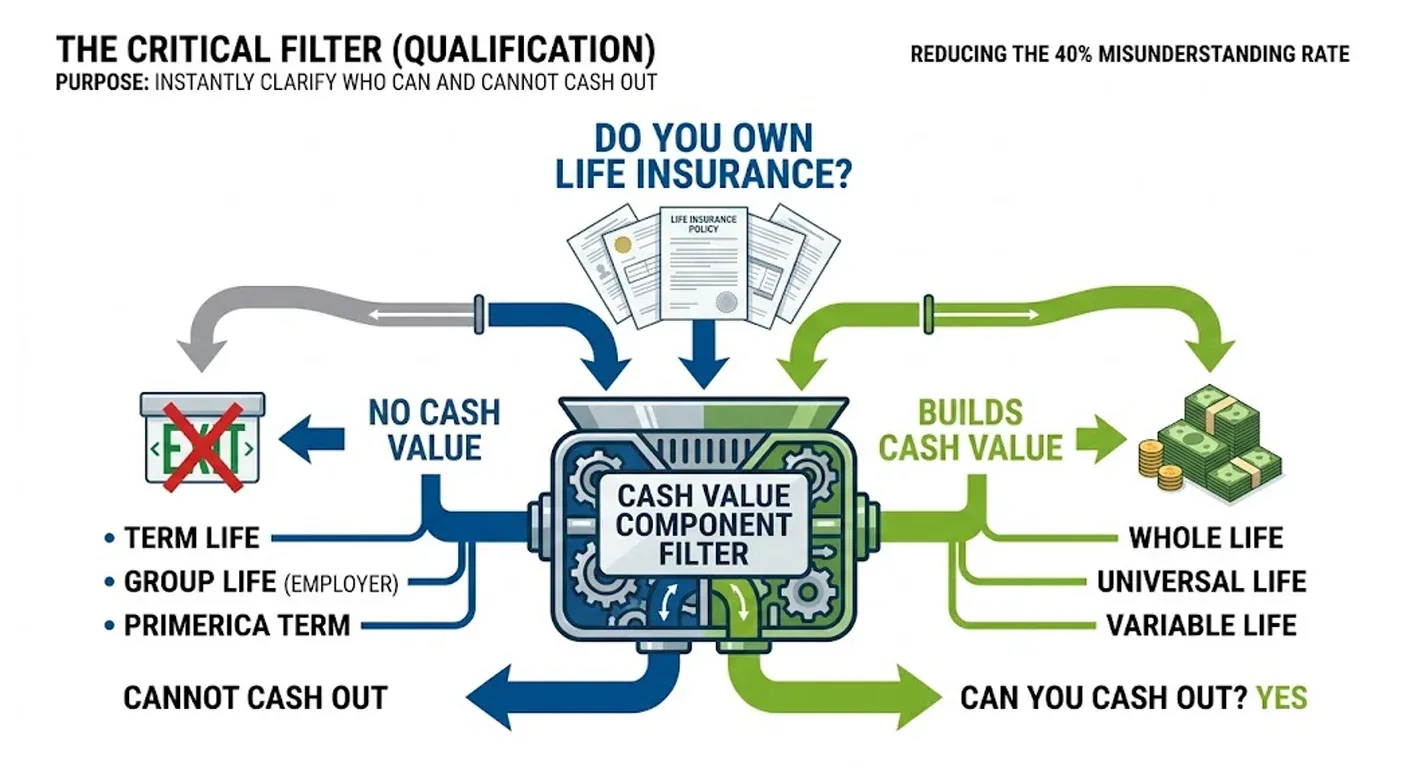

Yes, but only if your policy has built up cash value. That means whole life and universal life policies qualify. Term life policies do not have a cash value component, so you cannot cash them out.

This single distinction trips thousands of policyholders every year. If you have a term policy and someone told you that you can cash out, that information is wrong and acting on it could leave you uninsured with nothing to show for it.

According to LIMRA’s 2025 insurance barometer study, over 40% of Americans misunderstand what type of life insurance they actually hold. Check your policy documents or call your insurance company before making any financial decision.

Term vs. Whole Life: Which One Can You Actually Cash Out?

The table below shows the confusion.

Policy Type | Has Cash Value? | Can You Cash Out? | What You Get |

No | No | $0 — coverage ends at term | |

Yes | Yes | Cash surrender value minus fees | |

Yes | Yes | Accumulated cash value minus surrender charges | |

Yes | Yes (market-dependent) | Cash value tied to investment performance | |

Group Life (employer) | Rarely | Almost Never | Typically no cash value |

Term life is the most purchased policy type in the United States and this plan offers zero cash out value. If you have time, your only exit is letting it lapse or converting into a permanent policy if your insurance company allows it.

How to Cash Out a Whole Life Insurance Policy (Step by Step)

Cashing out a whole life insurance policy is straightforward, but the financial consequences are permanent. Here is how the process works.

Contact your insurer

Call or make and request for your current cash surrender value. This is the amount you will actually receive after surrender charges are deducted.

Request a surrender form

Your insurance company will send you a policy surrender or cancellation form. Fill it out completely because errors delayed the process.

Submit the form and your policy documents

Most of the insurance companies process this within 7 to 14 business days.

Receive your payout

Typically sent by check or direct deposit. This terminates your coverage permanently.

The important thing to remember is, once you surrender, your beneficiaries lose all death benefit protection. There is no undo button.

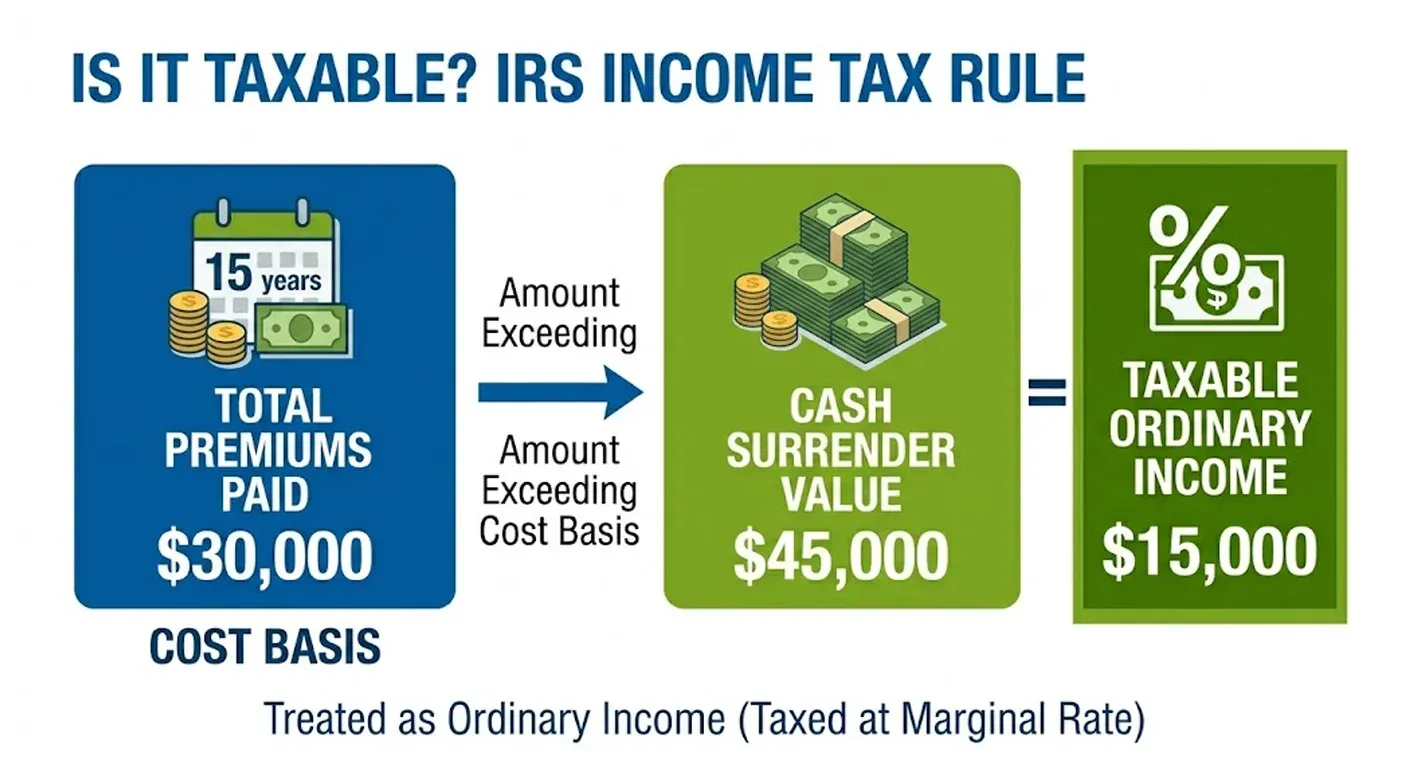

Is Cashing Out a Life Insurance Policy Taxable?

This is where most people get blindsided. Yes, cashing out a life insurance policy can be taxable, and the IRS has clear rules on this.

The rule is

You pay income tax on the amount that exceeds your cost basis that is the total premium you have paid into the policy over time.

For example

- You paid $30,000 in premium over 15 years

- Your cash surrender value is $45,000

- You owe ordinary income income tax on $15,000.

The tax on cash out of a life insurance policy is treated as ordinary income, not the capital gains. That means it is taxed at your marginal rate, which in 2026 could be anywhere from 10% to 37% depending on your total income for the year.

Per IRS publication 525, proceeds from surrendering a life insurance policy are included in gross income to the extent they exceed your investment in the contract.

Can You Cash Out a Primerica or Group Life Insurance Policy?

Primerica policies are primarily term life products. Because they are term policies, they do not accumulate cash value. You cannot cash out a Primerica life insurance policy in the traditional sense. Primerica’s model is buy term and invests the difference that is built around keeping the insurance and investment account separate.

If you are a Primerica policy holder thinking how to access money, your options are limited to canceling for no cash return, not checking if you have any separated investments or saving accounts through them.

Group life insurance offered through an employer almost never has cash value. These are typically term based group contracts with the employer holding the master policy. You have coverage but no ownership mistakes in the cash value because there is none. You cannot cash out a group life insurance policy under standard plans.

Should You Cash Out Your Life Insurance Policy?

For most people, cashing out early is the wrong move but the right answer depends entirely on your situation.

When cashing out might make sense

- Your policy has very little death benefit relative to its cash value

- You have no dependents who need the death benefit

- You are in low income tax bracket and the tax hits is minimal

- You urgently need funds and have exhausted all other options

When it almost never makes sense

- You still have dependents relying on the death benefit

- You are in high tax bracket, the tax hit will be significant

- You can qualify for a policy loan instead

- You are within the surrender charge period of the first 5 to 10 years.

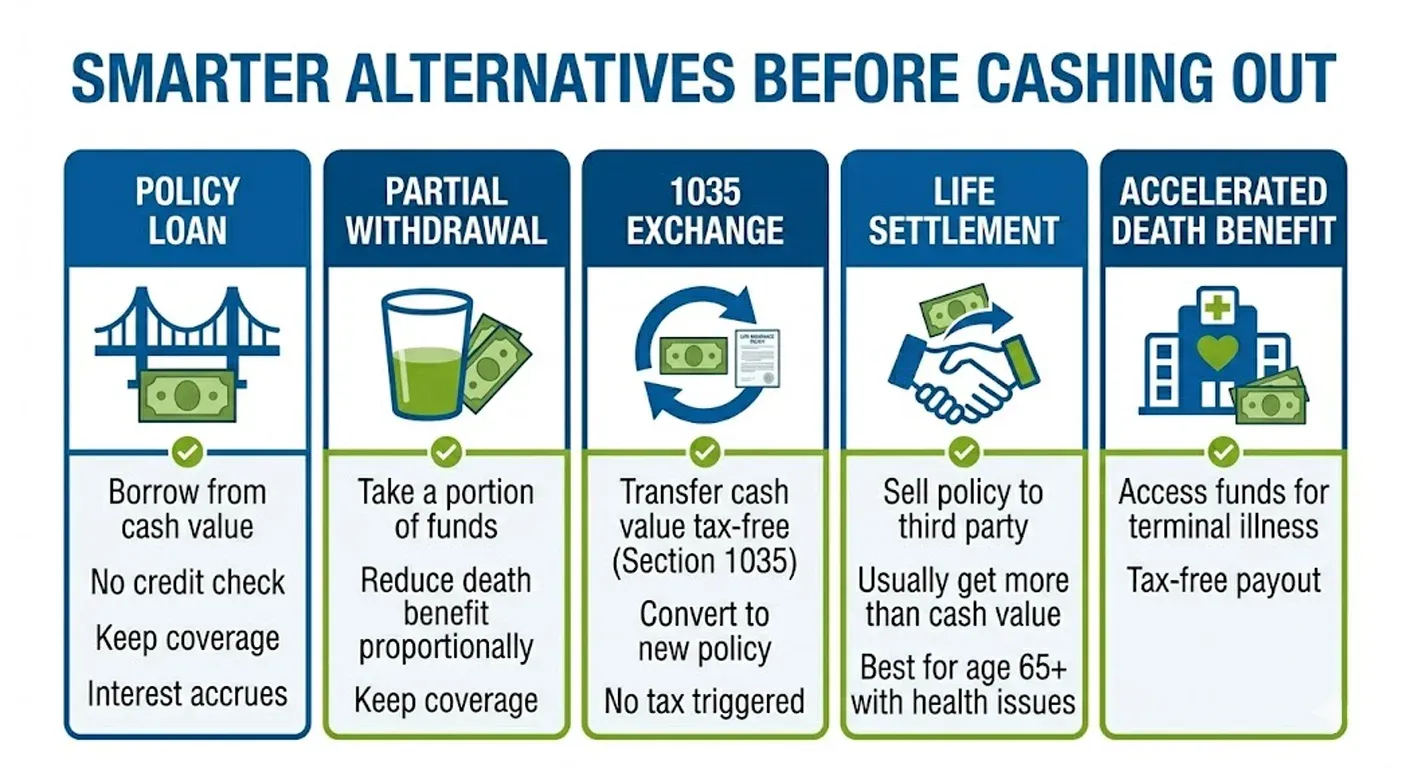

Smarter Alternatives Before You Cash Out

Before you pull the trigger, these options protect more of your money.

Policy Loan

Borrow from your policies cash value. No credit check, no tax consequences as long as the policy stays active. Interest occurs, but you repay on your own terms.

Partial Surrender / Partial Withdrawal

Some whole life policies allow you to withdraw a portion of the cash value without fully surrendering. You reduce the death benefit proportionally but keep coverage in place.

1035 Exchange

Transfer the cash value of your life insurance policy into a new tax-free under IRS section 1035. No tax triggered. No surrender of coverage. You can convert rather than cash out.

Accelerated Death Benefit

If you have a terminal illness diagnosis, the most modern policies allow you to access a portion of the death benefit early that is completely tax-free.

Life Settlement

Sell policy to a third-party company for more than the cash surrender value but less than the death benefit. Typically available to policyholders 65 and older with serious health conditions.

The Bottom Line: Think Twice Before You Act

Cashing out a life insurance policy is a one way door. The death benefit is gone, your coverage is terminated and depending on your gains, you may owe a significant tax bill.

If your policy has cash value and you need liquidity, a policy loan almost always costs you less than a full surrender that is financially and in terms of coverage lost.

Before you make any decision, get your current cash interval in writing, calculate the exact tax liability with the tax advisor and the alternatives above.

Ready to review your life insurance options with a professional?

At M-life Insurance, our licensed advisor will help you to understand exactly what your policy is worth and without cashing out is really the right move for your situation. No pressure, no sales scripts. Just a clear picture of your option so you can decide with confidence.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.