You searched for instant life insurance because waiting feels like gambling. Every week without coverage is a week your family is unprotected. That is the real danger like most people who click the first result, rush through a quote and end up with the wrong policy, one that pays out less than expected or the one that has a two year waiting period buried in the fine print.

This guide cuts you through that. You will know exactly what instant life insurance is, who it is for, what it actually cost in 2026 and where to get a real policy, not just a quote.

What Is Instant Life Insurance, and How Fast Is “Instant”?

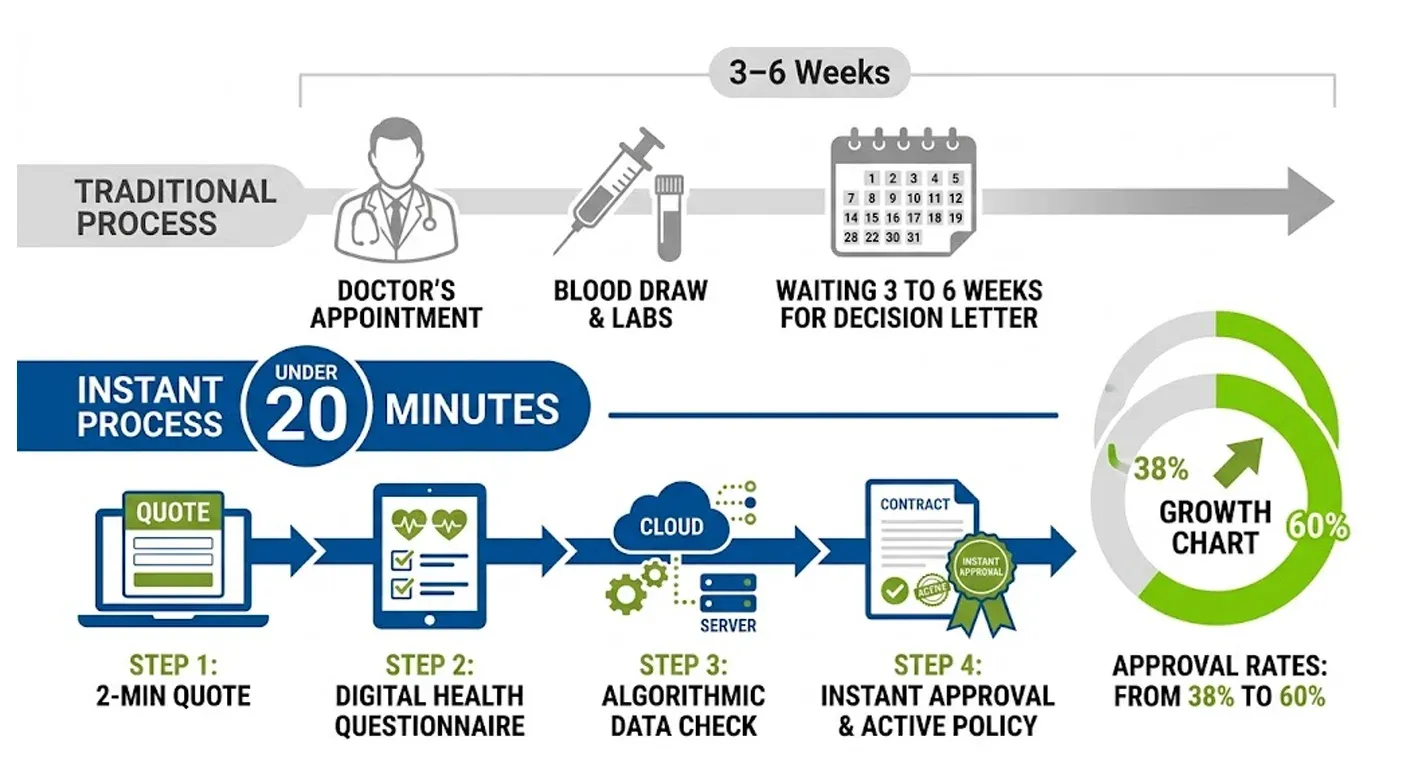

Instant life insurance means you apply online and receive a coverage decision or a full policy within minutes, sometimes under 20. No doctor’s appointment, no blood draw, no waiting 3 to 6 weeks for a letter in the email.

According to LIMRA’s 2025 Insurance Barometer Study, 44% of Americans say they would purchase life insurance if the process were simpler and faster. The industry responded. By 2026 most major insurance companies now offer some form of instant issue life insurance or accelerated underwriting that will deliver a binding decision in real time.

There are two main types

Instant issue life insurance

No medical exam is required in this plan. The insurance company uses data algorithm to make an underwriting decision instantly

Accelerated underwriting

It may use a short health questionnaire. The plan is faster than the traditional underwriting, still there is no exam for most healthy applicants.

The coverage you can get this way from $25,000 to $3 million depending on the carrier and your age .

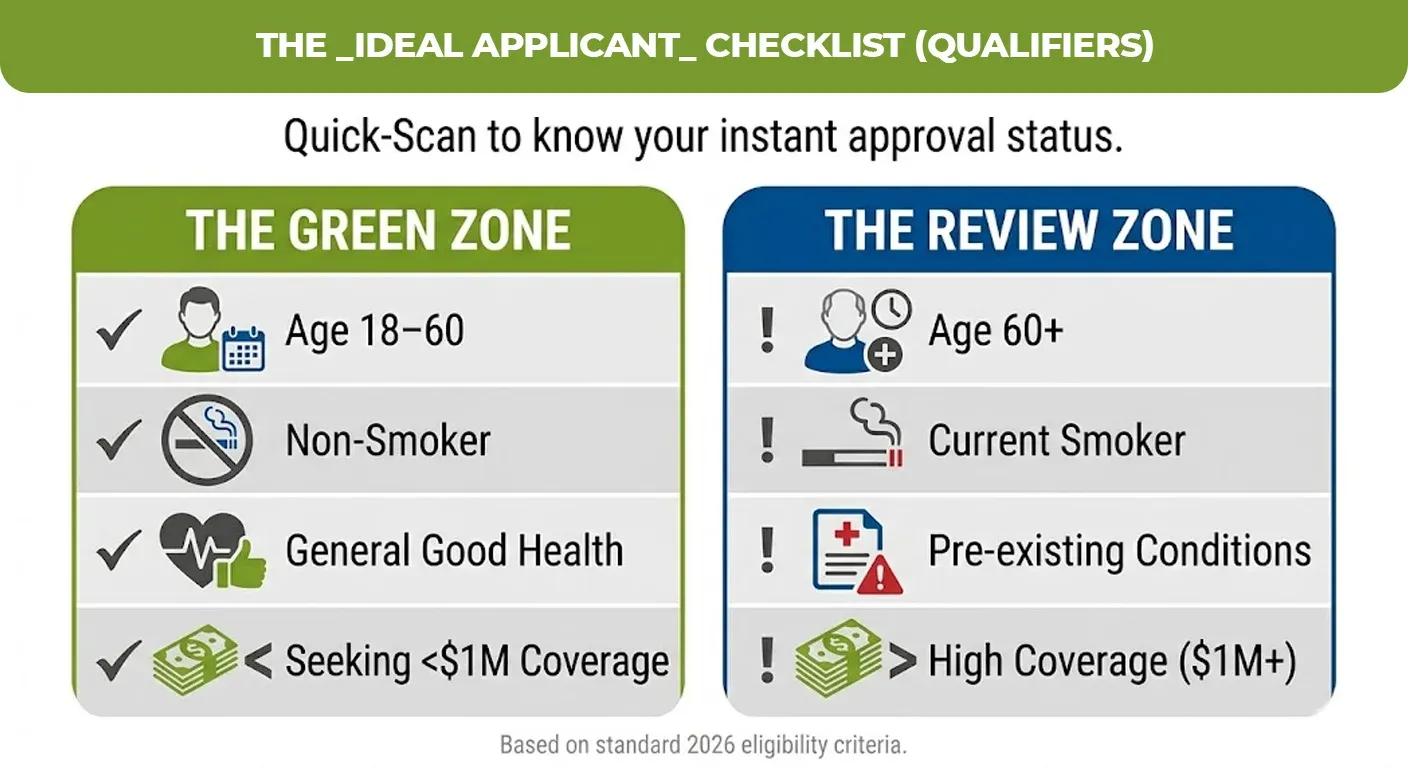

Who Actually Qualifies for Instant Approval Life Insurance?

Instant approval life insurance is not for everyone knowing this upfront saves you wasted time.

You are likely to qualify if you are

- Between 18 and 60 years old

- And generally good health with no major chronic conditions

- Non-smoker, or a recent quitter

- Any serious pre-existing conditions

You can face a more detailed review if you are

- Over 60

- Looking for more than $1 million in coverage

- Applying as a smoker

The American Council of life insurance ACLI reports that the companies are using algorithmic underwriting and now approve over 60% of applicants without any additional medical documentation. That number is up from 38% in 2022.

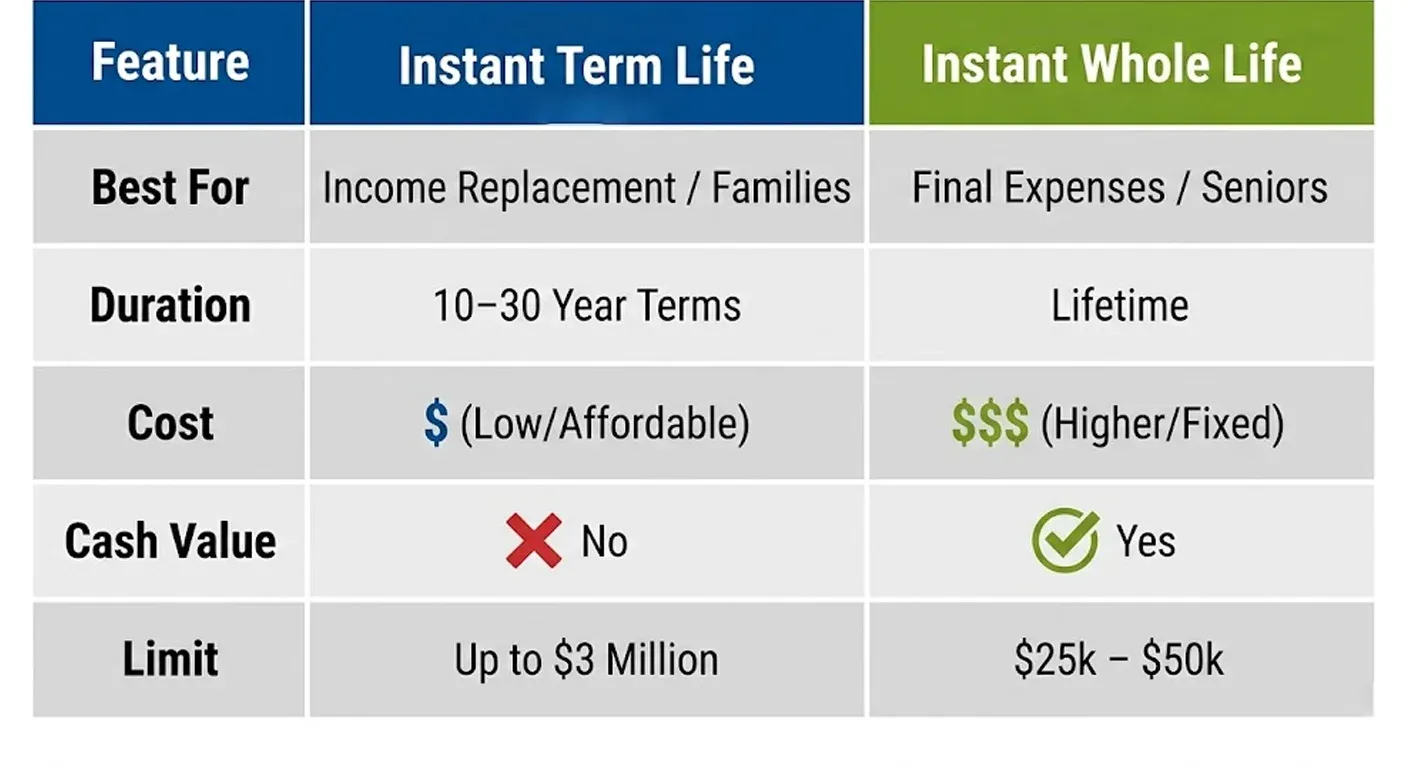

Instant Term Life Insurance vs. Instant Issue Whole Life: Which One Fits You?

Choosing the wrong type is where most people lose money. Here is a clear breakdown

| Feature | Instant Term Life Insurance | Instant Issue Whole Life |

| Coverage duration | 10, 15, 20, or 30 years | Lifetime |

| Monthly premium (sample: $500K, age 35) | $18–$35/month | $200–$450/month |

| Cash value accumulation | No | Yes |

| Best for | Income replacement, young families | Final expenses, estate planning |

| Coverage limit (typical) | Up to $3 million | $25,000–$50,000 |

| Medical exam required | No (for most carriers) | No |

Instant term life insurance is the better fit for the majority of working age adults who want maximum coverage at the lowest cost. You are not paying for cash value you may never use.

Instant issue life insurance makes sense for seniors or for those with serious health issues who need guaranteed, for funeral expenses and small estate needs.

How to Get Instant Life Insurance Quotes Online Without Getting Burned

Getting an instant life insurance quote online takes two minutes. Getting the right quote takes slightly more thought. Here is what to watch

- Use multi carrier quote tool

- Integrated health information

- Read the fine print on graded death benefits

- Confirm the policies from a financial carrier.

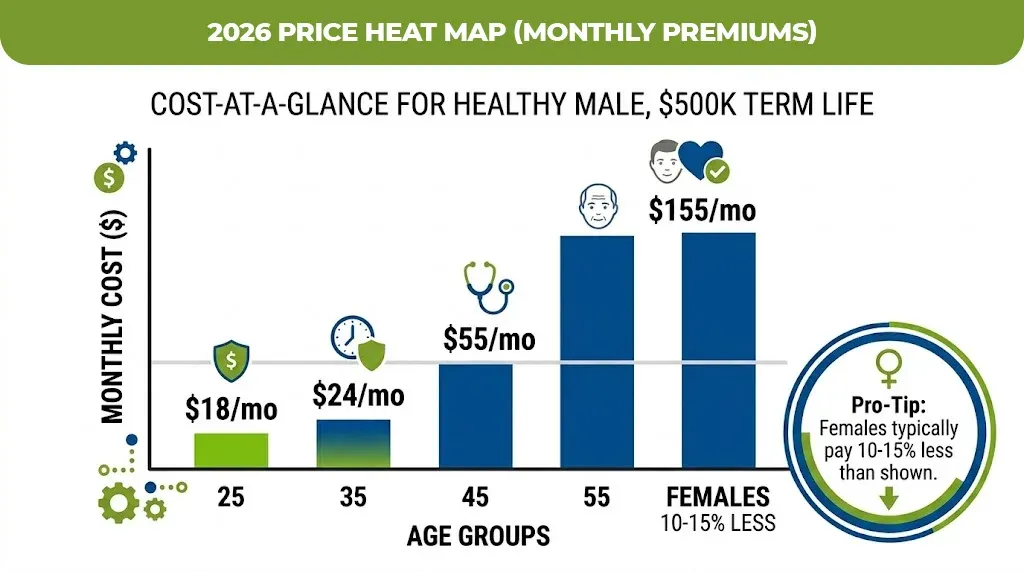

2026 Cost Comparison: Instant Life Insurance Quotes by Age and Coverage

These are representative monthly premiums for a healthy, non smoking male applying for a 20 year term life insurance policy

| Age | $250,000 Coverage | $500,000 Coverage | $1,000,000 Coverage |

| 25 | $11–$16/mo | $18–$28/mo | $30–$50/mo |

| 35 | $14–$22/mo | $24–$38/mo | $43–$68/mo |

| 45 | $30–$48/mo | $55–$88/mo | $100–$165/mo |

| 55 | $80–$120/mo | $155–$230/mo | $290–$420/mo |

Female applicants typically pay 10 to 15% less due to longer average life expectancy. Smokers paid 2 to 3x more.

What the Application Process Actually Looks Like (Step by Step)

Most of the insurance companies offering instant approval life insurance follows near identical process

- Enter your basic information like age, gender, state, decide coverage amount and term length

- Make sure to answer the health question

- Consent to data checks

- Receive a real time decision

- Signed digitally and pay for premium

This entire process from landing on the quote page to holding an active policy, routinely takes under 20 minutes for qualifying applicants.

Ready to Find the Right Policy? Start Here

If you have made this far, you are already more informed than most people who buy instant life insurance here. You know what type you need, what a fair price looks like and what questions to ask.

The next step is a quote, one that compares the real carriers, real premiums and real terms.

Explore M-life Insurance instant life insurance quotes online

The team is packed by a customer service operation bill specifically for potential insurance shoppers, real agents, fast response time and zero pressure to upsell. You get your clear answers, not a sales script.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.