Most of the people with diabetes assume they’ll either get declined or face premiums so high that coverage isn’t worth it. So they delay applying, tell themselves they’ll “sort it out later,” and leave their family unprotected for years.

That is the most expensive mistake in this space, not getting a bad rate, but never applying at all.

Life insurance for people with diabetes is not only possible in 2026, but also it is more accessible than it has ever been. But the outcome depends almost on which insurance company you approach, how you present your health history, and if your diabetes is well managed. This guide walks you through every factor that matters.

Can People with Diabetes Get Life Insurance? The Direct Answer

Yes, there are some people with diabetes who can qualify for life insurance, including the term and whole life insurance policies. According to the American Diabetes Association, approximately 38.4 million Americans have diabetes as of 2024. Insurance companies cannot afford to exclude this population entirely, and most don’t.

The word denial comes up far less often than most people can expect. Flat out declines are reserved for severe complications like kidney failure, recent amputations, or diabetes combined with serious cardiovascular disease.

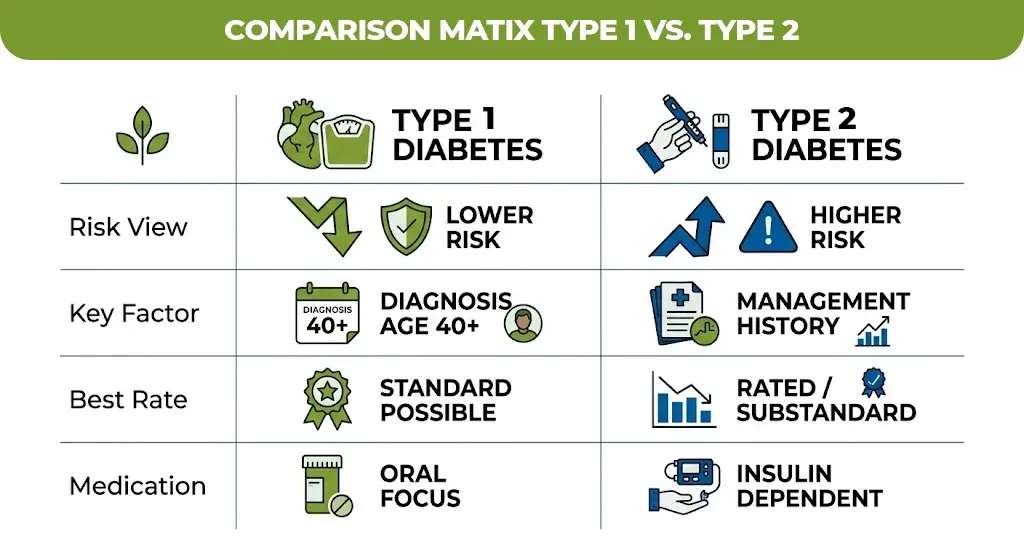

Type 1 vs. Type 2 Diabetes: How Underwriters See the Difference

The underwriters do not treat all diabetes in the same way, and understanding this can directly affect which insurance company you are choosing and what rate class you realistically qualify for.

Type 2 diabetes

Type 2 diabetes is way more common and when it is managed, it is viewed as a lower risk condition by most insurance companies. If you were diagnosed after age 40, maintain an A1C under 7.5, take oral medication with only no insulin, and have no complications, many carriers will offer you a standard rate class.

Type 1 diabetes

Type 1 diabetes involves insulin dependency from diagnosis and a longer history of managing blood sugar volatility. Underwriters view it as a higher-risk condition. That doesn’t mean coverage is unavailable, and it means fewer carriers are offering competitive rates, and your management history carries even more weight.

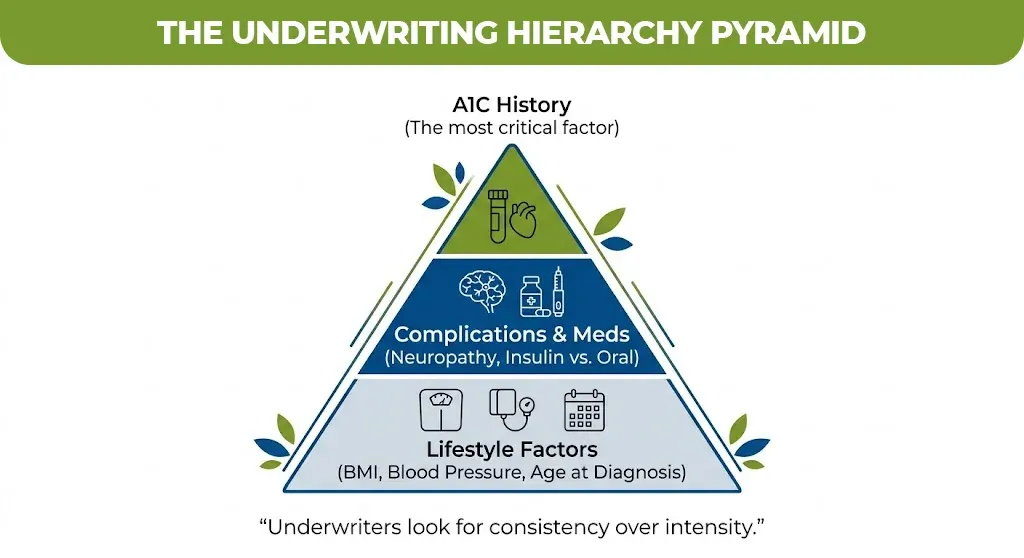

What Underwriters Actually Examine When You Apply

This is where most people get caught off guard. Life insurance underwriting for diabetes goes well beyond “do you have it.” here is the specific data an underwriter reviews

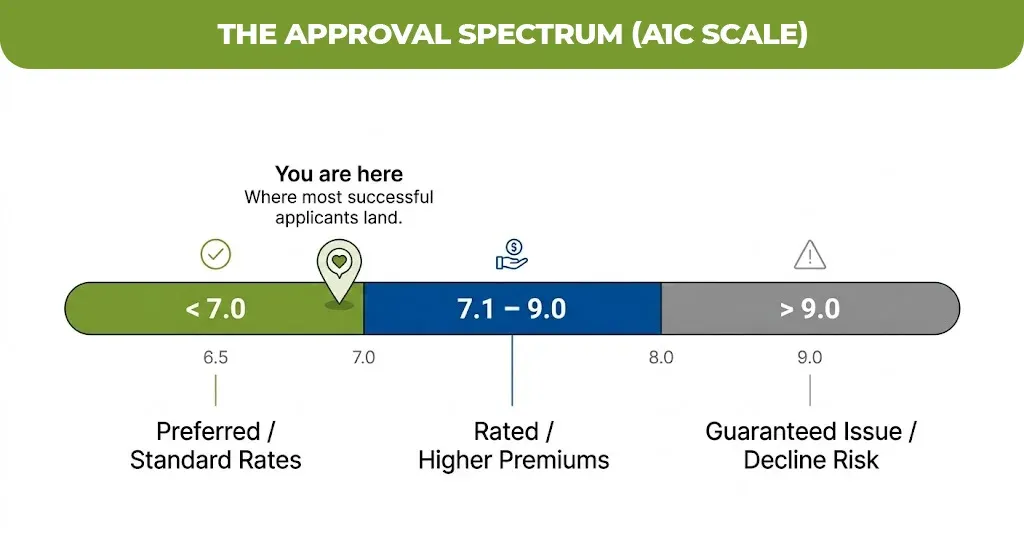

Your A1C history

This is the single most important number. An A1C consistently under 7.0 over two or more years signals controlled diabetes and typically results in the best available rate for a diabetic applicant. An A1C above 9.0 triggers either a rated policy that has the higher premium or the postpone or decline depending on other factors.

Age at diagnosis

Earlier diagnosis generally means a longer history with the condition, which underwriters factor into lifetime risk calculations

Medications and insulin use

Oral medication only is viewed more favorably than insulin. Insulin doesn’t disqualify you, it just signals a different risk tier.

Complications present or absent

Neuropathy, retinopathy, nephropathy, or cardiovascular events related to diabetes are the markers that most affect underwriting outcomes.

BMI, blood pressure, and cholesterol

These comorbid factors compound diabetes risk in underwriting models.Well-controlled blood pressure and cholesterol can partially offset a higher A1C

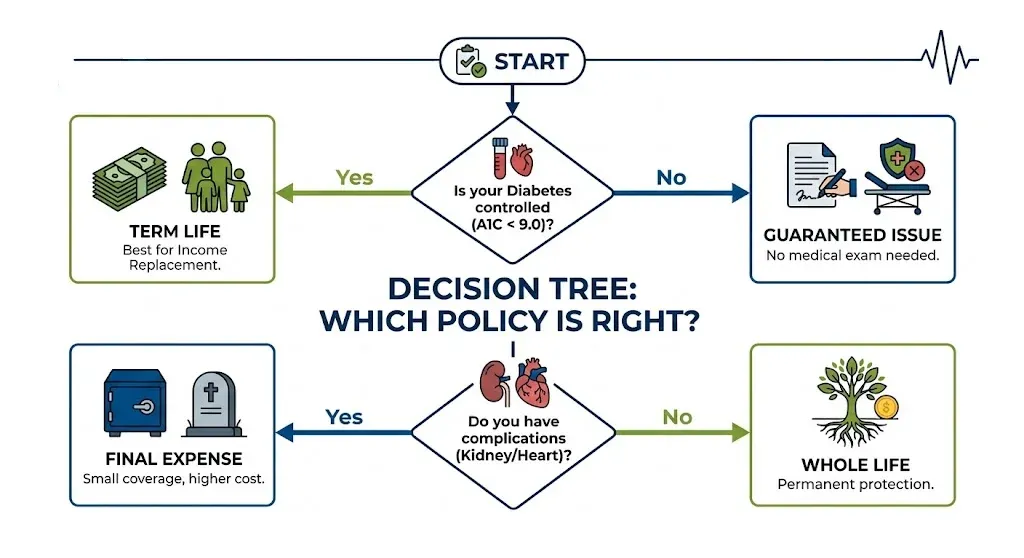

What Types of Life Insurance Are Actually Available — and Which Fits Your Situation

Not every policy type works equally well for people with diabetes. Here’s the honest breakdown:

| Policy Type | Best For | Underwriting Required | Typical Premium Impact |

| Term Life (10–30 yr) | Income replacement, mortgage protection | Full medical underwriting | 20–150% above standard depending on control |

| Whole Life | Permanent coverage, estate planning | Full medical underwriting | Higher base, but locked rate |

| Guaranteed Issue Whole Life | Severe complications, prior declines | None — no health questions | 2–4x standard premiums, low benefit caps ($5K–$25K) |

| Simplified Issue | Moderate risk, faster approval needed | Health questionnaire, no exam | 30–100% above standard |

| Final Expense Insurance | Seniors, smaller benefit needs | Minimal or none | Higher per-dollar cost, designed for burial/end-of-life |

How to Improve Your Approval Odds Before You Apply

Applying strategically matters more than applying quickly. These steps directly influence your underwriting outcome:

- Get your A1C tested first.

- Work with an independent broker, not a captive agent

- Don’t apply to multiple carriers simultaneously without guidance.

- Document your management actively

Key Pros and Cons

Pros

- Easier approval options

- Multiple policy choices

- Coverage still possible

- Flexible underwriting criteria

Cons

- Higher premium costs

- Strict health evaluation

- Limited carrier options

- Risk of denial

Life Insurance Costs for Diabetics in 2026: Realistic Numbers

Premiums can be different and it totally depending on the insurance company, but here’s a realistic range for a $250,000 20-year term policy in 2026 based on age and diabetes management:

| Age | Controlled Diabetes (A1C < 7.5) | Moderate Control (A1C 7.5–9.0) | Poorly Controlled (A1C > 9.0) |

| 40 | $90–$140/mo | $180–$280/mo | Rated or declined |

| 50 | $160–$220/mo | $300–$450/mo | Rated or declined |

| 60 | $280–$380/mo | $500–$700/mo | Likely decline or GI only |

These figures are estimates based on standard underwriting models across major carriers. Your actual premium depends on your full health profile, not diabetes alone.

Navigating Life Insurance With Diabetes as a Senior

If you are a senior with diabetes navigating these options, M-life provides straightforward information on final expense and burial insurance plans designed for people with health conditions. It’s worth reviewing what’s available for your age and health profile at Mlife Insurance, there will be no pressure, just a practical resource if you’re trying to understand your options before talking to an agent.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.