You are about to make the decision that will affect your family’s financial safety for the decades. And there is a good chance to advise you have been given is wrong for your situation.

Most people searching term vs whole life insurance already have an opinion from a friend, a YouTube video, or an advisor who profits from one answer. The problem is not that those sources are lying. The problem is that the right answer generally depends on your age, your income, your family structure and financial goals and most people never work through those four things before choosing.

Here is the straight answer, backed by 2026 data, so you can stop guessing.

Term vs Whole Life Insurance: Which One Should You Actually Choose?

For most of the families with the dependents and the mortgage, the term life insurance is a better starting point for them. For those who are focused on estate planning, retirement income or lifetime coverage, then the whole life insurance policy carries advantages that term life plans cannot replicate.

The honest answer is not term is always better or whole life is always a scam.Both serve different purposes. There is a mistake that most of the people will make and that is buying the cheaper option without understanding what they are giving up or buying the expensive option without understanding if they actually need it or not.

According to the 2026 Insurance Barometer Study by LIMRA and Life Happens, approximately 100 million Americans currently lack adequate coverage. The primary reason is not that they chose wrong. It is that they never chose at all, often because they overestimated the cost.

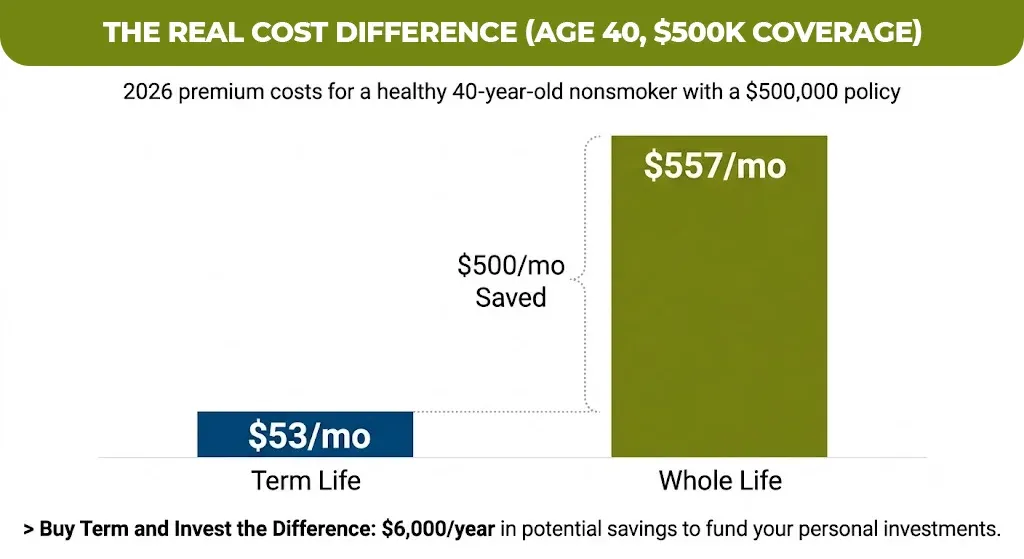

The Real Cost Difference: Whole Life Insurance vs Term Life Insurance

The price cap between these two policy type is bigger than most of the people expect.According to MoneyGeek’s 2026 rate analysis, a healthy 40-year-old nonsmoker pays roughly $53 per month for a $500,000 20-year term policy. The same person pays around $557 per month for a comparable whole life policy.

That is a monthly difference of roughly $500 or $6,000 per year.

| Policy Type | Age 30 (Monthly) | Age 40 (Monthly) | Age 50 (Monthly) |

| 20-Year Term ($500K) | $20 | $53 | $130 |

| Whole Life ($500K) | $200 | $557 | $1,100+ |

| Universal Life ($500K) | $150 | $336 | $765 |

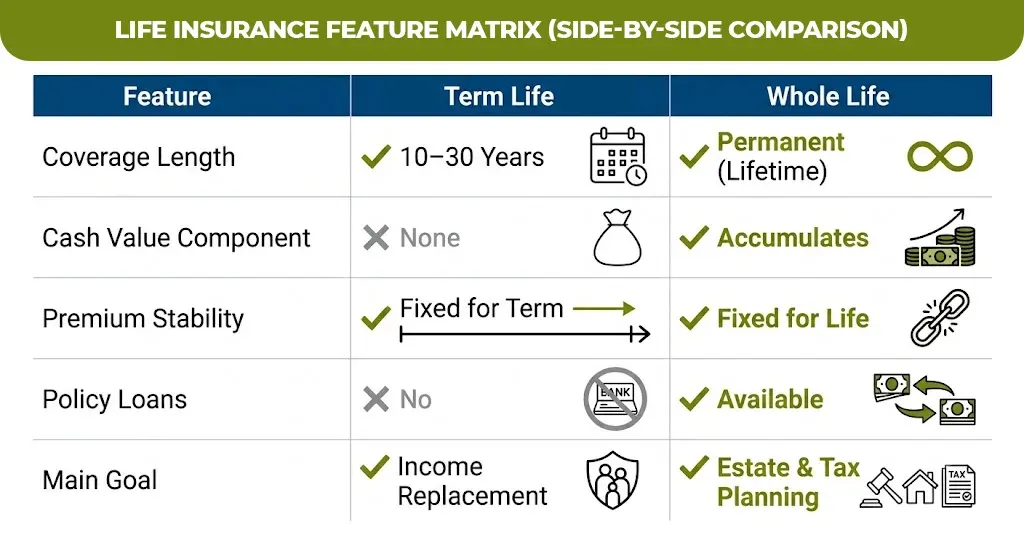

What You Get With Each Policy: A Side-by-Side Comparison

| Feature | Term Life Insurance | Whole Life Insurance |

| Coverage Length | Fixed term (10, 20, 30 years) | Lifetime (as long as premiums paid) |

| Death Benefit | Paid if death occurs during term | Guaranteed, paid at any death |

| Cash Value | None | Builds over time, tax-deferred |

| Premium Cost | Low, fixed for the term | High, fixed for life |

| Loan Access | No | Yes, borrow against cash value |

| Investment Component | None | Grows at guaranteed rate |

| Best For | Income replacement, mortgage coverage | Estate planning, lifelong needs |

| Expiry Risk | Yes, outliving the term is common | No expiry risk |

The core difference comes down to this: term life insurance is protection for a window of time. Whole life insurance is protection plus a savings vehicle for your entire life.

Who Should Choose Term Life Insurance

Term life is the right choice when your primary goal is income replacement during your working years. If someone depends on your income and you would not be able to replace it from savings alone, a term policy gives them maximum coverage at minimum cost.

Term life insurance makes the most sense when:

- You have young children or dependents at home

- You carry a mortgage or significant debt

- You need high coverage now but expect your financial picture to change

- Your budget does not allow for higher premiums

- You want to invest the difference in a 401(k) or IRA yourself

The “buy term and invest the difference” strategy is widely recommended by fee-only financial planners for exactly this reason. The savings from lower premiums, invested consistently, often outperform the cash value growth inside a whole life policy over a 20-to-30-year horizon.

Who Should Choose Whole Life Insurance

Whole life insurance will make sense when you need the coverage that will not end with your working years. This will include people who want to leave a current inheritance, cover the estate taxes on large assets are building a tax sheltered component within the broader financial plan.

The casual condition in whole life insurance policy will grow tax effort and you can borrow it without triggering a taxable event. This is the flexibility and it is very genuinely valuable in the right situation.

Whole life insurance makes the most sense when:

- Your estate is large enough to trigger estate taxes

- You have maxed out other tax-advantaged accounts such as 401k, IRA, HSE

- You want guaranteed lifelong coverage regardless of health changes

- You need a financial tool that builds accessible, tax-deferred cash value

- If you are a business owner who is structuring buy sell agreement or key person insurance.

It is worth noting that whole life held approximately 36% of new premium market share in the U.S. in 2024, according to LIMRA market data. That is not a fringe product. It is actively used by a significant segment of buyers for deliberate reasons.

Term Life Insurance vs Whole Life Insurance: Common Mistakes to Avoid

- Buying too little coverage on term

- Assuming whole life is always overpriced

- Waiting to decide

- Picking the wrong term length

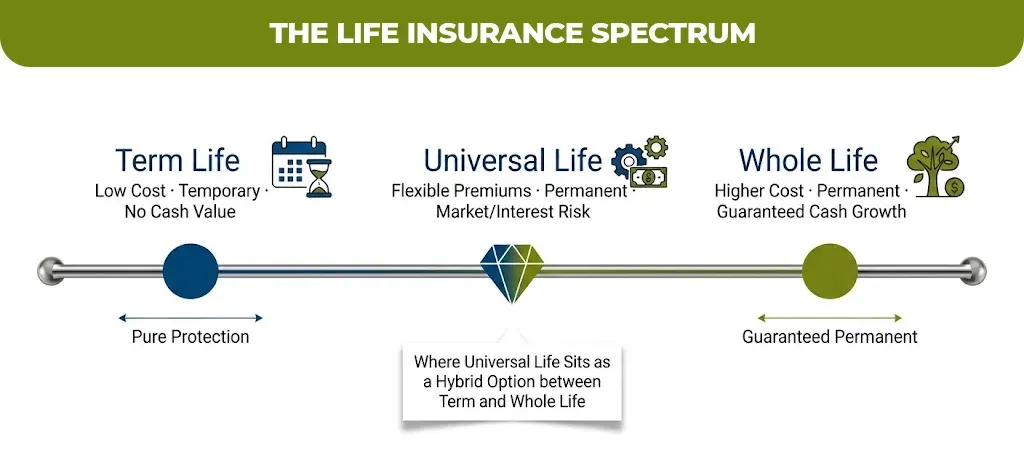

What About Universal Life Insurance?

Universal life insurance plans sit between the term and whole life. This plan will offer you lifelong coverage like a life policy but with the more flexibility in how you can pay your premiums and the cash value will grow.

This is the legitimate option for the buyers who want permanent life insurance coverage without the reduced premium structure of whole life insurance. However it will carry more internal risk than whole life policy because the cash value growth is tied to interest rates or market performance depending on the policy type. In a low rate or quality tile environment, the underfunded universal life policy and lapse.

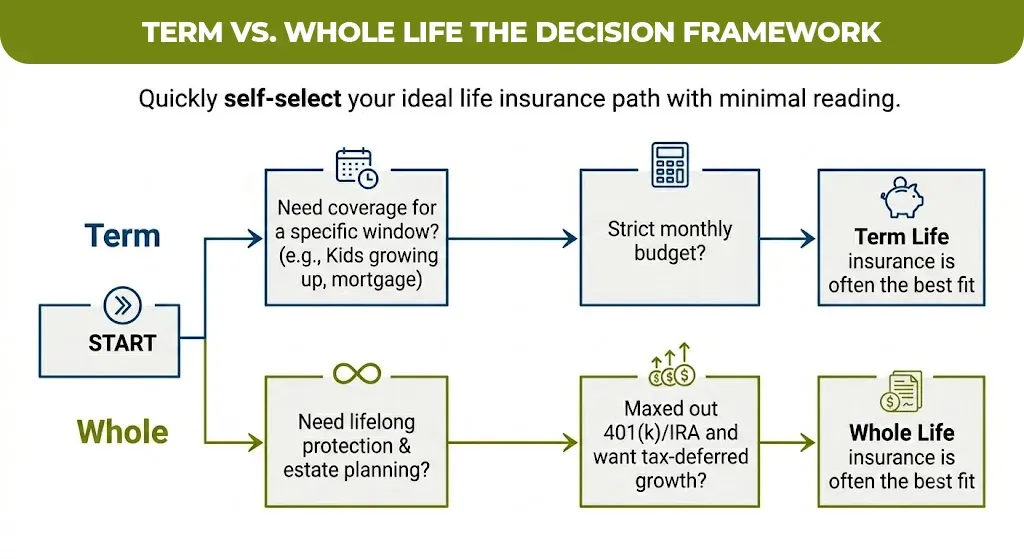

Making the Decision: A Simple Framework

Answer these four questions honestly:

How long do you need coverage?

If the answer is “until my kids are grown and my mortgage is paid,” term is probably right. If the answer is “forever,” consider whole life.

What is your budget?

If the whole life premium strains your monthly cash flow, a lapsed whole life policy protects no one. A term policy you can actually maintain is always better than a premium policy you drop.

Do you have other savings and investments?

If you already contribute to a 401(k), IRA, and have a growing emergency fund, the cash value component of whole life adds less incremental value than it would for someone without those assets.

Is this a temporary or permanent need?

Temporary needs belong in term. Permanent needs, estate planning, lifelong dependents, business succession, belong in whole life or a permanent alternative.

A Word on Getting the Right Guidance

Choosing between term and whole life insurance is not a product decision. It is a financial planning decision. The right answer changes based on your income, your debts, your family, your health, and your long-term goals.

If you are trying to figure out what that looks like for your specific situation, talking to a licensed advisor who can walk through your numbers without a product quota is worth more than any comparison article.

At mlife insurance, licensed advisors help individuals and families work through exactly this question without pressure to land on a particular product. Whether you need a straightforward term quote or want to understand how permanent coverage fits into your broader financial plan, the conversation starts with your goals, not a sales pitch.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.