You got a knock at your door, or a call from an agent and now you’re sitting with a Family Heritage Insurance brochure in your hand wondering if this is legit, if the cancer coverage actually pays out, and whether the “return of premium” promise is real or a gimmick.

That hesitation is healthy. Too many people either buy without reading the fine print or cancel prematurely without understanding what they actually have. This guide gives you the full, unfiltered picture of Family Heritage Insurance, like the products, the payouts, the complaints, and the honest verdict, so you can decide with confidence.

What Is Family Heritage Life Insurance, and Who Actually Owns It?

Family Heritage Life Insurance Company of America is a supplemental health and life insurance provider, not a standard health insurance carrier. That distinction matters more than most agents will volunteer.

In 2019, Family Heritage changed its name to Globe Life Family Heritage Division after becoming an affiliate of Torchmark Corporation in 2012. So when you search “Family Heritage life insurance company, you’re really looking at a Globe Life subsidiary, one of the largest insurance groups in the United States.

Today, Family Heritage Life offers its products in 49 states and focuses on life insurance and supplemental health products including cancer coverage and accident coverage. AM Best gives it an “A” rating and places it in the $1.25–$1.5 billion financial size category.

The “A” financial strength rating from AM Best, the insurance industry’s leading credit rating agency, means that the company can pay its claims. That’s the floor you need before trusting any insurer with your premiums.

What Does Family Heritage Supplemental Insurance Actually Cover?

Family Heritage supplemental insurance fills gaps your primary health plan leaves open, it does not replace it.

Their products include cancer policies that pay benefits upon diagnosis, intensive care (ICU) coverage that applies to any illness or accident requiring ICU confinement, heart and stroke policies, and accident injury policies.

Here’s how the core products stack up:

| Product | What It Pays For | Who It’s Best For |

| Cancer Insurance | Diagnosis, treatment, travel, lodging | Anyone with family cancer history |

| Accident Insurance | ER visits, hospitalization, fractures, burns | Active adults, families with children |

| ICU / Critical Illness | Any ICU stay regardless of cause | Broad coverage seekers |

| Heart & Stroke | Out-of-pocket costs from cardiac events | Adults 40+ with cardiovascular risk |

| Life Insurance | Death benefit for adults and children | Families needing permanent coverage |

All plans pay in addition to any other insurance you own, pay benefits directly to the policyholder, not the hospital and include a 100% return of unused premiums.

Family Heritage Cancer Insurance Return of Premium: Real or Marketing?

It’s real, but “unused” is the operative word, and most people miss it.

The return of premium feature on Family Heritage cancer insurance means if you never file a claim and the policy reaches its designated return date, you receive your paid premiums back. Globe Life Family Heritage advertises this as a win-win situation, you either use the coverage when you need it, or you get your money back.

Family Heritage Insurance Phone Number, Login & Customer Service

If you’re already a policyholder and need help fast, here’s what you need to know.

Family Heritage Life Insurance phone number: The primary contact number is 1-844-726-4371. Average call time is around 3 minutes, with the shortest wait times on Sundays and the longest on Mondays.

Family Heritage insurance login: Policy management has moved under the Globe Life umbrella. You can log in and manage your policy at home.globelifeinsurance.com/familyheritage.

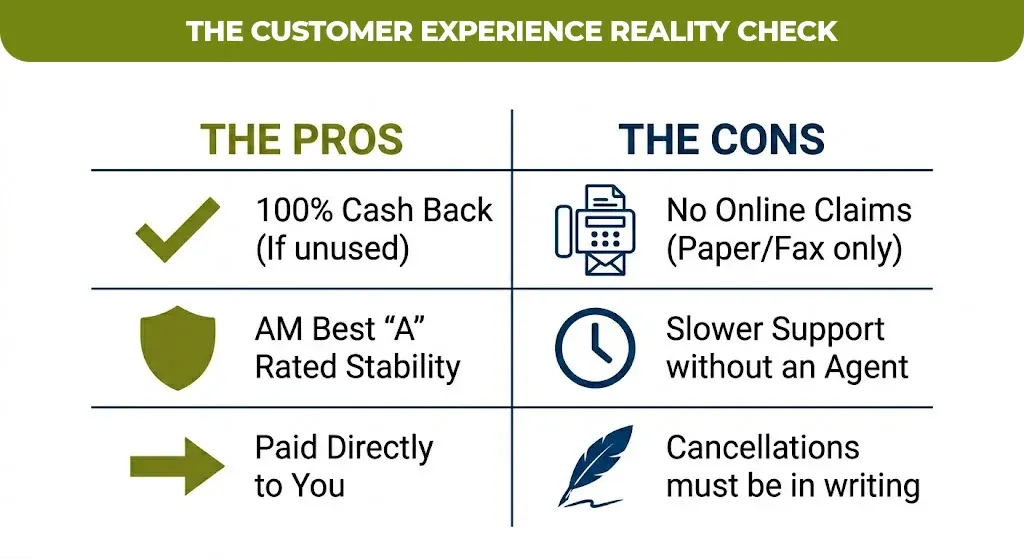

Family Heritage insurance customer service options include phone inquiries, a general contact form through their website, and fax for claims. Notably, the company does not offer online or phone claims filing directly, claims are submitted via fax or mail, which is a meaningful friction point for people expecting modern digital service.

If you want or are trying to cancel your policy, do it in writing and keep every record. Multiple customer reviews flag that verbal cancellation requests are not always actioned.

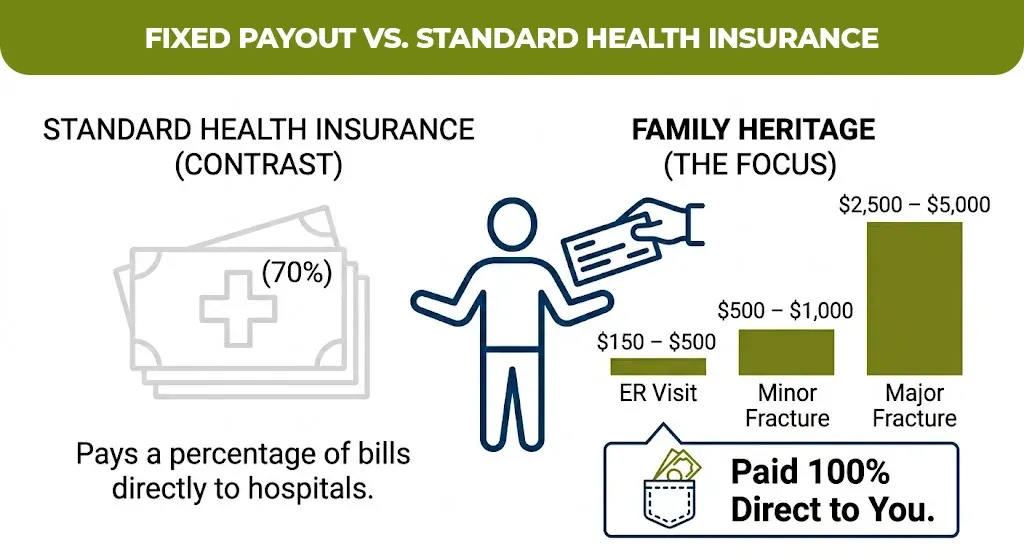

Family Heritage Accident Insurance Payouts: What to Realistically Expect

Accident insurance from Family Heritage pays a scheduled benefit, it means that there is a fixed dollar amount that is tied to specific injuries or events, not a percentage of your actual medical bill.

A typical Family Heritage accident insurance payouts chart would look something like this

| Event | Estimated Payout Range |

| Emergency Room visit | $150 – $500 |

| Fracture (minor, e.g., finger) | $500 – $1,000 |

| Fracture (major, e.g., hip) | $2,500 – $5,000 |

| Hospitalization (per day) | $100 – $300/day |

| Ambulance transport | $150 – $400 |

| Follow-up therapy | $30 – $75/visit |

American Family Heritage Insurance vs. Family Heritage Life: Are They the Same?

No, and confusing them is a costly mistake.

Family Heritage Life

Family Heritage Life Insurance Company of America (now Globe Life Family Heritage Division) focuses on supplemental health products like cancer, accident, ICU coverage and is based in Cleveland, Ohio.

American Family Heritage

American family heritage insurance and “heritage family insurance” are terms that often appear in searches but may refer to entirely different carriers depending on your state. American Heritage Life Insurance Company, for example, is an Allstate subsidiary and operates differently in both products and service models.

The Honest Verdict: Is Family Heritage Life Insurance Worth It?

For supplemental coverage specifically cancer, accident, and ICU, the product design is solid. The execution is inconsistent.

The return of premium features is a genuine differentiator. The AM Best “A” rating confirms financial stability. And the payouts-directly-to-you structure is genuinely useful when a crisis hits.

But the agent-dependent distribution model means your experience will vary enormously based on who sold you the policy. Claims filed without agent support can hit significant delays. Customer service, by modern standards, is behind the curve.

If you’re considering Family Heritage supplemental insurance, work through a licensed independent agent who has a track record of helping clients through claims, not just the initial sale.

Not Sure Which Coverage Fits Your Situation?

Understanding supplemental insurance like how it layers with your primary plan, what it actually pays, and where the gaps are can take time most people don’t have when they need it.

mlife Insurance will help the people to compare supplemental and life insurance options in plain language, without the pressure of a door to door pitch. If you are trying to figure out if a policy like Family Heritage makes sense for your family’s situation or not, it’s a solid place to start your research.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.