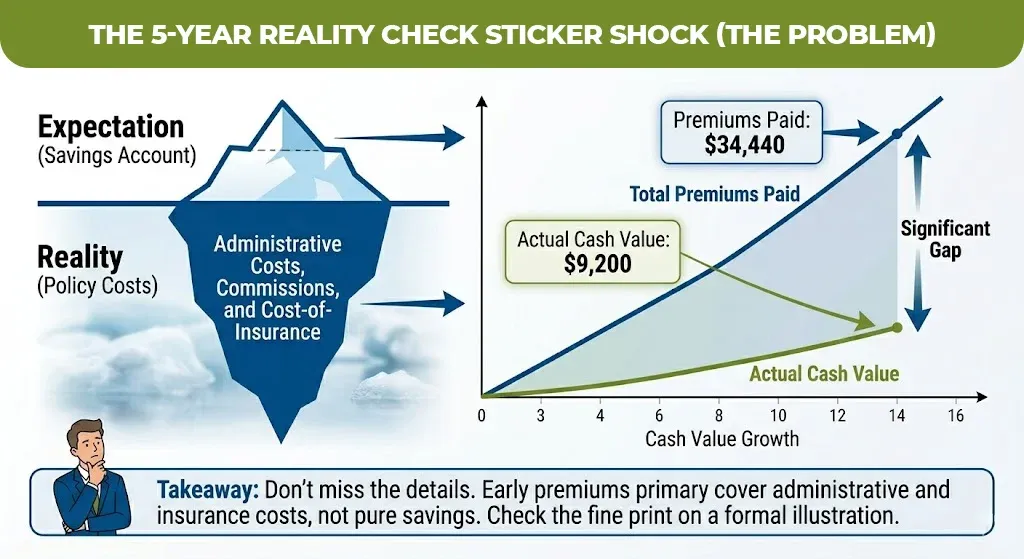

A 40 year old man is quoted $574 a month for a $500,000 whole life policy. He signs up because the agent told him it’s like a savings account.Five years later, his cash surrender value is $9,200 , on $34,440 in premiums paid.

He didn’t use a whole life insurance calculator before buying. He had no idea how slowly cash value builds in the first decade, or that the spread between carriers can run hundreds of dollars per month for identical coverage.

Before you commit to a policy that will likely run for decades, you need two numbers upfront: what your premium will be, and how your cash value grows year by year. This guide gives you both with real 2026 data and explains what online calculators show you versus what they can’t.

What a Whole Life Insurance Calculator Actually Tells You

A whole life insurance policy calculator estimates the three main things that are your annual or monthly premium, your projected cash value at a future date, and also for the participating policies, potential dividend-boosted growth on top of the guaranteed baseline.

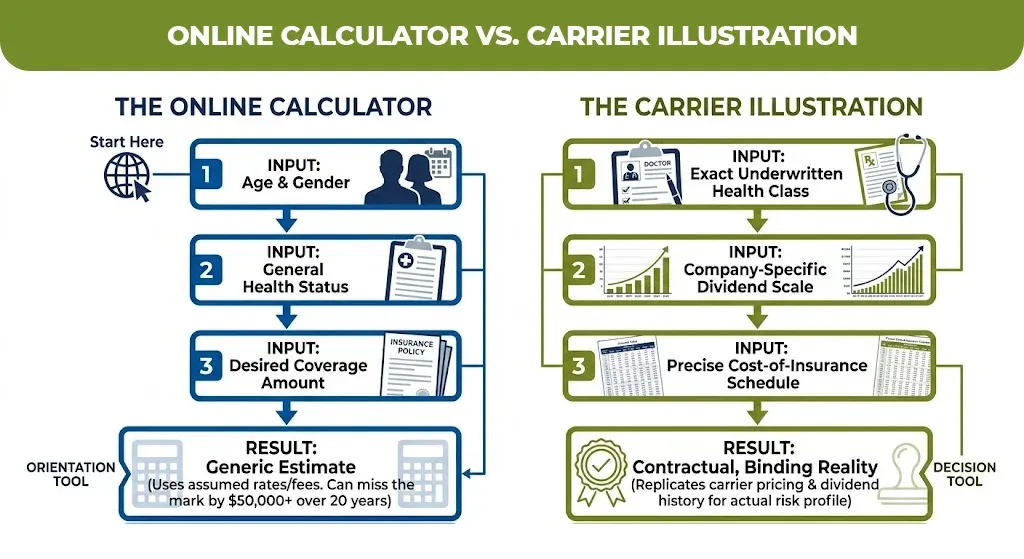

Most online calculators ask for your age, gender, health status, coverage amount, and whether you want to pay premiums for life or for a limited period 10-pay, 20-pay. From those inputs, the calculator runs your numbers against actuarial pricing models.

What it can’t do is replicate a real carrier illustration. An online tool uses a single assumed interest rate and generic fees. A formal illustration from a carrier like New York Life or Mutual of Omaha uses your actual health class, the specific dividend scale, and the precise cost-of-insurance schedule for that product. The gap between a calculator estimate and a real illustration can exceed $50,000 in projected cash value over 20 years.

Use a whole life insurance cost calculator to get oriented and eliminate options. Use a formal carrier illustration to actually decide.

2026 Whole Life Insurance Premium Rates by Age and Coverage

Here’s what real premium data looks like in 2026, sourced from MoneyGeek’s analysis of over 50 A-rated carriers, for non-smoking applicants in average health:

$250,000 Whole Life Coverage — Monthly Premium Estimates

| Age | Female | Male |

| 30 | $150/mo | $185/mo |

| 40 | $270/mo | $325/mo |

| 50 | $430/mo | $510/mo |

| 60 | $680/mo | $820/mo |

| 70 | $1,100/mo | $1,340/mo |

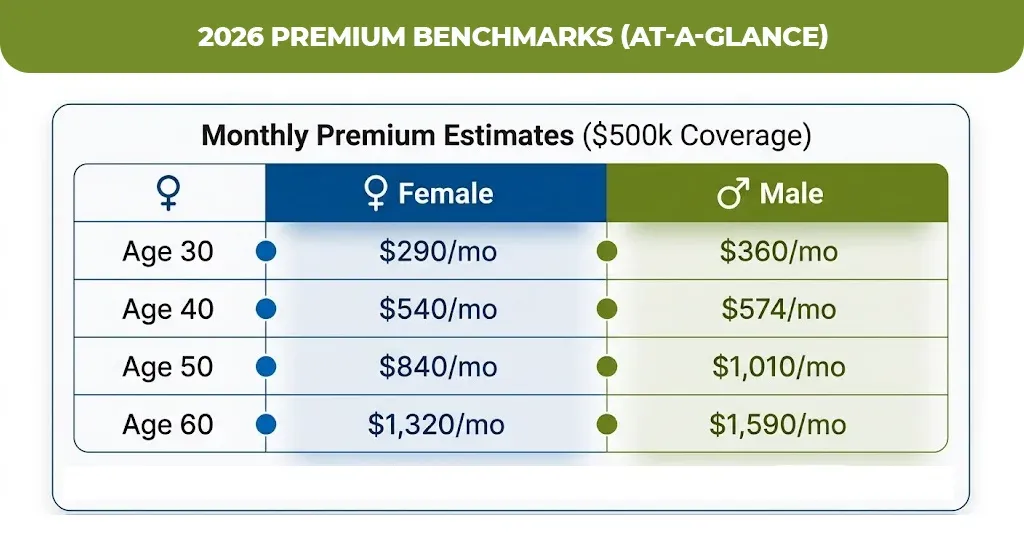

$500,000 Whole Life Coverage — Monthly Premium Estimates

| Age | Female | Male |

| 30 | $290/mo | $360/mo |

| 40 | $540/mo | $574/mo |

| 50 | $840/mo | $1,010/mo |

| 60 | $1,320/mo | $1,590/mo |

| 70 | $2,140/mo | $2,600/mo |

How the Whole Life Insurance Cash Value Calculator Works — Year by Year

Cash value grows slowly in the first decade. Most of your early premium covers the insurer’s administrative costs and the cost of the death benefit itself, not your savings account.

According to MoneyGeek’s 2026 analysis, whole life cash value grows at a fixed guaranteed rate of roughly 2% to 4% annually after the initial policy years. For comparison, high yield savings accounts paid 4% to 5% in 2025 with the key difference being that whole life cash value grows tax-deferred and can be accessed via policy loans without a credit check.

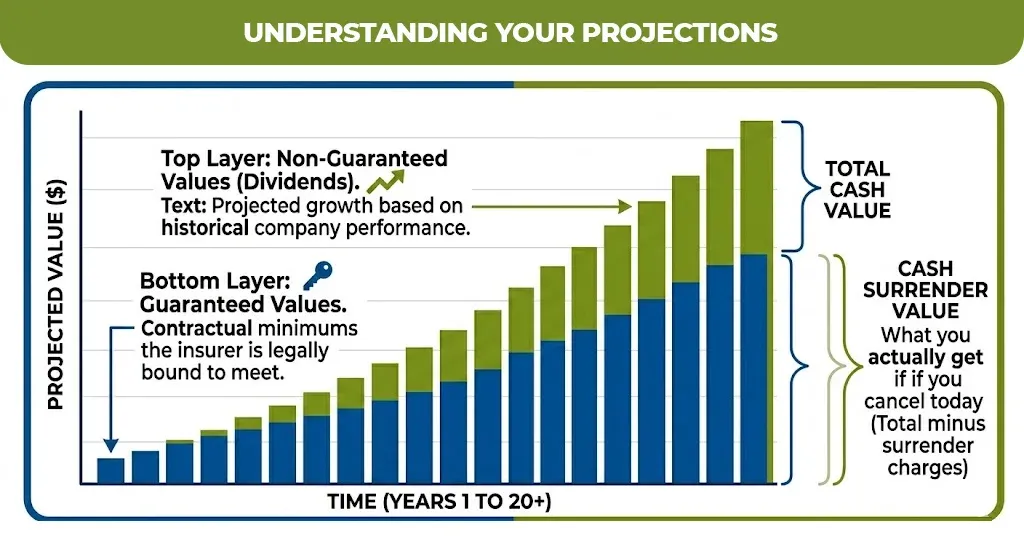

Guaranteed vs. Non-Guaranteed Cash Value Projections

Every whole life insurance policy cash value calculator will show you two columns:

| Projection Type | What It Means | Reliable? |

| Guaranteed values | Contractual minimums the insurer is legally bound to meet | Yes, written into the policy |

| Non-guaranteed (dividend) values | Projected growth if the company pays dividends at the current scale | Not guaranteed but many mutual insurers have paid dividends continuously for 100+ years |

| Cash surrender value | What you’d receive if you cancel the policy today (guaranteed minus any surrender charges) | Yes but varies by year |

State Farm vs. New York Life vs. Mutual of Omaha: Calculator Comparison

People frequently search for carrier-specific calculators before choosing. Here’s what the data shows for each in 2026:

State Farm Whole Life Insurance Calculator

State Farm offers a whole life calculator on its website tied to its own product illustrations. It’s straightforward to use, but State Farm is a captive insurer like their tool only quotes State Farm products. If you’re comparing across the market, you’ll need additional sources.

New York Life Whole Life Insurance Premium Calculator

New York Life’s calculator and formal illustrations tend to reflect higher premiums but strong dividend scales, given NY Life’s mutual ownership structure and consistent dividend history. The New York Life whole life insurance calculator is best used alongside an agent conversation, the tool generates leads, not final pricing.

Mutual of Omaha Whole Life Insurance Calculator

Mutual of Omaha is frequently cited as the most affordable option for whole life coverage under $50,000, making it a top pick for final expense planning. Their calculator is straightforward, though like all carrier tools it only quotes their own products.

Single Premium and Child Whole Life Insurance: Calculator Inputs Are Different

Single premium whole life insurance works very different from the standard policies. You have to pay one lump sum upfront that is around $25,000 to $100,000 and the policy is fully paid up immediately. Cash value starts accumulating from day one at a higher base, and the single premium whole life insurance calculator asks only for your lump sum amount, age, gender, and health class.

The IRS classifies most single premium policies as Modified Endowment Contracts (MECs), which changes how loans and withdrawals are taxed. This doesn’t eliminate the value, it just means you need to understand the tax treatment before funding.

Child whole life insurance calculators work on the same inputs but with dramatically different premium outputs. A $50,000 policy for a newborn can run as low as $20–$30 per month. The advantage is locking in insurability before any health conditions develop, and the cash value has 50+ years to compound before the child would ever need to access it.

What a Whole Life Insurance Calculator Excel Template Can Show You

Some buyers prefer building their own projection rather than trusting a vendor tool. A basic whole life insurance cash value calculator Excel model uses four inputs:

- Annual premium

- Guaranteed interest rate

- Number of years

- Dividend crediting rate

The formula logic, each year, your cash value equals last year’s cash value, plus the net premium allocated to cash value, plus interest credited at the guaranteed rate. If the policy pays dividends, you add that figure as a separate column using the current dividend scale.

Ready to Get an Accurate Number? One Next Step That Costs Nothing

Most online whole life insurance calculators give you directional estimates. The number that actually matters is the one on a formal carrier illustration that is specially designed to your age, your health class, and the specific policy structure.

Mlife Insurance works with multiple A rated carriers to pull real illustrations side by side, so you can see guaranteed cash value, dividend projections, and exact premiums before committing to anything.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.