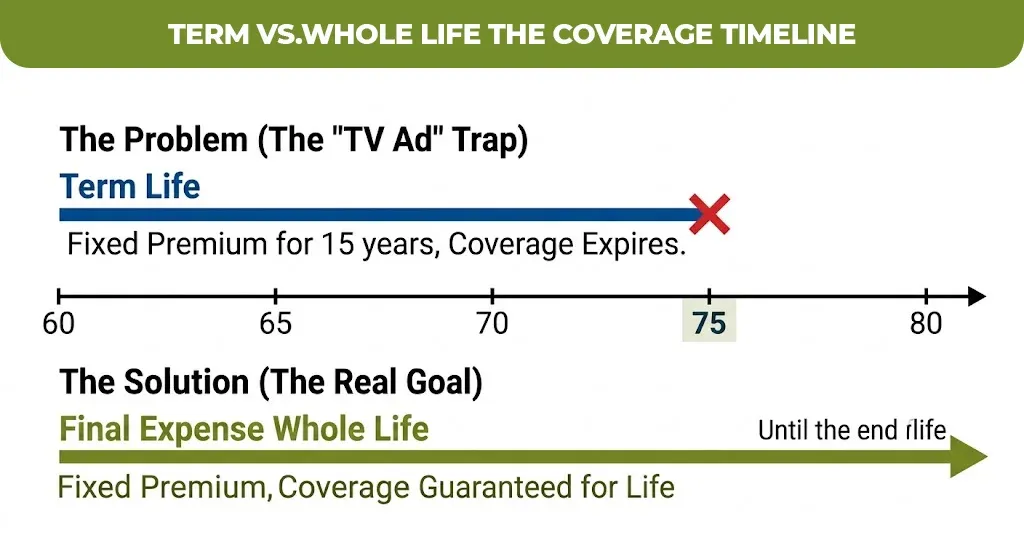

Picture this, there is a 74 years old woman who sees the TV commercial in which he sees that they are promising life insurance for $9.95 a month. She immediately signs up, relieved that she is covered. Three years later, her daughter discovered that the policy payout is less than $3000 and this is not the amount that can cover the funeral expenses.

That’s not a made up scenario. It happens every day with products marketed vaguely as burial insurance or senior life coverage, with the word whole life buried in the fine print. If you or someone you love is shopping for final expense whole life insurance, the difference between a well chosen policy and a poorly marketed one can be $5,000 to $8,000 in uncovered costs left to your family.

This guide gives you the straight answer, like no insurance jargon, no vague platitudes.

What Is Whole Life Final Expense Insurance, Exactly?

Final expense whole life insurance is a permanent, small cash value life insurance policy that is designed to cover end of life costs, and it never expires as long as you pay your monthly premiums.

This is not like a term life plan, in which it covers you for a set number of years and then stops, whole life insurance for final expenses lasts your entire life. The premium you lock in today is the premium you pay forever. It won’t increase when you turn 75. It won’t get cancelled because your health declined.

The coverage can be $5000-$25,000 and approval is usually required only a short health questions. Also there is no medical exam and no blood draw. The death benefit goes directly to the beneficiary. The beneficial letter can use this amount for the funeral expenses, outstanding medical bills or anything else.

It’s often called burial insurance, funeral insurance, or a whole life final expense policy. All of these terms describe the same product.

Why the Cost of Doing Nothing Is Higher Than You Think

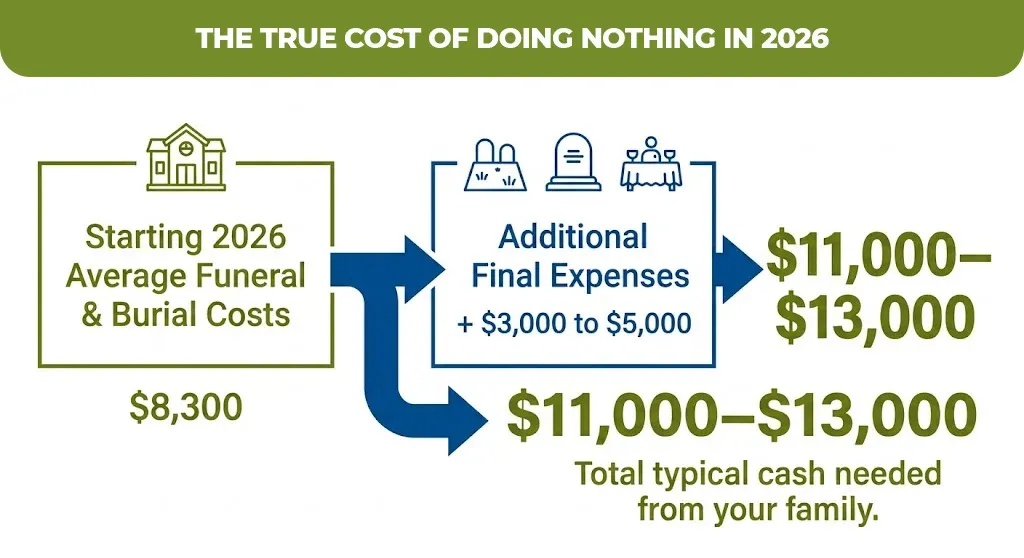

According to the National Funeral Directors Association, the average cost of a funeral with viewing and burial in 2026 is $8,300, and that’s only the funeral home’s fees. Once you add a cemetery plot, headstone, vault, flowers, and a post service reception, then all in total prices climbs to $11,000 and $13,000.

And that’s before final medical bills. End-of-life costs in the U.S. average $88,300 when you include the final year of medical expenses that is approximately $80,000 in medical care plus $8,300 in burial costs, per MoneyGeek’s 2026 analysis of NFDA and LIMRA data.

Most families don’t have $10,000 sitting in a savings account designated for this. A final expense whole life insurance policy replaces that problem with a fixed monthly premium that, for most seniors, costs less than a streaming subscription bundle.

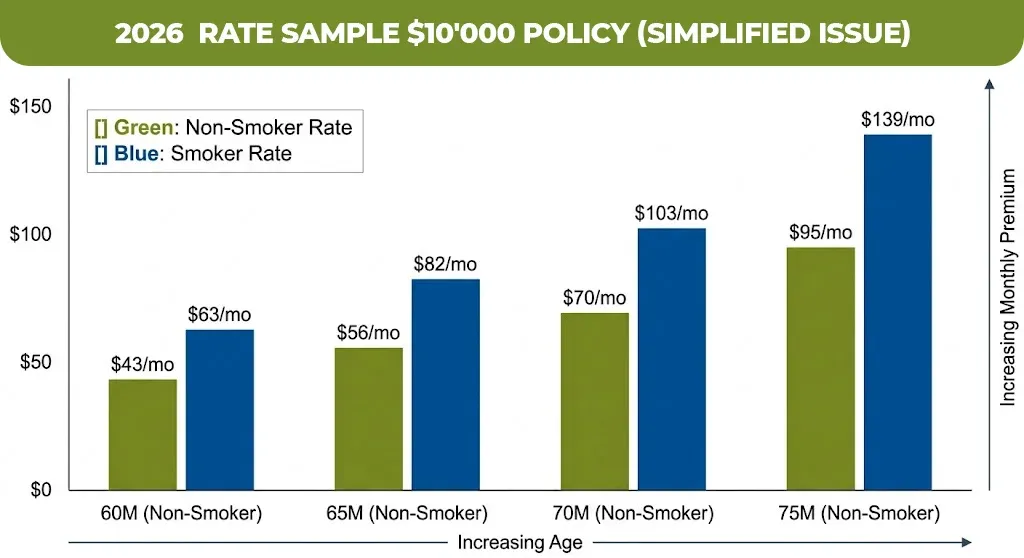

Final Expense Whole Life Insurance Rates: What You’ll Actually Pay in 2026

Rates vary by age, gender, tobacco use, and the type of policy you choose. Here’s what real 2026 data shows for a $10,000 policy:

Simplified Issue (Health Questions, No Exam — Recommended if You Qualify)

| Age | Female (Non-Smoker) | Male (Non-Smoker) | Female (Smoker) | Male (Smoker) |

| 60 | $33/mo | $43/mo | $48/mo | $63/mo |

| 65 | $42/mo | $56/mo | $61/mo | $82/mo |

| 70 | $55/mo | $70/mo | $80/mo | $103/mo |

| 75 | $73/mo | $95/mo | $107/mo | $139/mo |

| 80 | $100/mo | $130/mo | $147/mo | $191/mo |

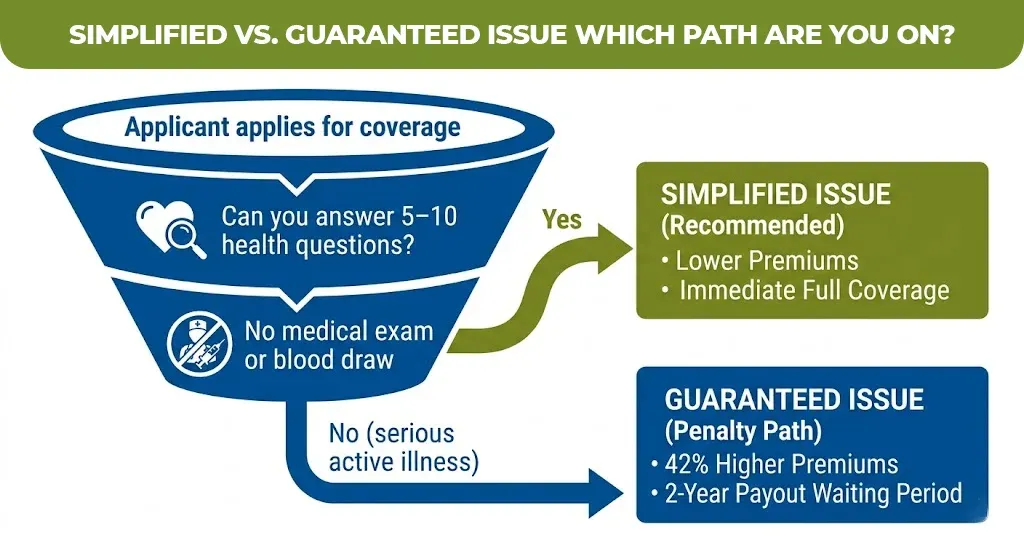

Guaranteed Issue (No Health Questions — Anyone Qualifies, But at a Cost)

Guaranteed issue policies cost approximately 42% more per month than simplified issue and include a 2-year waiting period before the full death benefit pays. InsuranceGeek’s 2026 data shows a 70-year-old male pays $69.78/month for $10,000 in simplified issue coverage versus $99.18/month for guaranteed issue.

The rule of thumb

If you can answer a short healthcare questions form without disqualifying the condition then a simplified issue is almost always a better choice for you. If serious conditions like and stage kidney diseases, any active cancer or terminal illness are present then guaranteed issue is your path to the coverage.

Simplified Issue vs. Guaranteed Issue: Which One Do You Need?

This is the most important decision most people get wrong, and agents who push guaranteed issue on healthy applicants cost them hundreds of dollars a year unnecessarily.

| Factor | Simplified Issue | Guaranteed Whole Life / Guaranteed Issue |

| Health Questions | Short questionnaire (5–10 questions) | None |

| Medical Exam | Not required | Not required |

| Waiting Period | Usually none (day-one coverage) | 2–3 years for natural death |

| Monthly Premium | Lower | 30–42% higher |

| Who Should Choose It | Most seniors in average health | Those with serious pre-existing conditions |

| Age Range | Usually 45–80 | Usually 45–85 |

| Coverage Amount | $5,000–$35,000 | $5,000–$25,000 |

If you’re diagnosed with a terminal illness or have had a major cardiac event in the last two years, simplified issue may decline you, and guaranteed issue becomes the right answer. Otherwise, do not pay the premium penalty.

How to Find the Best Final Expense Whole Life Insurance Rates Right Now

The biggest mistake is going directly to one carrier. Each company weights your health conditions differently, what Carrier A declines, Carrier B may approve at standard rates.

- Determine your coverage target

- Know your health profile

- Compare at least three A-rated carriers

- Check for a waiting period

- Confirm AM Best rating.

Ready to Compare? One Practical Step Before You Buy

If you’ve read this far, you’re better informed than most seniors who buy the first policy they see advertised on TV. You know what simplified issue means, why guaranteed issue costs more, and why shopping three carriers beats calling one.

If you want unbiased help comparing real rates, without a high-pressure sales call then Mlife Insurance works with multiple A-rated carriers to find the right fit for your health profile and budget. There’s no obligation, and the quotes are free.No commitment required. Just accurate numbers so you can decide with clarity.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.