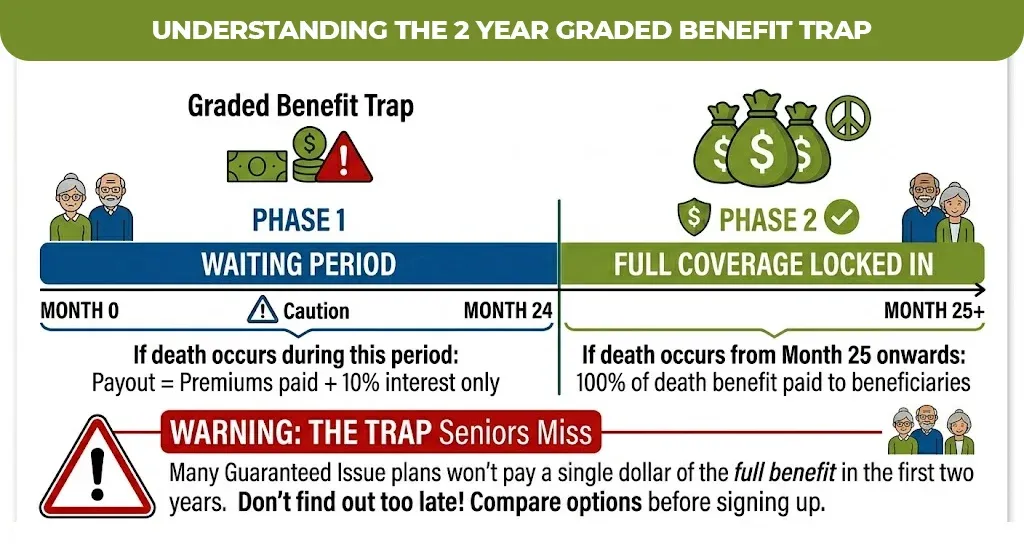

Here’s the mistake thousands of seniors make every year: they search for life insurance for seniors over 60 no medical exam, find the first plan with “guaranteed approval,” sign up, and end up paying $80 a month for a policy that won’t pay a single dollar if they pass away in the first two years.

That’s a real clause. It’s called a graded death benefit. And most people don’t find out until their family tries to file a claim.

You deserve more and even better than that. This article cuts through and tells you exactly what types of no exam life insurance are in 2026, what is the actual cost, who can qualify for these plans, and how to find a policy that genuinely protects the people you love.

Can You Actually Get Life Insurance Over 60 Without a Medical Exam?

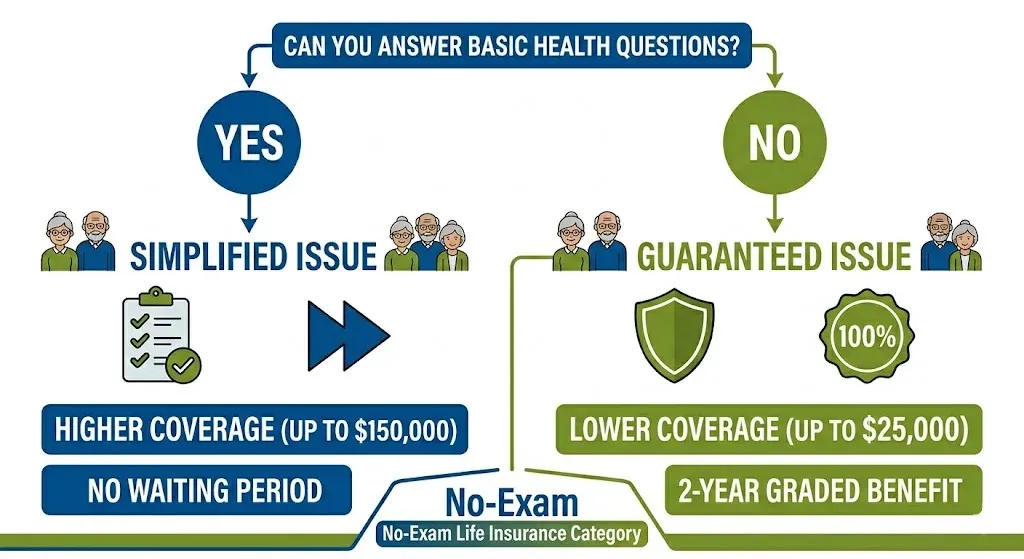

Yes, and it is more accessible than most people realize. The no exam life insurance market for seniors has been widened in the past. In 2026, you have two primary paths like simplified issue and guaranteed issue policies, each designed for different health situations.

The critical distinction most seniors miss is this, no medical exam does not always mean no health questions. Simplified issue policies skip the blood draw and physical but still ask about your health history. Guaranteed issue policies ask nothing at all, but they come with trade offs.

Understanding this difference before you apply is very important and this separates a smart decision from an expensive one.

Simplified Issue vs. Guaranteed Issue: Which One Is Right for You?

| Feature | Simplified Issue | Guaranteed Issue |

| Medical exam required | No | No |

| Health questions | Yes (10–15 questions) | None |

| Who qualifies | Seniors in moderate health | Anyone ages 50–85 |

| Coverage amount | $10,000–$150,000 | $2,000–$25,000 |

| Monthly premium (no exam life insurance for seniors age 60, $15K policy) | $48–$63 (women/men) | Higher per dollar of coverage |

| Graded death benefit | Rarely | Almost always (2-year wait) |

| Best for | Final expenses + some legacy | Serious health conditions only |

The graded benefit trap

Most guaranteed issue policies have a 2-year waiting period. If death occurs within 24 months of the policy issue for reasons other than accident, most guaranteed issue policies pay only the premiums paid plus 10% interest, not the full death benefit. This matters enormously if your health is already compromised.

If you can answer health questions and qualify, even with these conditions like hypertension or type 2 diabetes, the simplified issues are almost always the better value.

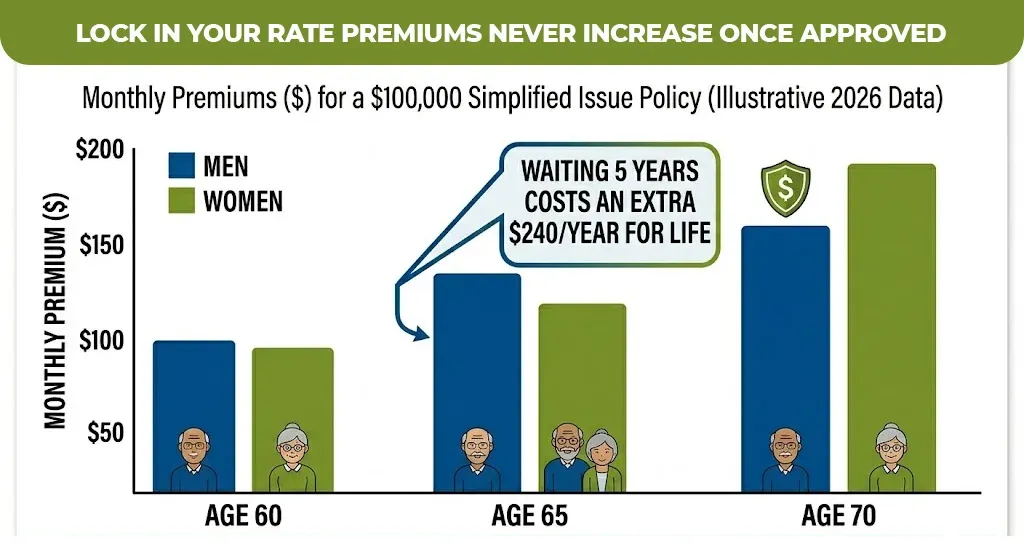

What Does No-Exam Life Insurance for Seniors Over 60 Actually Cost in 2026?

Rates vary by age, gender, health, and coverage amount. Here’s a realistic picture based on current market data:

Simplified Issue Whole Life Insurance For Seniors Over 60 No Medical Exam (Non-Smoker)

| Age | Gender | $10,000 Coverage | $25,000 Coverage | Coverage |

| 60 | Female | $28–$35 | $58–$72 | $105–$130 |

| 60 | Male | $36–$46 | $76–$92 | $135–$165 |

| 65 | Female | $38–$48 | $78–$96 | $145–$175 |

| 65 | Male | $50–$62 | $105–$128 | $190–$225 |

| 70 | Female | $55–$68 | $112–$138 | $210–$255 |

| 70 | Male | $72–$90 | $148–$182 | $275–$340 |

Estimates based on 2026 simplified issue market averages. Your rate depends on carrier, state, and health profile.

One thing to understand about timing is every year you wait adds to your premium. Senior men who wait from age 60 to 65 pay an average of $20 more per month, that’s $240 more per year, on a 10-year, $100,000 plan.

The rate you lock in today is the rate you keep. Once your policy is approved, your premium is fixed and guaranteed never to increase for the life of the policy. That predictability matters on a fixed income.

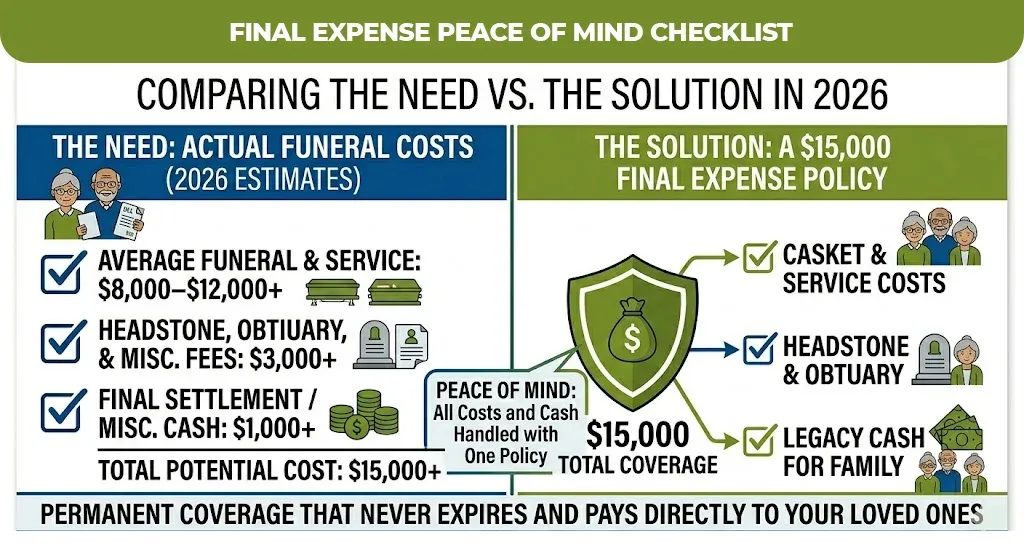

What Is Final Expense Insurance — and Is It the Same Thing?

Final expense insurance for seniors over 60 is not a separate product category. It’s a marketing name for small whole life policies, that is $5,000 to $25,000, and it is designed to cover funeral and burial costs.

The average US funeral cost runs $8,000–$12,000 in 2026. That figure doesn’t include headstone, obituary, or post-service expenses, which can push the total toward $15,000 in many regions.

Final expense policies are almost always simplified or guaranteed issues, like no medical exams required. They are permanent, it means it will not expire, premiums don’t increase, and they pay directly to your beneficiary, who can use the funds for any purpose.

If your primary goal is making sure your family isn’t handed a funeral bill at the worst possible moment, a final expense policy is one of the most straightforward financial decisions you can make after 60.

Is No-Exam Life Insurance Worth It for Seniors in Good Health?

The honest answer is, not always. Fully underwritten policies cost less than no-exam options for most seniors in decent health. The exam is worth it if your health profile is solid. If you’re a healthy 60-year-old with no significant conditions, going through standard underwriting can get you significantly higher coverage at a lower monthly premium.

No-exam policies are most worth it when:

- You have health conditions that complicate traditional underwriting

- You need coverage fast (approval can come in days, not weeks)

- You want simplicity and certainty without the anxiety of a full exam

- Your coverage need is modest ($10,000–$50,000 for final expenses)

No-exam policies are less optimal when:

- You’re in good health and want $100,000+ in coverage

- Cost per dollar of coverage is your primary concern

- You are in your early 60s and have time to go through standard underwriting

How to Find the Best Rate Without Getting Burned

Three rules that apply regardless of which policy type you’re considering:

- Never buy from a single quote.

- Work with an independent broker, not a captive agent

- Lock in now, not later.

Top Life Insurance Providers for Seniors Over 60 — No-Exam Options at a Glance

| Provider | Policy Type | No-Exam Option | Max Coverage | Best For |

| AARP / New York Life | Term + Whole Life | Yes — all plans | $150,000 | Members wanting flexible options |

| Mutual of Omaha | Whole Life | Yes — guaranteed issue | $25,000 | Seniors with health concerns |

| Fidelity Life | Term + Whole Life | Yes — simplified issue | $150,000 | Seniors in their early 60s |

| Colonial Penn | Whole Life | Yes — guaranteed issue | Unit-based | Entry-level final expense |

| Physicians Mutual | Final Expense | Yes — simplified issue | $50,000 | affordable life insurance for seniors over 60 no medical exam |

One Last Thing Before You Decide

The best policy is not the one with the lowest sticker price. It’s the one that will actually pay out when your family needs it, at a premium you can maintain on a fixed income, without a waiting period that leaves your loved ones and family unprotected.

If you’re still comparing options or not sure which policy type fits your health situation, the team at Mlife Insurance helps seniors do exactly this, compare multiple carriers, understand the fine print, and find coverage that makes financial sense.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.