Have you ever wondered if you, as a non-US citizen, can secure life insurance in the United States? The answer is yes, but the process and requirements can be different from those for US citizens. Life insurance is an essential financial tool that provides security and peace of mind, ensuring your loved ones are protected in the event of your passing.

In this comprehensive guide, we’ll explore the world of life insurance for non-US citizens. We’ll go through the types of policies available, the eligibility criteria you’ll need to meet, the documentation required, and the benefits of securing life insurance as a non-US citizen.

Whether you’re a long-term resident, a temporary visitor, or a non-resident alien, understanding your options for life insurance in the US can help you make informed decisions to protect your family’s financial future.

Understanding Life Insurance for Non-US Citizens

Life insurance for non-US citizens is a topic that raises many questions. Can non-US citizens get life insurance in the United States? What are the requirements and options available? Understanding these aspects is crucial for those seeking financial security and peace of mind.

Life insurance for non-US citizens generally mirrors those for US citizens but with some differences. Non-US citizens may encounter stricter eligibility criteria and higher premiums due to perceived risks associated with their residency status. Despite these challenges, with the right information and guidance, non-US citizens can secure suitable life insurance coverage in the US.

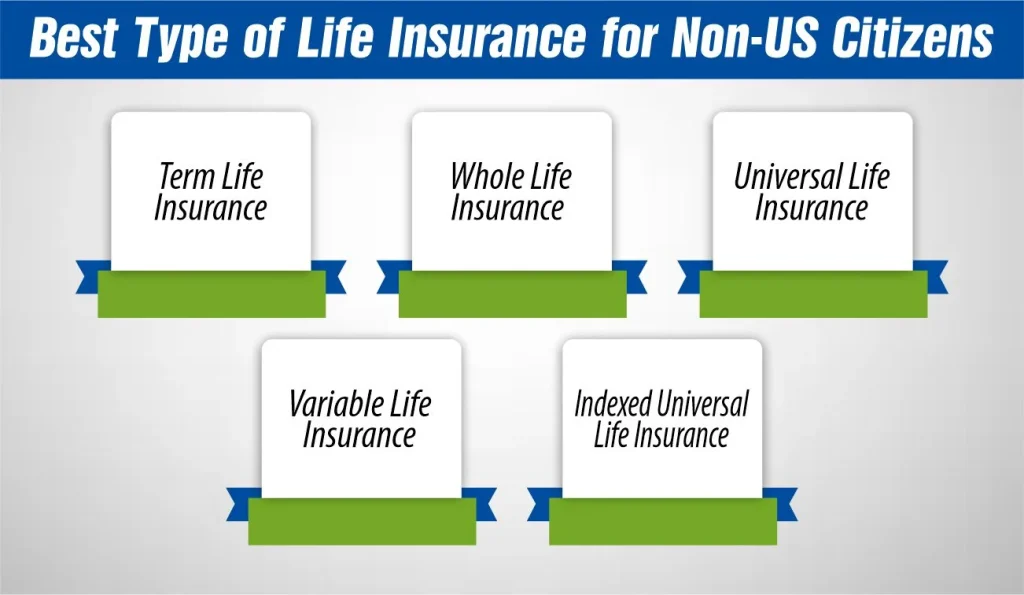

Best Type of Life Insurance for Non-US Citizens

Best Type of Life Insurance for Non-US Citizens

Choosing the best type of life insurance for non-US citizens depends on your individual needs and circumstances. Here are some common options to consider:

1- Term Life Insurance

This type of insurance provides coverage for a specific period, such as 10, 20, or 30 years. It’s generally more affordable than permanent life insurance and can be a good option if you only need coverage for a certain period, such as until your mortgage is paid off or your children are grown.

2- Whole Life Insurance

Whole life insurance provides coverage for your entire life, as long as you continue to pay the premiums. It also includes a cash value component that grows over time, which you can borrow against or use to supplement your retirement income.

3- Universal Life Insurance

Universal life insurance offers more flexibility than whole life insurance. You can adjust your premium payments and death benefit amount as your needs change. It also includes a cash value component that earns interest over time.

4- Variable Life Insurance

This type of life insurance allows you to invest the cash value component in various investment options, such as stocks and bonds. The value of your policy can fluctuate based on the performance of your investments.

5- Indexed Universal Life Insurance

The insurance policy combines the flexibility of universal life insurance with the potential for higher returns linked to a stock market index, such as the S&P 500. It offers a minimum guaranteed return, protecting your cash value from market downturns.

Before choosing life insurance for non-US citizens, consider factors such as your age, health, financial goals, and budget. Moreover, it’s also a good idea to consult with a financial advisor who specializes in working with non-US citizens to help you find the best coverage for your needs.

How Non-US Citizens can buy Life Insurance?

Non-US citizens can buy life insurance in the United States, but the process may be slightly different from that for US citizens. Here’s a general guide to how non-US citizens can buy life insurance:

1- Research and Compare Policies

Start by researching different types of life insurance policies and comparing them based on your needs and budget. Consider factors such as the coverage amount, premium cost, and policy term.

2- Find an Insurance Agent

Look for an insurance agent or broker who has experience working with non-US citizens. They can help you navigate the process and find the right policy for your needs.

3- Gather Required Documents

You’ll typically need to provide documents such as a valid passport, visa, or other proof of legal status in the US. You may also need to provide proof of income or financial stability.

4- Undergo Medical Examination

In most cases, you’ll need to undergo a medical examination as part of the application process. The insurance company will use this information to assess your health and determine your premium rate.

5- Submit Application

Once you’ve selected a policy, you’ll need to complete an application form and submit it to the insurance company along with any required documents.

6- Wait for Approval

The insurance company will review your application, including your medical exam results, and determine whether to approve your policy. This process can take several weeks.

7- Pay Premiums

If your application is approved, you’ll need to pay your premium to activate your policy. You can usually choose to pay annually, semi-annually, quarterly, or monthly.

8- Receive Policy Documents

Once your policy is active, you’ll receive a copy of your policy documents. Be sure to review them carefully to understand your coverage and any limitations or exclusions.

It’s important to note that the process and requirements for buying life insurance for non-US citizens can vary depending on the insurance company and your circumstances. However, working with an experienced insurance agent can help ensure a smooth application process.

Benefits of Life Insurance for Non-US Citizens

Life insurance offers numerous benefits for non-US citizens, providing financial security and peace of mind for themselves and their loved ones. Here are some key benefits:

Financial Protection

Life insurance provides a financial safety net for your loved ones in the event of your passing. The death benefit can help cover expenses such as funeral costs, outstanding debts, mortgage payments, and everyday living expenses.

Income Replacement

The death benefit from a life insurance policy can replace lost income, ensuring that your family can maintain their standard of living and meet financial obligations even after you’re gone.

Estate Planning

Life insurance can be an essential tool for estate planning, helping to preserve and transfer wealth to future generations. The death benefit can provide liquidity to pay estate taxes or equalize inheritances among heirs.

Business Continuity

For non-US citizens who own businesses in the United States, life insurance can help ensure continuity in the event of the owner’s death. The death benefit can be used to buy out business partners, repay business debts, or fund a succession plan.

Legacy Planning

Life insurance can be used to leave a financial legacy for future generations or support charitable causes that are important to you. The death benefit can provide a meaningful impact long after you’re gone.

Overall, life insurance is a valuable financial tool for non-US citizens, offering protection, security, and peace of mind for themselves and their families. By understanding the benefits of life insurance and choosing the right policy, non-US citizens can ensure that their loved ones are taken care of financially, no matter what the future holds.

Requirements of Life Insurance for Non-US Citizens

Life insurance requirements for non-US citizens can vary depending on the insurance company and the type of policy. However, there are some common requirements that non-US citizens typically need to meet:

- Legal Status: Non-US citizens must have legal status in the United States, such as a valid visa or other proof of legal residency.

- Age: Most insurance companies have minimum and maximum age requirements for applicants. The exact age limits can vary depending on the insurer and the type of policy.

- Health: Non-US citizens will usually need to undergo a medical examination as part of the application process. The insurance company will use the results of the exam to assess the applicant’s health and determine their premium rate.

- Documentation: Non-US citizens will need to provide certain documents as part of the application process. This typically includes a valid passport, visa, or other proof of legal status in the US, as well as proof of income or financial stability.

- Policy Type: The requirements for different types of life insurance policies can vary. For example, term life insurance may have different requirements than whole life insurance or universal life insurance.

- Premium Payment: Non-US citizens will need to pay their premium to activate their policy. The premium amount can vary depending on factors such as age, health, and the type of policy.

- Residency: Some insurance companies may require non-US citizens to have a certain length of residency in the US before they can apply for life insurance.

It’s important for non-US citizens to carefully review the requirements of the insurance company they are interested in and to work with an experienced insurance agent who can help guide them through the application process.

Cost of Life Insurance for Non-U.S. Citizens

The cost of life insurance for a non-US citizen can vary based on several factors, including age, health, coverage amount, and the type of policy. Here’s a table showing estimated monthly premiums for a $500,000 term life insurance policy for non-US citizens of different ages and health statuses:

| Age | Excellent Health | Good Health | Average Health |

| 30 | $20 – $30 | $30 – $40 | $40 – $50 |

| 40 | $30 – $40 | $40 – $50 | $50 – $60 |

| 50 | $50 – $60 | $60 – $70 | $70 – $80 |

| 60 | $80 – $90 | $90 – $100 | $100 – $110 |

Please note that these are rough estimates and actual premiums may vary based on individual circumstances and the insurance company. It’s best to consult with an insurance agent to get a more accurate quote based on your specific situation.

Conclusion

Life insurance for non-US citizens is a complex but achievable goal. By understanding the requirements and working with an experienced insurance agent, non-US citizens can find the right life insurance policy to meet their needs. If you’re a non-US citizen considering life insurance in the US, it’s essential to do your research and explore your options to find the best coverage for you.

FAQs

1- Can non-US citizens living abroad buy life insurance in the US?

Yes, non-US citizens living abroad can often purchase life insurance in the US, provided they meet the eligibility criteria set by the insurance company.

2- Will my immigration status affect my ability to get life insurance?

Your immigration status can impact your eligibility and the cost of life insurance. However, many insurance companies offer coverage options for non-US citizens with various immigration statuses.

3- Can non-US citizens get the same coverage options as US citizens?

Non-US citizens may have access to similar coverage options as US citizens, but they may face different eligibility requirements and premium rates based on factors such as residency status and country of origin.

4- Are there any restrictions on the coverage amount for non-US citizens?

While there are generally no restrictions on the coverage amount for non-US citizens, the maximum coverage available may vary depending on the insurance company and the individual’s financial circumstances.

5- Can non-US citizens living in the US temporarily buy life insurance?

Yes, non-US citizens living in the US temporarily, such as students or temporary workers, can typically buy life insurance. However, they may need to provide proof of legal residency or visa status.

References:

https://www.quotacy.com/life-insurance-for-non-us-citizens/

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.