You are about to buy a life insurance policy or maybe you already have one and the number staring at you says $500,000. That sounds like a lot. But here is the question most people never think to ask

Is that the amount your family actually gets when you’re gone?

Not always. And that confusion between what a policy appears to offer and what it actually pays is one of the most expensive mistakes families make. Getting this wrong does not mean picking the wrong number. It can mean your spouse cannot pay off the mortgage. Your kids’ college fee funds disappear. Everything you worked for, undone by a term you never fully understood.

Let’s fix that right now in an easy and simple way so that you can understand.

What Is the Face Value of a Life Insurance Policy?

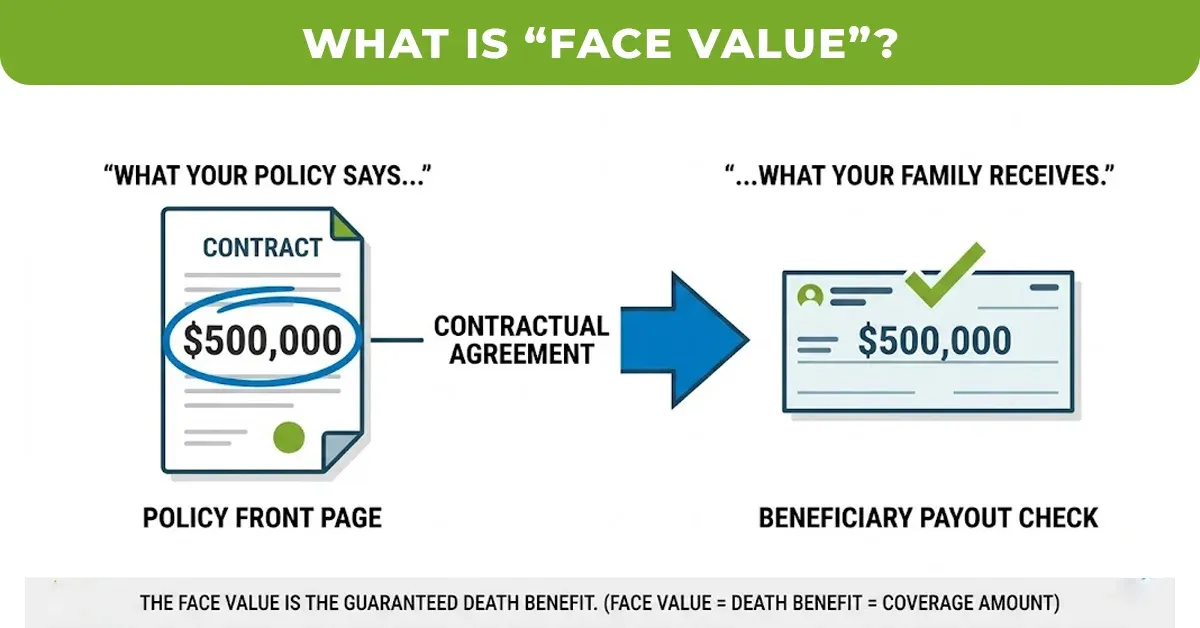

The face value of a life insurance policy is the base death benefit, the fixed dollar amount your beneficiaries will receive when you die, as stated on the front page of your policy contract.

It is also called the policy face amount, death benefit or coverage amount. If your policy says $500,000, that is the face value. When you pass away and your beneficiaries file a claim, that is the check the insurance company is contractually obligated to issue, assuming the policy is in force.

The face value is set at the time you purchase the policy. It does not grow on its own. It does not fluctuate with the market. It is the guaranteed payout your family is counting on.

In short the face value is equal to the dollar amount printed on your policy is equal to what your family gets when you die.

Face Value vs. Cash Value — They Are Not the Same Thing

This is where most people get seriously confused, and where wrong decisions get made.

| Feature | Face Value | Cash Value |

| What it is | Death benefit paid to beneficiaries | Living savings component inside permanent policies |

| Who receives it | Your beneficiaries (after you die) | You (while you’re alive) |

| Available in | Term & permanent life insurance | Permanent life insurance only |

| Grows over time? | No (unless specified) | Yes — slowly, over years |

| Can you access it early? | No | Yes — through loans or withdrawals |

Face Value vs. Cash Value: A Comparison

Term life insurance

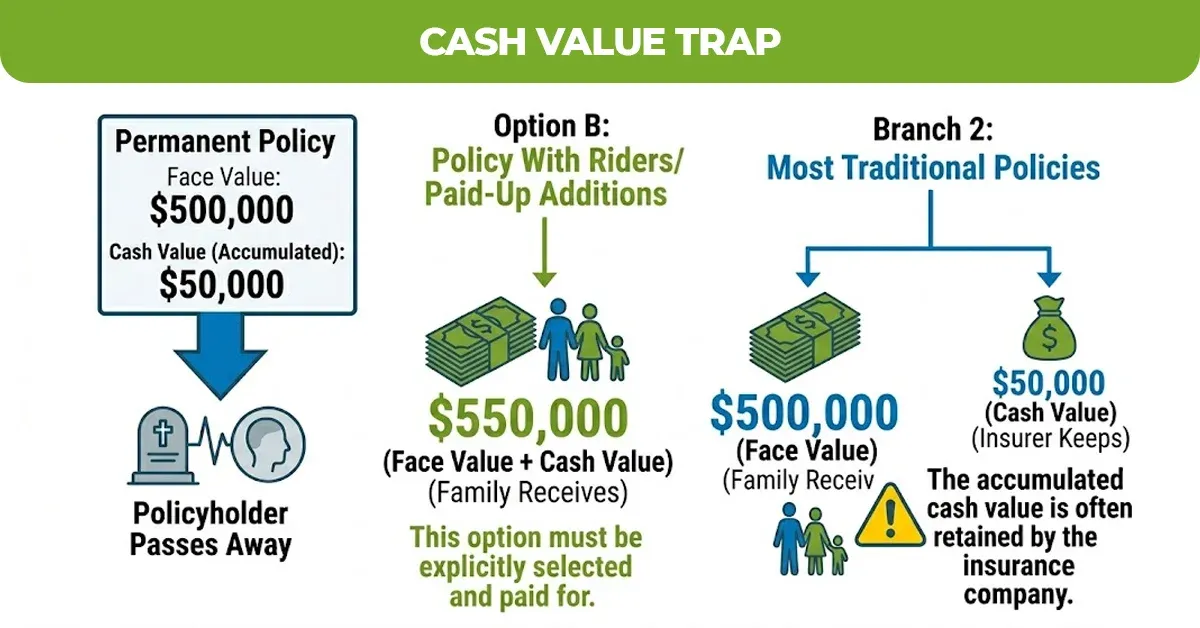

Term life insurance has a face value at zero cash value. It is pure protection like pays the premium, and get the death benefit, nothing else.

Whole Life or Universal Life Insurance

Whole life for universal life carries both. The cash value is a separate savings account that builds overtime inside the policy. But here is the most agent glosses over. In many traditional whole life policies, your beneficiaries receive the face value not the face value plus the cash value. The insurance company may keep the accumulated cash value up upon your death.

Always confirm with your insurance company whether your policy pays face value only, or face value plus accumulated cash value. This single question can mean a difference of tens of thousands of dollars.

How Is the Face Value of a Policy Determined?

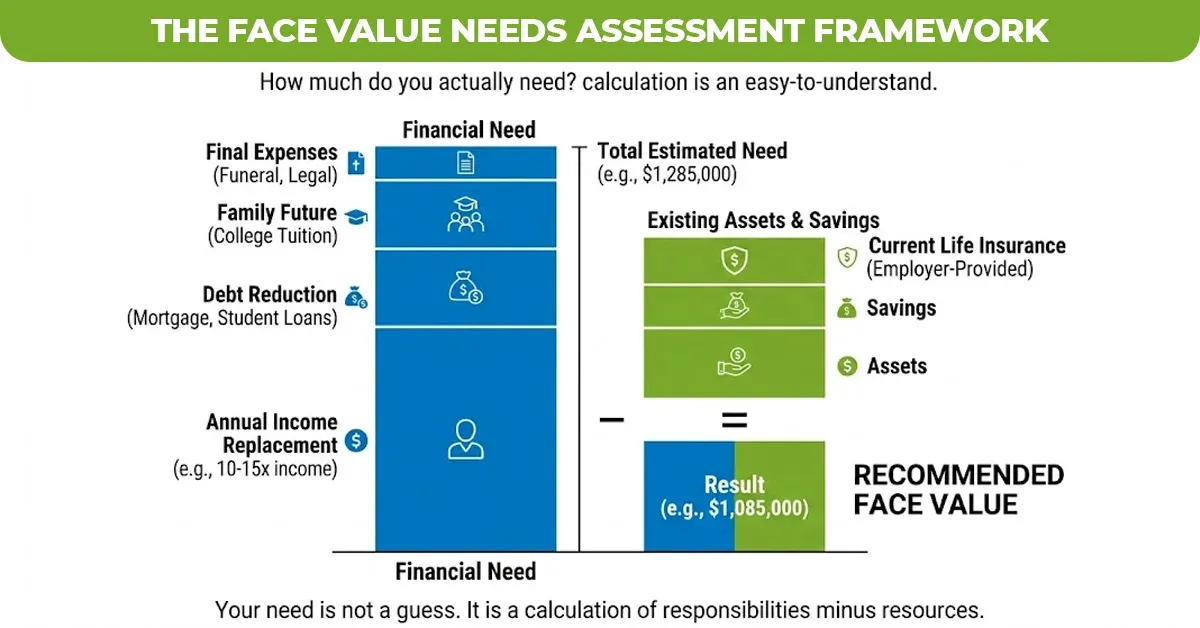

You can choose your face value when you apply. But what you should choose is shaped by several real factors.

- Your income and debt obligation, most financial advisor recommend coverage of 10 to 15x your annual income

- Your dependents, spouses, children, aging parents who rely on you

- Outstanding liabilities like mortgage, student loans and car payments.

- Future financial goals, like college funding, retirement income replacement

- Your age and health, these determine your premium for the chosen face value.

The 2026 Coverage Reality Check

According to LIMRA’s 2025 Insurance Barometer Study 44% of Americans say their household would face financial hardship within six months if the primary earner died. The leading cause? Under insurance that is often the result of choosing a face value based on affordability alone, not need.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.