A lot of the people nowadays choose a health insurance plan the same way they pick a Netflix show like they scroll very fast, pick something that they think is good, and hope it will work out. The problem here is? A wrong plan choice can leave you with a $4,000 surprise bill at a specialist visit, or locked out of your preferred doctor entirely.

There are 7 types of health insurance plans and each plan works very differently, also they cost you the different prices and suit your different situations. Knowing each plan is very important that you can pick the one that fits your needs and your situation because choosing the best plan is the final decision that affects every doctor visit for the next 12 months.

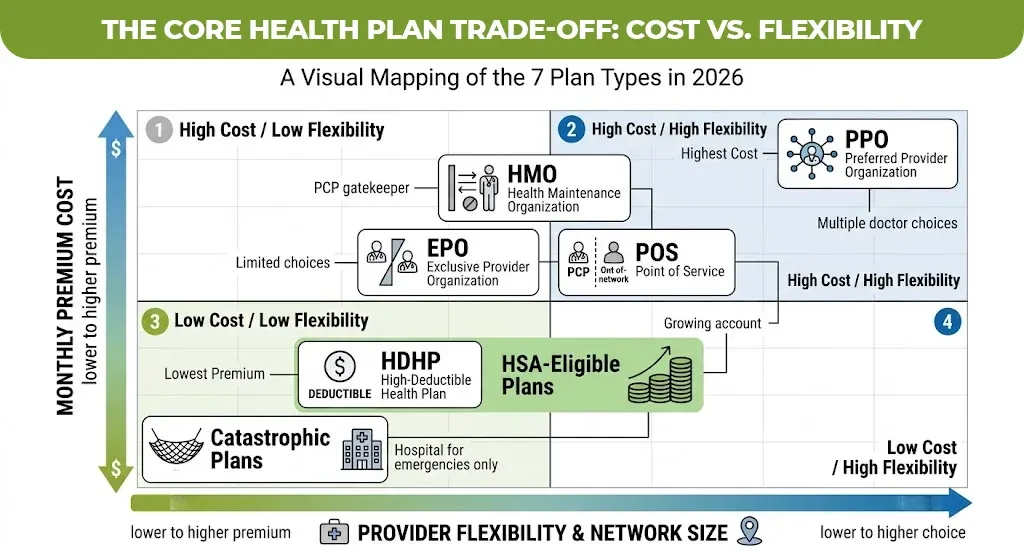

7 Types of Health Insurance Plans

The seven types of health insurance plans that are issued by the U.S. Centers for Medicare & Medicaid Services (CMS), and these plans are,

- HMO, Health Maintenance Organization

- PPO, Preferred Provider Organization

- EPO, Exclusive Provider Organization

- POS, Point of Service

- HDHP, High-Deductible Health Plan

- HSA Eligible Plans, Paired with a Health Savings Account

- Catastrophic Plans, For young adults and hardship cases

Each of these types of health insurance plans is specially made around the different situations like cost vs flexibility. Understanding where you land on that thing is the fastest way to make the right choice.

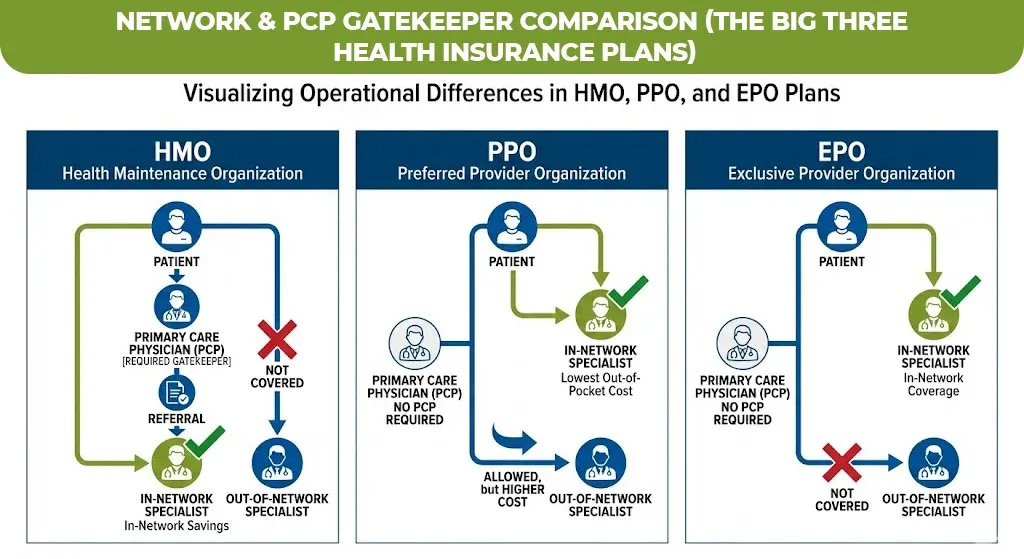

HMO Vs. PPO Vs. EPO: The Big Three Health Insurance Types Of Plans Compared

These are the three most common types of employer health insurance plans that are offered in the workplace. Here is the quick table to get better understanding.

| Feature | HMO | PPO | EPO |

| Primary Care Physician Required? | Yes | No | No |

| Referral Needed for Specialists? | Yes | No | No |

| Out-of-Network Coverage? | No (emergencies only) | Yes (higher cost) | No |

| Average Monthly Premium (2026) | Lower | Higher | Moderate |

| Best For | Cost-conscious, consistent care | Flexibility seekers | Mid-range budget, in-network only |

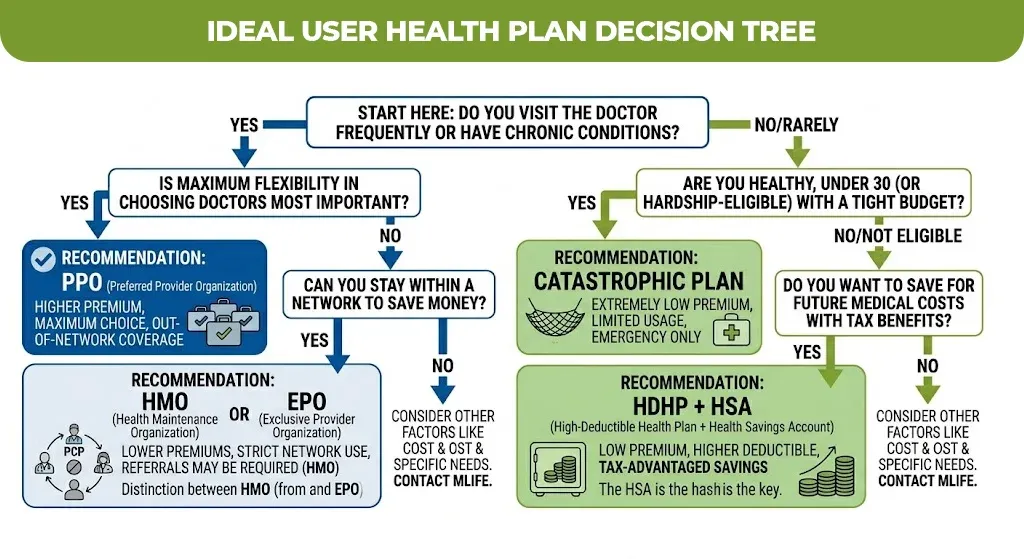

HMO Plans: Low Cost, But Low Flexibility

An HMO is the most restrictive plan of the different types of health insurance plans, and also this plan is most affordable as compared to others.

You choose one primary care physician PCP who acts as your healthcare gatekeeper. Every specialist visit requires a referral from that PCP. You stay entirely within the plan’s network or pay out of pocket.

Who should choose an HMO

People who need a predictable, low cost coverage, also the ones who travel, and already have a primary doctor they like. According to KFF’s 2025 Employer Health Benefits Survey, HMOs remain the second most commonly offered plan type by employers after PPOs.

PPO Plans: Maximum Flexibility, Higher Price Tag

A PPO plan lets you visit any doctor you want to, even without a referral. If you choose doctors in the network, then you have to pay less. If you go outside the network, you can still get care, but it will cost you even more.

PPOs are the most popular of all types of health insurance plans in the U.S. employer market. The tradeoff is real like PPO premiums average 20–30% higher than comparable HMO plans.

EPO Plans – The Middle Ground Most People Miss

An EPO is a hybrid. Like a PPO, you do not need a referral for specialists. Like an HMO, you must stay in the network or pay the full bill yourself.

EPOs are one of the most underrated different types of health insurance plans, they often cost less than a PPO while offering more specialist access than an HMO.

POS Plans: Referrals Required, Some Out-of-Network Access

A POS plan is a blend of HMO and PPO features. You designate a primary care physician like in an HMO, need referrals for specialists, but have to retain some out of the network coverage unlike a standard HMO.

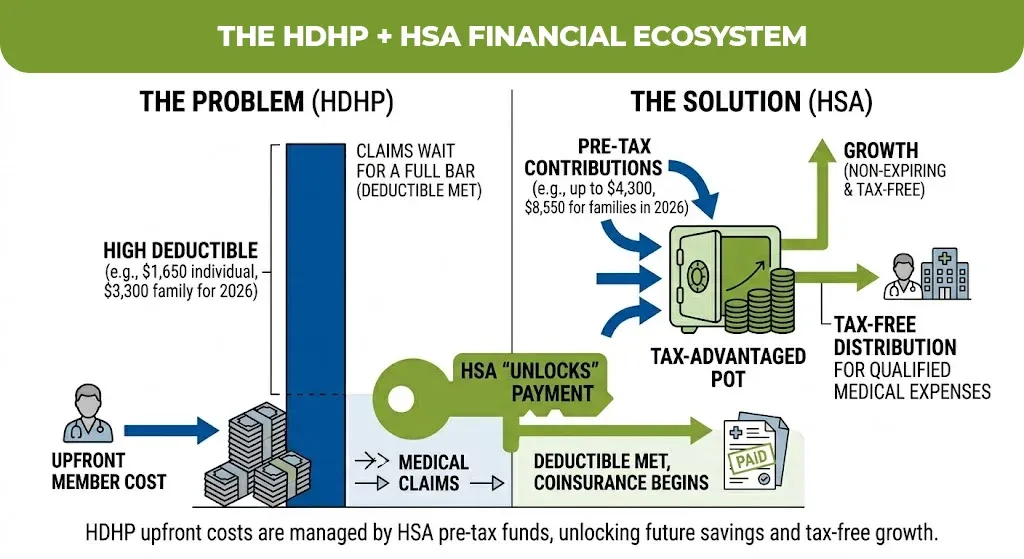

HDHPs and HSA-Eligible Plans: Built for Healthy People Who Plan Ahead

A High Deductible Health Plan that is HDHP, comes with the lower monthly premiums but a higher deductibles like the IRS defines 2026 HDHPs as plans with deductibles of at least $1,650 for individuals and $3,300 for families.

The big advantage of an HDHP is that you can use it with a Health Savings Account HSA. In 2026, you can put up to $4,300 a year into an HSA that can be $8,550 for families. The best part is that the money doesn’t expire, it will stay in your account, also grow over time, and you don’t have to pay tax on it.

Who should choose an HDHP + HSA

This plan is best for young people, healthy people who don’t go to the doctor often and want to save money for future medical costs with tax benefits.

Who should avoid it

Anyone who is managing a chronic condition with the frequent specialist visits or prescriptions. You will hit that deductible fast, and the the savings will not offset the costs.

Catastrophic Plans: Last Resort or Smart Backup?

Catastrophic plans cover the worst case scenarios like hospitalizations, surgeries, and also the major emergencies at very low premiums. But they come with extremely high deductibles (can be $9,200+ in 2026 and cover almost nothing below that threshold.

They are only available to people under 30, or those who qualify for a hardship exemption. Among the two types of health insurance plans least understood by consumers, catastrophic plans rank high, many people assume that they are “bad” plans, when in reality they are a legitimate option for someone young and healthy with a tight budget.

Types of Private Health Insurance Plans vs. Employer Plans: What’s the Difference?

Types of private health insurance plans purchased on the individual market through HealthCare.gov or state exchanges and employer-sponsored plans use the same plan structures like HMO, PPO, EPO, etc. The difference is in who’s paying and how much.

Employer plans typically cover 70–80% of the premium cost on your behalf, making them almost always the better financial deal when available. Individual market plans under the ACA may qualify for subsidies based on income.

If your employer doesn’t offer coverage, or if you are self-employed who is comparing types of health insurance plans on the marketplace is your next step. Use HealthCare.gov’s plan comparison tool to compare costs side by side.

How to Actually Choose the Right Plan (Without Getting It Wrong)

Stop comparing plans by premium alone. The right plan depends on four things:

- How often you use healthcare

- Your preferred doctors

- Your prescriptions

- Your financial buffer

Pros And Cons

Pros

- Covers all plan types

- Easy plan comparison

- Helps avoid mistakes

- Clear 2026 insights

Cons

- Too much information

- US-focused only

- Needs careful reading

- No exact pricing

Ready to Choose Confidently?

Understanding the 7 types of health insurance plans in the USA is the first step. Knowing which one fits your exact situation is where most people get stuck.

Explore your options at M-Life Insurance

M-Life Insurance makes things very easy for you so that you can compare the plans side by side that are based on your real situation, not just the price tag. No matter if you are looking for group coverage, individual plans, or guidance during open enrollment, you can get clear, honest answers without the sales pressure.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.