There are a lot of people who are shopping for whole life insurance and then they end up quoted on the universal life policy instead or the other way around. The agent used permanent and whole life insurance terms like they meant the same thing, the buyer sign and then after a few years the premium jumped out and the cash value did not grow the way they were expecting.

That confusion is understandable. Whole life insurance is a type of permanent life insurance policy but not permanent policies a whole life policy. Get that distinction wrong and you could end up with a policy whose cost or guarantees don’t matter what you actually wanted.

Is Permanent Life Insurance the Same as Whole Life Insurance?

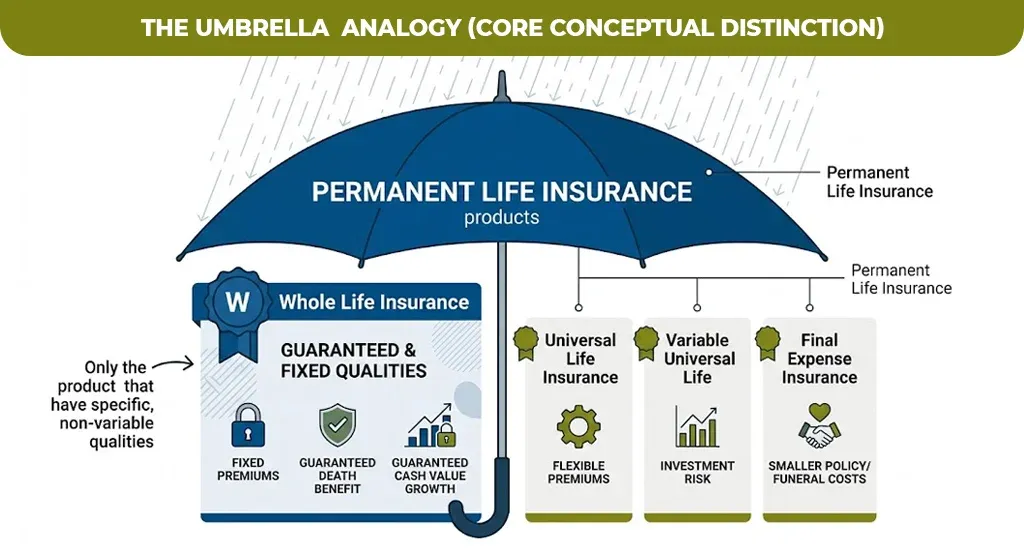

No, the permanent life insurance is the broad category and the policy that will cover you for your entire life as long as you are paying your premiums. Whole life insurance is the one specific product inside that category. It comes with the fixed premiums, guarantee death benefit and guarantee cash value growth.

Universal life, valuable universal life, and final expense insurance are also the permanent life insurance plans but they were differently from whole life insurance. So permanent life insurance vs whole life insurance, is not really a battle between two rivals, it is a comparison between a category and one option inside that category.

What Is Permanent Life Insurance and How Does It Work?

The permanent life insurance provides lifelong coverage, it also build cash value on default basis and it never expires as long as you are keeping your monthly premium. That is the opposite of term life insurance, which only covers you for a number of years and pays nothing if you outlive that term.

Part of every premium you pay goes towards the death benefit, and the part goes towards the policy is cash value. You can generally borrow against that cash value or you can withdraw from me whenever you want while you are alive. Though to reduces the death benefit if the loan is not repaid.

Types of Permanent Life Insurance

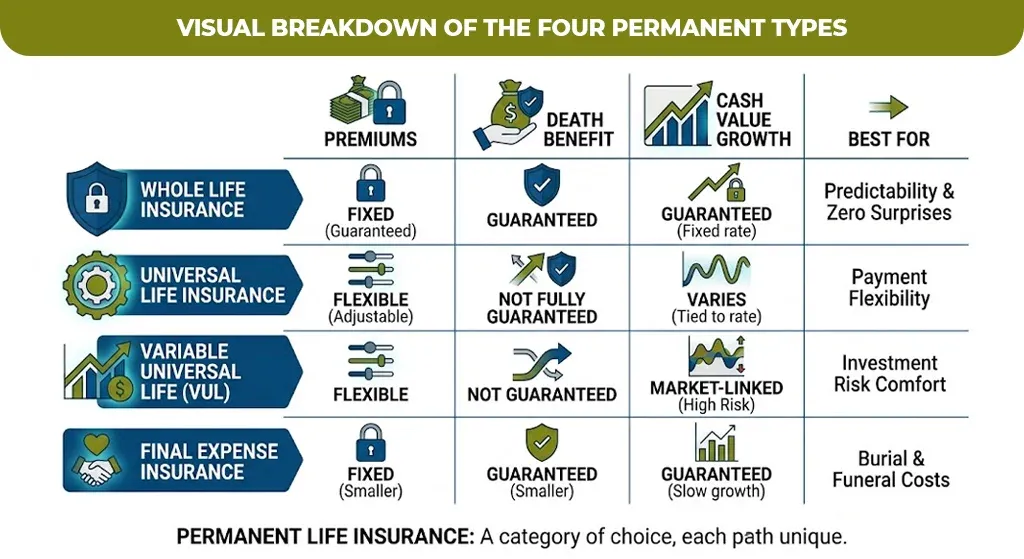

Permanent life insurance is not one product, it is a family of four main types and the differences between them matters a lot more than the most people realize before they buy.

| Type | Premiums | Death benefit | Cash value growth | Best for |

| Whole life | Fixed for life | Guaranteed, fixed | Guaranteed, fixed rate | People who want zero surprises |

| Universal life | Flexible, adjustable | Adjustable, not fully guaranteed | Tied to a minimum guaranteed rate, can vary | People who want payment flexibility |

| Variable universal life | Flexible | Not guaranteed | Invested in market-based subaccounts | People comfortable with investment risk |

| Final expense (a type of whole life) | Fixed, smaller policy | Guaranteed, smaller ($5,000–$50,000 typical) | Guaranteed, slower growth | People who mainly need funeral/burial coverage |

whole life insurance is the most predictable of four. Universal and variable universal life trade that predictably for flexibility, which sound appealing until an underfunded policy lapse is right when you need it most.

Key Features of Permanent Life Insurance vs Whole Life Insurance

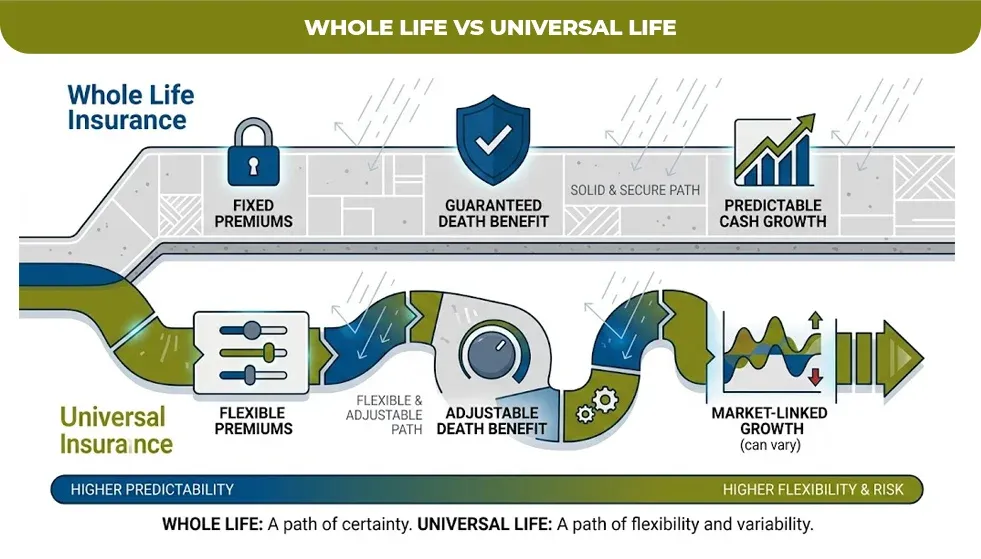

Whole life insurance policy is permanent but not every feature of permanent life insurance shows up the same way once you are inside a specific whole life contract. Here is where they actually diverge.

Premium Structure

All permanent life insurance policies guaranteed coverage for a life, but only the whole life guarantees the premium will never change. Universal life premiums can be adjusted by the policyholder and if funded the insurance company can increase the cost of insurance charges within the policy.

Cash Value Growth

Permanent life insurance properly promises tax Stafford cash value growth but the rate is not fixed across all types. Whole life locks in a guaranteed minimum growth rate set as issue like universal and variable universal lifetime growth to interest rate or market performance. Which means that it can go up or down.

Dividends

Some whole life policies especially those from the mutual insurance companies pay non-guaranteed annual dividend that can be used to buy the additional coverage or reduced the premiums. This feature is specific to participating the whole life policy is not guaranteed across every permanent policy type.

Policy Lapse Risk

Whole life insurance policy with premium paid on time essentially cannot lapse. Life policy scans if the casual drops too low to cover the internal charges. Even if the policyholder believed they were adequately funding it.

Permanent Life Insurance vs Whole Life: Cost Comparison for 2026

Cost is where the category versus product distinction really shows up because the permanent life insurance can cost different depending on which title you choose.

| Age | Whole life ($500K, nonsmoker) | Universal life ($500K, nonsmoker) |

| 25 | $349–$379/month | $182–$210/month |

| 40 | $540–$574/month | $362/month |

| 60 | $1,308–$1,443/month | $765–$930/month |

Data based on 2026 rate averages from MoneyGeek’s life insurance cost analysis. Whole life consistently costs more than universal life at every age because of the growth and premium guarantees built into the contract that you’re paying for certainty, not just coverage.

For comparison, a healthy 40-year-old buying $500,000 of 20-year term life insurance pays around $321 a year, a small fraction of either permanent option, according to NerdWallet’s 2026 average life insurance rates. Term is cheaper because it only has to cover a limited window, not a guaranteed lifetime payout.

Which One Should You Actually Buy?

The Bottom Line

Permanent life insurance is the umbrella. Whole life insurance is one option under it, built for people who want guarantees over flexibility. Before you sign anything, confirm exactly which type of permanent policy you’re being quoted, the word “permanent” alone doesn’t tell you what you’re actually buying.

If you’re trying to figure out which type of permanent coverage actually fits your goals and budget, M-Life Insurance can walk you through real quotes across whole life, universal life, and final expense options so you know exactly what you’re comparing before you commit to a policy.

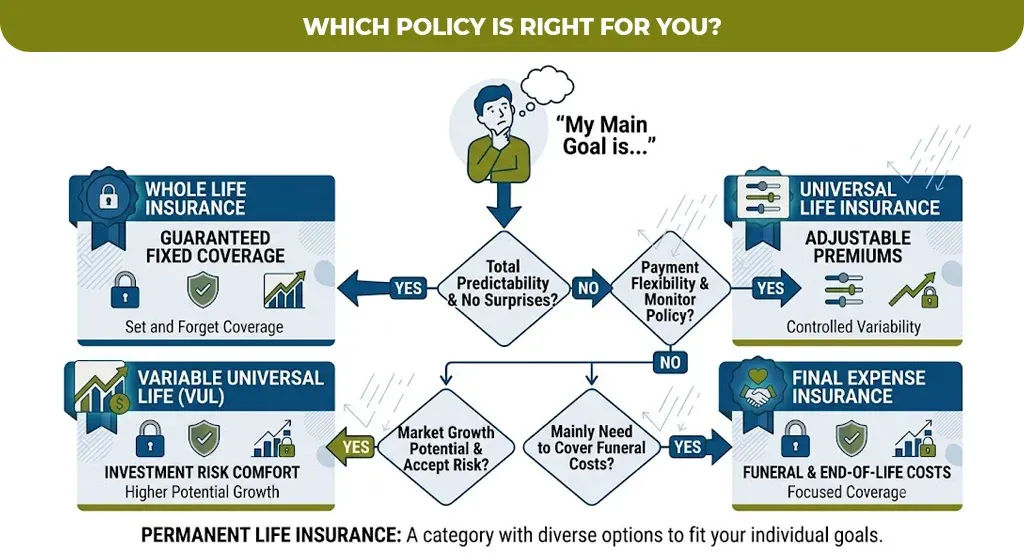

Which One Should You Actually Buy?

Start with what you need the policy to guarantee, not with the word “permanent” on its own.

- Want a fixed premium you’ll never have to think about again, plus guaranteed cash value growth? Whole life insurance is built for exactly that.

- Want flexibility to adjust premiums as your income changes, and you’re comfortable monitoring the policy? Universal life gives you that room, with more responsibility on your end.

- Comfortable with market risk in exchange for higher potential cash value growth? Variable universal life fits, but understand you could also lose value.

- Mainly need coverage for funeral and end-of-life costs, not a large death benefit? Final expense insurance, a smaller whole life policy, is usually the more affordable fit.

The Bottom Line

Permanent life insurance is the umbrella. Whole life insurance is one option under it, built for people who want guarantees over flexibility. Before you sign anything, confirm exactly which type of permanent policy you’re being quoted, the word “permanent” alone doesn’t tell you what you’re actually buying.

If you’re trying to figure out which type of permanent coverage actually fits your goals and budget, M-Life Insurance can walk you through real quotes across whole life, universal life, and final expense options so you know exactly what you’re comparing before you commit to a policy.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.