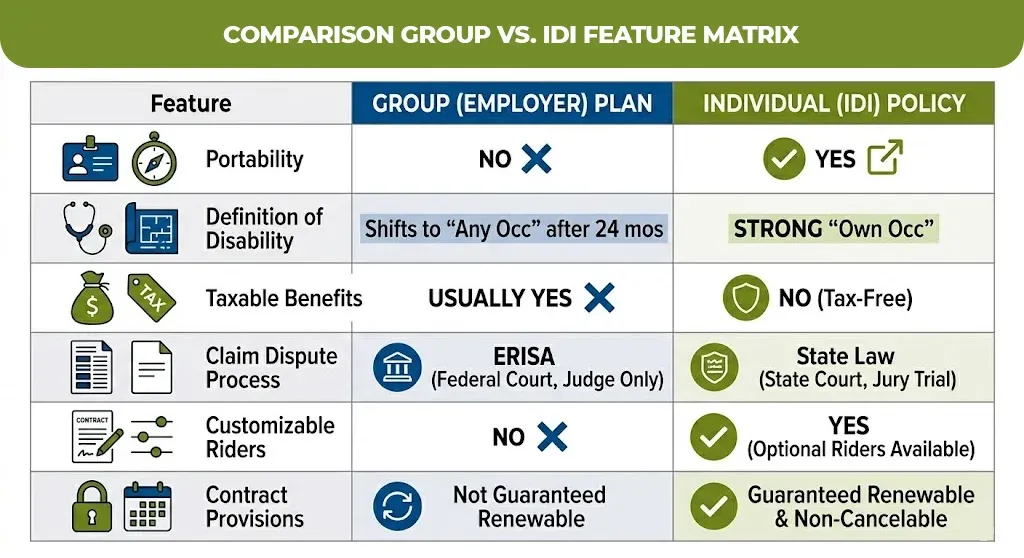

| Factor | Individual Disability Insurance | Group (Employer) Disability Insurance |

| Portability | Yes — you own it | No — tied to employment |

| Governed by | State insurance law | ERISA (federal) |

| Disability definition | “Own occupation” available | Shifts to “any occupation” after 24 months |

| Benefits offset by SSDI? | No | Yes — dollar-for-dollar reduction |

| Benefits taxable? | No (if you pay premiums) | Usually yes (if employer pays premiums) |

| Customizable riders | Yes | No |

| Claim dispute process | State court, jury trial available | Federal court, judge only, no punitive damages |

| Pre-existing condition handling | Permanent exclusions possible | Exclusion typically expires after 12 months |

| Premium cost | Higher | Lower (employer often subsidizes) |

| Benefit amount cap | Based on income | Often capped at 60% of salary |

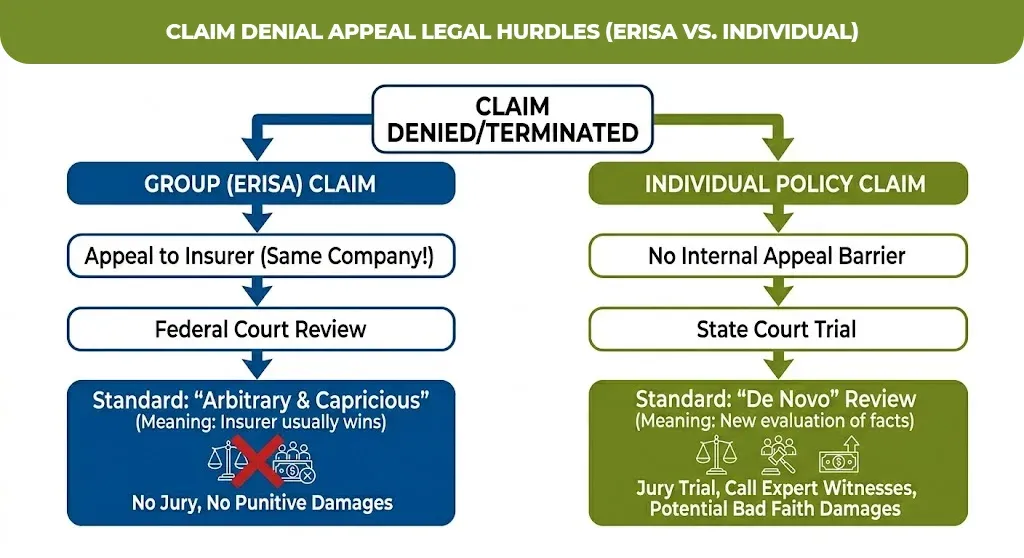

The ERISA issue is one most employees never think about until it’s too late. If your coverage is provided through a group employer plan, that policy is likely governed by ERISA. This means that if your claim is denied and you want to appeal, you’re essentially appealing to the same insurance company that denied the claim, in federal court, with no right to a jury trial and no risk of bad faith damages against the insurer.

With an individual policy, the playing field is different. Your case is heard by a judge and jury in state court. You can introduce new supporting evidence during the trial process and call expert witnesses, options that simply don’t exist in ERISA claims.

The practical takeaway is if your employer offers group coverage, don’t cancel it, it’s often free or low cost. But layering an individual policy on top provides the protections that matter when a real claim arises.

ERISA vs. Individual Disability Insurance: Why This Distinction Could Cost You Thousands

ERISA is the employee retirement income security act of 1974. This is the federal law that will require most of the employers sponsored benefit plans. It especially designed to protect the employees, but it heavily favor the insurance companies in dispute situations.

Here’s what ERISA means for your disability claim

One of the biggest drawbacks of group disability plans is that they fall under ERISA. Insurance companies know this, so they will deny benefits and terminate claims in a high percentage of ERISA cases, knowing that the bar to appeal an adverse decision is very high.

Under ERISA, courts typically review claim denials using an “arbitrary and capricious” standard, it means that the insurance company wins unless their decision was completely unreasonable. Under state law governing individual policies, courts often apply “de novo” review, where a judge independently evaluates the claim from scratch.

The benefit offset trap

Group plan benefits are offset against Social Security, potential retirement benefits, and workers’ compensation, dollar for dollar. Group insurers therefore have a strong incentive to push claimants to apply for SSDI, since any SSDI approval directly reduces what the insurer pays. Individual policy benefits are not offset against other income sources, if you qualify, you collect the full benefit regardless of what SSDI pays.

The Best Individual Disability Insurance Companies in 2026

Not every carrier is equal in underwriting flexibility, payout reliability, or policy features. These are the most established names in the individual disability market:

| Carrier | Standout Feature | Best For |

| Guardian Life | Strong own-occupation definitions; accepts many managed conditions | Professionals, physicians |

| MassMutual | Noncancelable, guaranteed renewable policies | Long-term income protection |

| Principal Financial | Flexible benefit periods; good for business owners | Self-employed, executives |

| The Standard | Strong residual/partial disability riders | Those in specialized occupations |

| Mutual of Omaha | One of few carriers offering short term disability insurance for individuals | Broader health profiles |

| Ameritas | Competitive pricing; strong future increase options | Younger professionals building coverage |

According to Milliman’s 2025 annual survey of the U.S. individual disability income insurance market, new annualized premium across 12 major contributing companies reached $423 million in 2024. This reflects a mature market with established players shop across multiple carriers before committing.

Supplemental Individual Disability Insurance Income: When to Add It

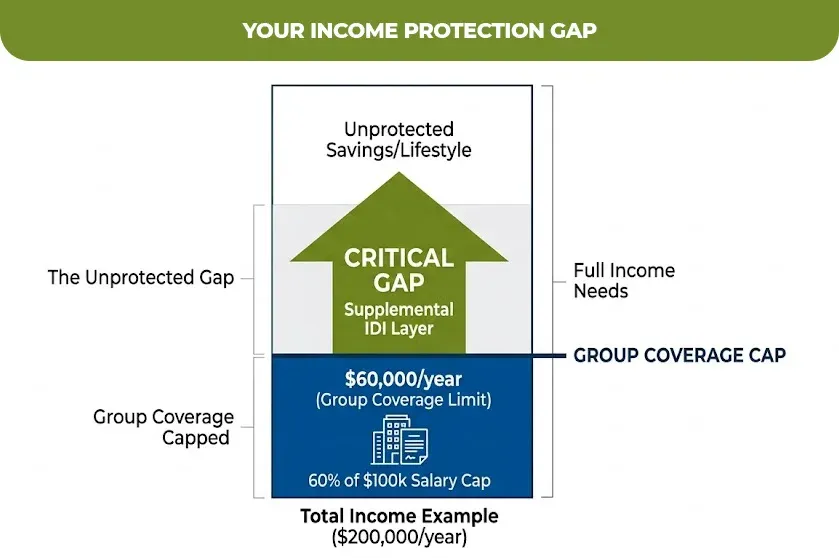

Supplemental individual disability income insurance fills the gap between what your group plan pays and what you actually need to live on.

Most group plans replace 60% of your salary that is capped at a dollar maximum that may be well below what high earners need. If you earn $200,000, a $10,000 per month group cap leaves a large unprotected gap.

Supplemental IDI solves this by layering additional monthly benefits on top of your existing group coverage. It is individually underwritten, privately owned, and stays with you if your employment changes.

The disability market is valued at $4.58 billion in 2025 and it is projected to reach $7.11 billion by the end of 2029 at CAGR of 11.6%. An obvious portion of that growth is trapping by the high income professionals who are purchasing the supplemental coverage and it is evidence that awareness of the coverage gap is growing.

When supplemental coverage makes sense

- Your group plan’s monthly benefit cap is less than 60% of your actual take-home income

- You have significant fixed expenses like mortgage, business overhead, dependents

- You are in a high-demand specialized profession with specific own-occupation needs

Ready to Review Your Disability Coverage?

If you are reading this, you probably have questions a general article can not fully answer about your specific occupation, health history, or the gap between your group coverage and what you actually need.

The next smart step is a side by side comparison of what you currently have versus what individual disability insurance could add. An independent disability insurance specialist can do this without pressure or upselling.

If you’re evaluating your income protection strategy in 2026, start with an honest audit of your existing coverage. The worst time to discover a gap is after a claim.

Protect Your Income Before It’s Too Late

Don’t wait for a claim to find gaps in your coverage. Review your disability protection today with Mlife Insurance and see what you’re really covered for.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.