You are signing loan documents. The lender offers you payment protection or “credit life insurance.” It sounds responsible. You check the box and move on.

That might be the most expensive checkbox you ever click without reading the fine print.

Millions of borrowers in 2026 are paying the premiums for a policy that protects the lender, not their family. Before you sign, or before you cancel, here is exactly what you need to know.

What Is Credit Life Insurance Meaning?

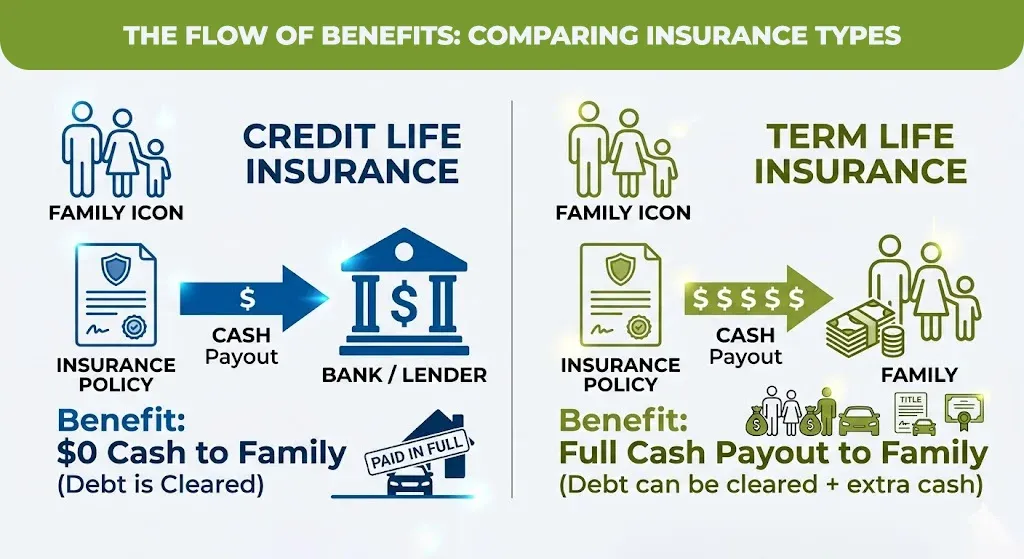

Credit life insurance is a policy that pays off your outstanding loan balance if you die before the debt is fully repaid. The beneficiary is the lender, not your spouse, also not your children.

The credit life insurance definition sounds straightforward like you borrow money, then you buy a policy, and the loan gets cleared if you pass away. But the important detail most people miss is who actually gets the benefit from this.

Your family will not receive a cash payout. The bank does. Your family just gets a debt-free estate, which is then valuable, but not the same as life insurance that pays your mortgage and covers living expenses.

Let’s take the real world example:

Sarah takes out a $30,000 auto loan and adds credit life insurance at $45/month. She died in year two. The remaining $22,000 balance is paid to the lender. Her husband gets no cash, just a cleared car title.

Credit Life Insurance vs. Traditional Life Insurance: The Honest Comparison

This is where most people make the wrong decision. Here is a side by side breakdown:

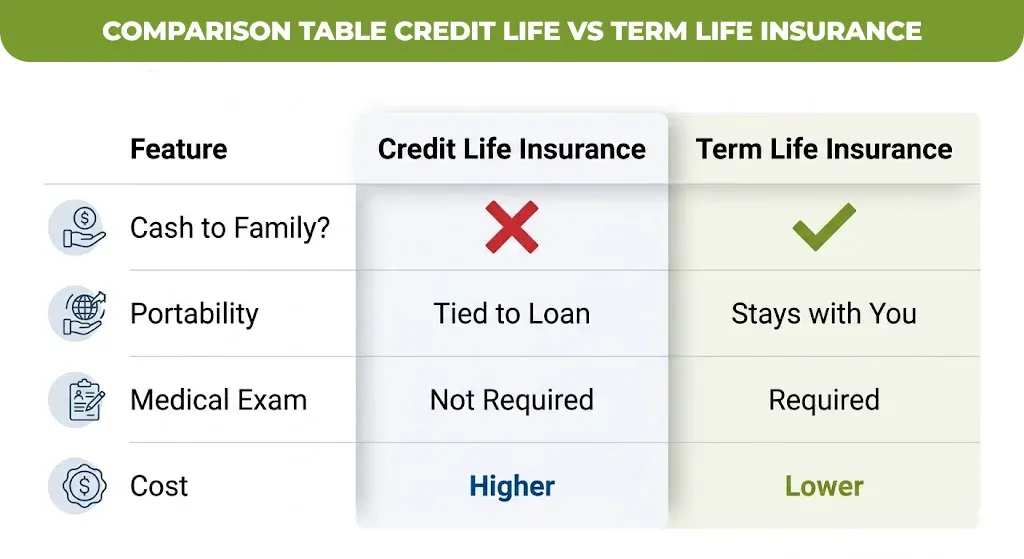

| Feature | Credit Life Insurance | Term Life Insurance |

| Beneficiary | The lender | Your family |

| Payout | Loan balance only | Fixed death benefit |

| Coverage decreases over time? | Yes — as loan balance drops | No — fixed amount |

| Medical exam required? | Usually no | Often yes |

| Average monthly cost (2026) | $30–$80 per $100K | $15–$35 per $100K |

| Portability | Tied to specific loan | Stays with you |

| Does the family receive cash? | No | Yes |

Term life insurance typically delivers twice the protection at half the cost. According to the Consumer Financial Protection Bureau (CFPB), credit insurance products are among the least cost-effective insurance products available to consumers.

Where Credit Life Insurance Is Commonly Sold And Why It Matters

Credit life insurance shows up in three major lending contexts and each one works a bit differently.

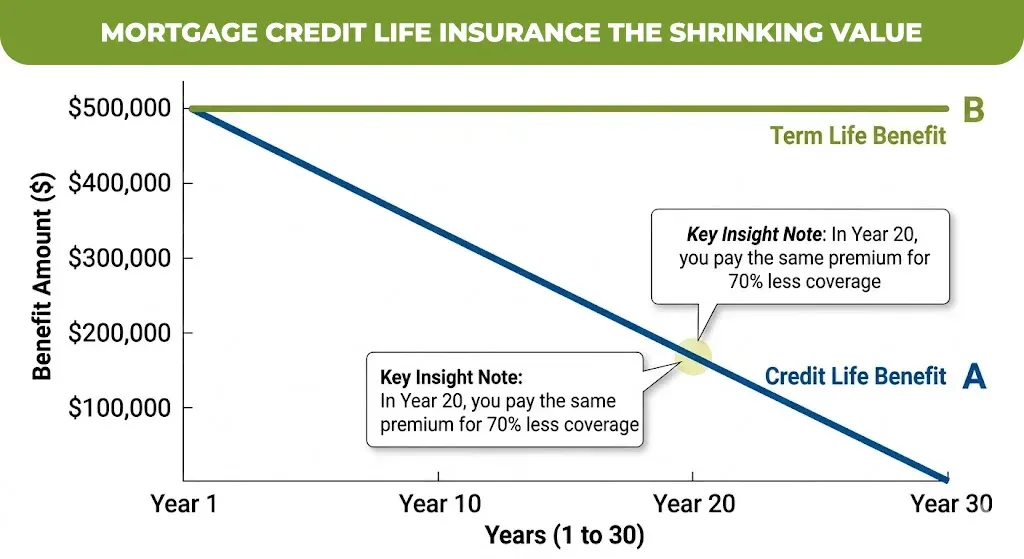

Mortgage Credit Life Insurance

Mortgage credit life insurance pays off your home loan if you die. The coverage amount shrinks every year alongside your mortgage balance. A $400,000 policy in year one might only be worth $310,000 by year five but your premiums stay the same or even increase.

Compare that to a 30-year term life policy at a flat $400,000. Your family keeps the full benefit, can pay off the mortgage and have money left over.

Credit Life Insurance for Auto Loans

Auto loan terms are shorter that is typically 48–72 months, so the exposure window is very small. Credit life insurance on a car loan is less costly overall, but still often overpriced relative to term coverage.

Credit Union Life Insurance

Credit unions sometimes bundle life insurance products, including the credit life at lower rates as compared to the traditional lenders. According to NCUA 2025 data, the credit union insurance products tend to have lower embedded profit margins than bank-sold equivalents. If you are getting credit life, a credit union is often a better source.

How Much Does Credit Life Insurance Actually Cost?

Credit life insurance rates in 2026 vary by lender, loan type, and your age but here is a realistic cost table

| Loan Type | Loan Amount | Approx. Monthly Premium | Annual Cost |

| Auto loan | $25,000 | $18–$35 | $216–$420 |

| Personal loan | $15,000 | $12–$22 | $144–$264 |

| Mortgage | $300,000 | $60–$120 | $720–$1,440 |

| Mortgage | $500,000 | $90–$175 | $1,080–$2,100 |

These are estimates based on industry-average rates. Your actual credit life insurance cost depends on your lender’s pricing, your age, and the loan term. Use a credit life insurance calculator most lenders provide one to get an exact quote before agreeing.

Who Is the Beneficiary Under a Credit Life Insurance Policy?

The lender is always the beneficiary, not your family. This is the most misunderstood feature of a credit life insurance policy.

This is not inherently wrong. Clearing a debt can protect your family from collectors and preserve assets like your car, your home. But it’s a fundamentally different product than standard life insurance.

If your main goal is to protect your family financially, then a credit life insurance policy alone is not enough. It handles one debt. It doesn’t cover income replacement, childcare costs, or other debts not listed in the policy.

Group Credit Life Insurance: A Better Option for Employees?

Group credit life insurance is offered through employers or associations and is typically more affordable than individually purchased policies.

It works similarly to group health insurance, the risk is spread across so many people, so the premiums are lower. If your employer or credit union offers a group credit life insurance option, it’s worth comparing against individual policies before signing with a lender.

The CFPB recommends comparing at least two insurance quotes before accepting any creditor-offered insurance product.

Is Credit Life Insurance Worth It in 2026?

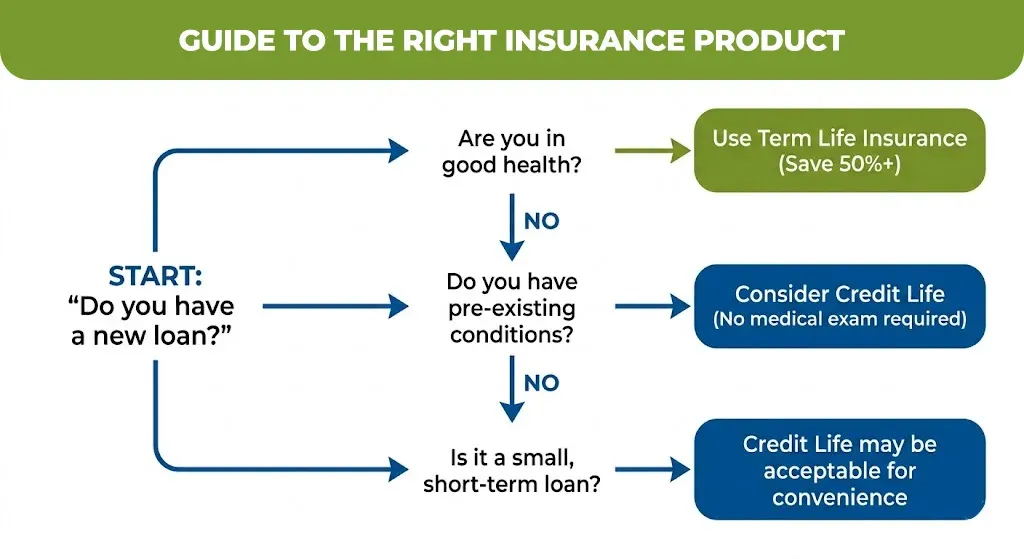

For most borrowers with good health, no. For those who can not qualify for standard life insurance, possibly yes.

Here is the decision framework

- If you are healthy then make sure to get a term life policy. It is cheaper, more flexible, and your family gets the cash, not just a zeroed-out loan.

- If you have health conditions that disqualify you from term life then credit life insurance requires no medical exam and offers guaranteed acceptance. It is not ideal, but it’s coverage.

- If your loan is small and short-term: The math may work. A 24-month $8,000 personal loan has limited exposure. The premium cost may be acceptable for peace of mind.

- If you’re taking out a large mortgage then avoid credit life. A dedicated mortgage credit life insurance or standard term policy almost always wins on value.

According to LIMRA’s 2025 Insurance Barometer Study, 44% of U.S. households say they need more life insurance coverage than they currently carry, and many are over relying on creditor-linked products that don’t fill that gap.

How to Evaluate a Credit Life Insurance Policy Before You Sign

Before accepting any credit life insurance companies’ offer at the loan desk, ask these five questions:

- Is this coverage required? In most U.S. states, it is not mandatory. Lenders cannot deny your loan for declining it.

- Can I cancel it later? Most policies allow cancellation with a prorated refund.

- What exactly does it cover? Confirm if it’s death only, or also disability and involuntary unemployment.

- Is the premium built into the loan? If so, you’re paying interest on your insurance premium.

- What does an equivalent term life policy cost? Get a quote before you sit at the closing table.

The Right Coverage Starts With the Right Guidance

Credit life insurance isn’t a scam, but it is often oversold to people who would be better served by a proper life insurance policy. The difference can mean tens of thousands of dollars over a loan’s lifetime.

At M-Life Insurance, our team helps you compare options clearly, without pressure. Whether you need mortgage protection, auto loan coverage, or a full life insurance review, we’re here to make sure you’re covered the right way, not just the convenient way.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.