Importance of Guaranteed Death Benefit in Life Insurance Policies

The guaranteed death benefit stands as a crucial and defining aspect of life insurance policies, offering numerous benefits and playing a pivotal role in financial planning. Here’s why it holds significant importance:

Financial Security for Loved Ones

The primary purpose of a guaranteed death benefit is to provide financial protection to your beneficiaries after your passing. It ensures that your loved ones receive a tax-free lump sum payment, enabling them to cover immediate expenses such as funeral costs, outstanding debts, mortgage payments, and ongoing living expenses.

Certainty and Peace of Mind

The assurance of a guaranteed death benefit provides peace of mind to policyholders. Knowing that regardless of when death occurs, their beneficiaries will receive a predetermined sum of money offers a sense of certainty and security, allowing individuals to focus on their lives without worrying about their family’s financial future.

Income Replacement

For families reliant on the income of the insured individual, the death benefit serves as a replacement for lost income, ensuring that beneficiaries maintain their standard of living and financial stability.

Legacy and Charitable Giving

Life insurance policies with guaranteed death benefits can be used to leave a legacy or support charitable causes. By naming charitable organizations as beneficiaries, individuals can make a lasting impact on causes they care about deeply.

Predictable Financial Planning

The fixed nature of the guaranteed death benefit allows for better financial planning. Beneficiaries know the exact amount they will receive, facilitating better long-term financial management and stability.

What Makes Guaranteed Death Benefits Different from Other Types of Life Insurance?

There are several different types of life insurance, and each type has its own unique features and benefits. Guaranteed death benefits are different from other types of life insurance in several key ways.

The policyholder will be guaranteed a death benefit no matter when they pass away. This means that if you pass away tomorrow or twenty years from now, your beneficiaries will receive the death benefit.

The government ensures the tax-free payment of the annuity guaranteed death benefit. This can be a significant advantage for your beneficiaries, as they will not have to pay taxes on the death benefit.

They do not require a medical exam. It can be beneficial for those who are not in good health, as they may not be able to qualify for other types of life insurance.

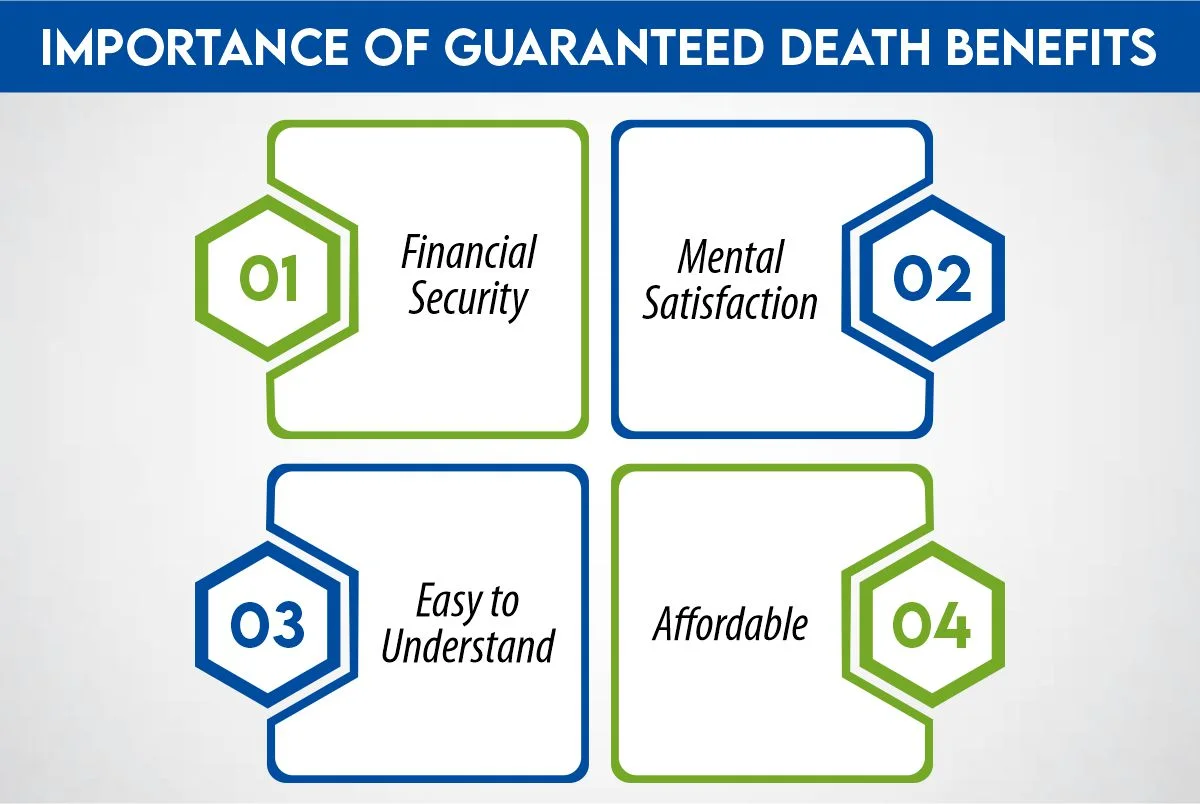

Why Are Guaranteed Death Benefits Important for Life Insurance?

These death benefits are important for life insurance for several reasons:

- Financial Security: The death benefit provides financial security to your loved ones so that they can pay for expenses such as funeral costs, outstanding debts, and living expenses.

- Mental Satisfaction: You and your loved ones can both experience peace of mind by knowing that they will be taken care of financially.

- Easy to Understand: These death benefits are a straightforward and simple feature of life insurance, making it easy for policyholders to understand and take advantage of.

- Affordable: Because guaranteed death benefits do not require a medical exam. They are often more affordable than other types of life insurance.

Who Should Consider a Life Insurance Plan with Guaranteed Death Benefit?

A life insurance plan with a guaranteed death benefit can be beneficial for various individuals based on their financial goals, family situation, and future plans. Here’s who might consider such a plan:

Parents and Breadwinners

Individuals who have dependents relying on their income should consider a policy with a guaranteed death benefit. It ensures financial stability for their loved ones in the event of their untimely death, covering expenses like mortgage payments, outstanding debts, and future financial needs.

Estate Planning

Those with substantial assets or estates might use life insurance as a part of their estate planning. The death benefit can provide liquidity to cover estate taxes and other expenses, preventing the need to sell assets hastily.

Business Owners

Business owners often opt for life insurance with a guaranteed death benefit to protect their businesses. It can provide funds for succession planning, buy-sell agreements, or key person insurance, ensuring the business continues smoothly in case of an owner’s passing.

Individuals Seeking Long-Term Financial Security

Some individuals use life insurance policies with guaranteed death benefits as a means of long-term financial planning or retirement income. Policies with cash value accumulation can serve as a source of tax-deferred savings.

Those Wanting to Leave a Legacy

Individuals who wish to leave a financial legacy for their loved ones or support charitable causes can use the guaranteed death benefit to create a lasting impact beyond their lifetime.

Furthermore, anyone concerned about providing financial protection for their loved ones, ensuring their financial obligations are met, or leveraging life insurance as a financial planning tool might find a life insurance plan with a guaranteed death benefit suitable for their needs.

The Bottom Line

Guaranteed death benefits are a crucial component of Burial insurance providing financial security to your loved ones in the event of your death. Such a life insurance plan is both affordable and straightforward to find because no medical exam is required and the benefit is paid tax–free.

It is important to consider your current expenses and future financial obligations when determining the amount of death benefit. You need to regularly review your policy to ensure that it continues to meet your needs. Investing in them can give your loved ones financial security and peace of mind.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.