Your health is keep changing since you bought your term life insurance policy and now you are thinking if you waited too long. Convert at the wrong time or with the wrong provider, and you could log in a permanent premium that will far more higher as compared to it needed to be, or even it is so worse.

This is the part most of the term life insurance buyers never read closely like the conversion loss. It is the one line in your policy that will decide if you have a safe night later or nothing at all.

What Is Convertible Term Life Insurance?

A convertible terminal insurance policy is the term policy that can include the right to switch to the permanent policy, such as more universal life insurance without any medical exam or any healthcare questionnaire. You keep the rating you qualified for when you first bought the policy, even if your health has since declined.

The conversion features are either built into the policy automatically or they are added as the rider. It totally depends on the carrier. It does not cost extra to have the option like you only pay more once you actually convert, because the permanent coverage is priced differently as compared to term.

How Does Converting Term Life Insurance Actually Work?

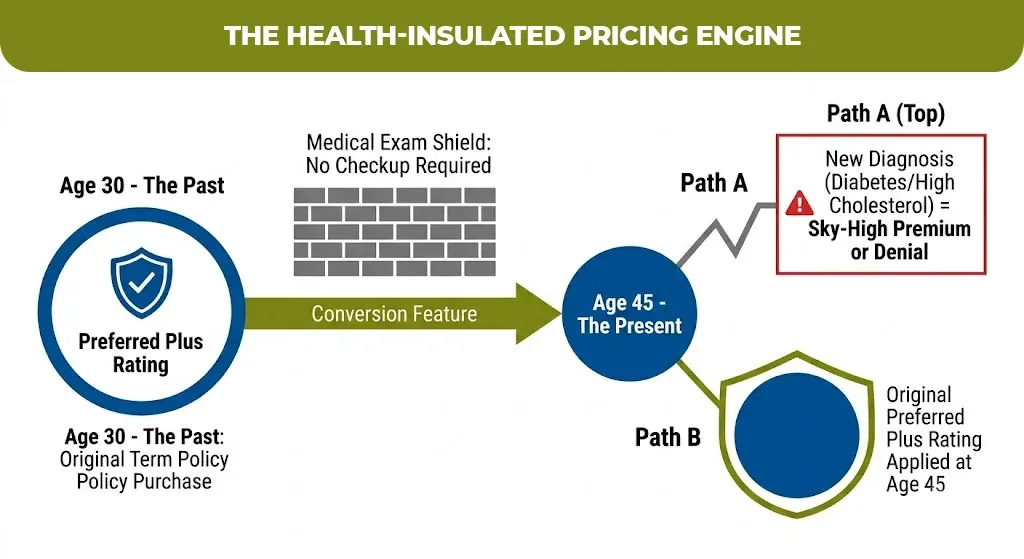

Converting term life insurance policy in contacting your insurance company before your conversion window process and requesting to move some of or all your death benefit into the permanent policy at the same company. The insurance company the price is the coverage using your current age, but it will keep your original health classification.

The distinction matters a lot.A 45-year-old converting a policy bought at age 30, with a Preferred health rating from back then, still gets Preferred permanent life pricing today, even if a checkup last year turned up high cholesterol or a new prescription.

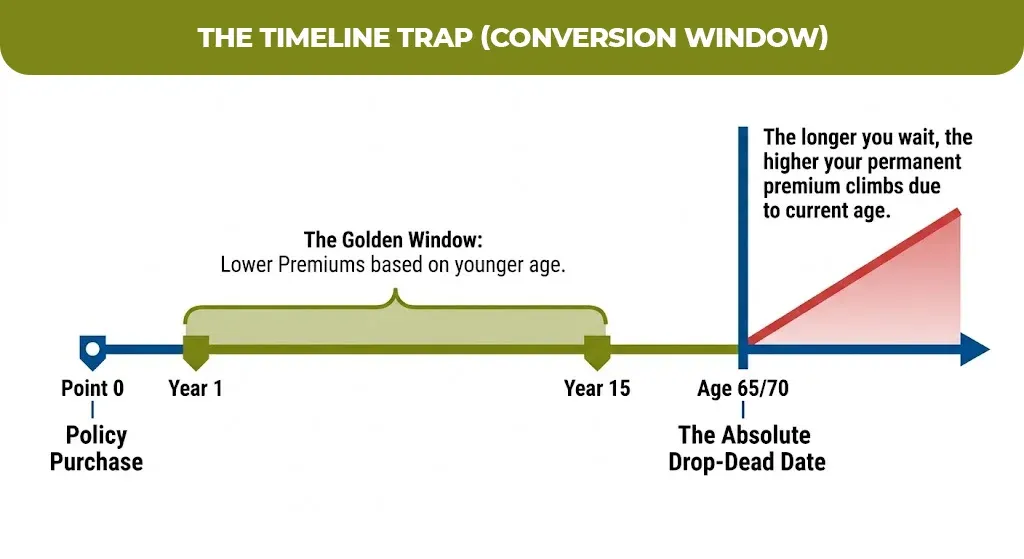

According to U.S. News’s 2026 review of convertible life insurance most of the carrier restrict when you are allowed to convert. Some The window at the first 10 to 15 years of the policy like others will let you convert any time before a set age that is often 65 or 70 years. Most of the carrier restrict when you are allowed to convert. Some The window at the first 10 to 15 years of the policy like others will let you convert any time before a set age that is often 65 or 70 years.

Waiting until the last year of that window is the single most common mistake, because your permanent premium is based on your age at conversion, not your original purchase age.

Convertible Term Life Insurance Pros and Cons

| Pros | Cons |

| No new medical exam required | Permanent premiums cost more than term |

| Keeps your original health rating | Only available during a limited window |

| Builds cash value once converted | Insurer may limit which permanent products you can convert into |

| Guarantees future insurability | A conversion fee may apply, based on the amount converted |

| Allows partial conversion | Once the window closes, the option is gone permanently |

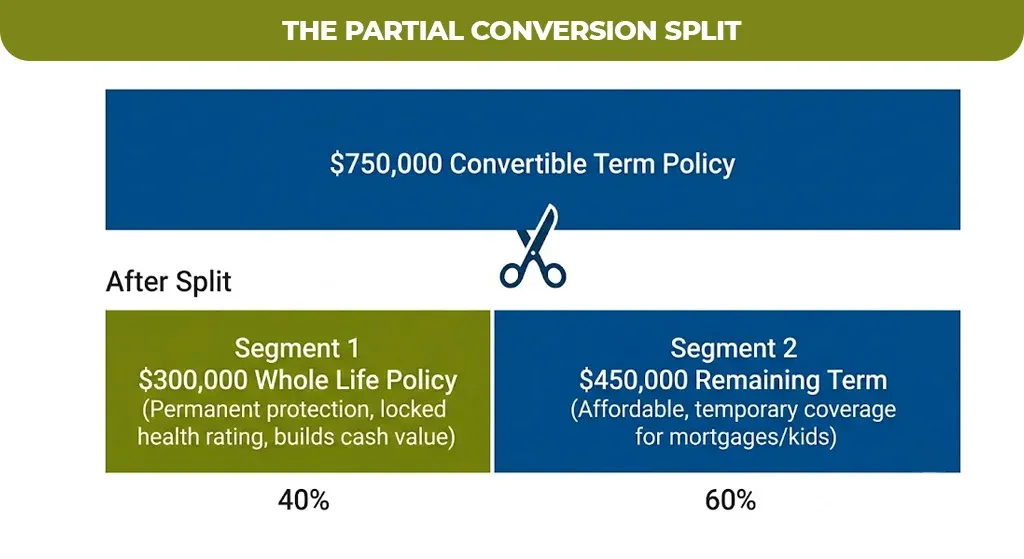

The partial conversion is worth knowing about if the full switch feels too expensive. If you want a $500,000 convertible life insurance policy, then you can generally convert $200,000 to permanent coverage and keep the remaining $300,000, which will lower the new premium but still lock in some lifetime protection.

Convertible vs. Renewable Term Life Insurance

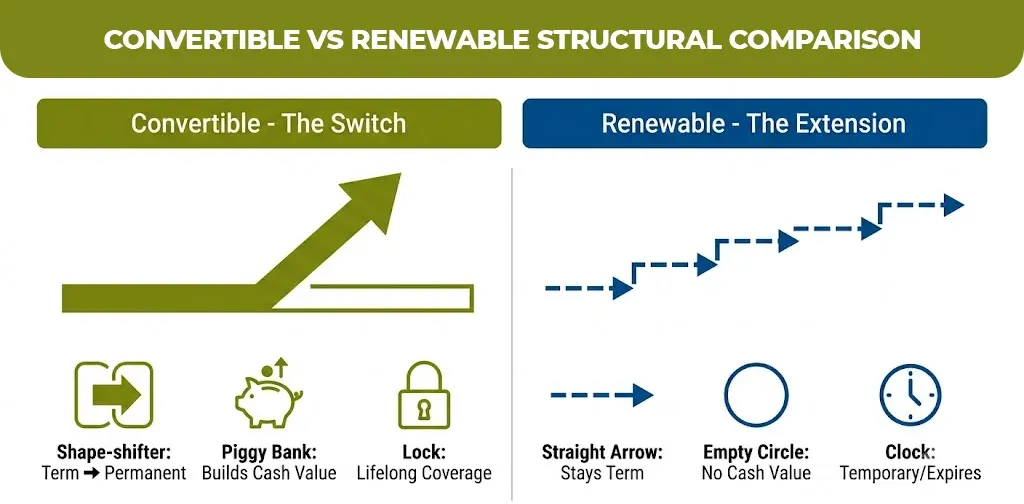

These two features get confused constantly, and the difference changes what your money buys you.

| Feature | Convertible Term | Renewable Term |

| What it does | Switches you to a permanent policy | Extends your existing term coverage |

| Medical exam needed | No | No |

| Premium after the change | Higher, permanent-policy pricing | Higher, but still term-level pricing |

| Cash value | Yes, once converted | No |

| Best for | Needing lifelong coverage or protecting insurability | Needing a few more years of term coverage |

Renewable terms keep you in the same type of policy, just extended and repriced. Convertible terms change what kind of policy you have altogether, moving you from coverage that expires to coverage that doesn’t.

When Should You Convert Term to Whole Life Insurance or Universal Life?

convert your plan when your health has changed, your financial applications have become permanent or when you are approaching the end of your conversion window and still want the option available. All these are the three situations where the converting actually pays off, not just nice to have

Your Health Has Declined

This is the most common and the most valuable reason to convert. Lock in euro original reading can save you from being denied new coverage entirely.

Your Obligations Turned Permanent

A dependent with lifelong care needs, a growing state that can face state tax or a business succession plan or all recent term that expired no longer fits.

Your Window Is Closing And You’re Unsure

Some of the carriers offered partial conviction specifically so you do not have to choose all or nothing before a deadline.

If all of the above are not applying, letting the term life insurance simply expire is not a loss. It means the policy did exactly what it was designed to do and it is to protect you while a mortgage, Yonkers or other temporary obligations were active. above are not applying, letting the term live insurance simply expire is not a loss. It means the policy did exactly what it was designed to do and it is to protect you while a mortgage, Yonkers or other temporary obligations were active.

Converting After a Health Diagnosis – Understanding With Example

Consider a 42-year-old who bought a 20-year, $750,000 convertible term policy at age 32 with a Preferred Plus health rating. At 42, a new type 2 diabetes diagnosis would make new coverage expensive or hard to qualify for on the open market.

Because the original policy is convertible, this person can convert $300,000 of that death benefit into a whole life policy this year, using the Preferred Plus rating from a decade earlier. The remaining $450,000 stays as term for the rest of the original 20-year period, keeping the overall premium manageable while still locking in permanent, health-proof coverage where it matters most.

How Much Does It Cost to Convert Term Life Insurance?

Expect your premium to increase by roughly 10% to 15% or more when you convert, since permanent insurance is priced to last a lifetime and build cash value rather than expire. Some insurers also charge a separate conversion fee, typically based on the size of the death benefit being converted.

The exact number depends on your age at conversion, the permanent product your carrier offers for conversions, and how much of the death benefit you switch. Converting earlier in your window, rather than waiting until it’s about to close, is the most reliable way to keep that increase on the lower end.

Working through whether to convert, and which permanent product actually fits your numbers, is easier with a second set of eyes on your specific policy. M-Life Insurance can walk through your current coverage and conversion window with you and lay out the real cost difference before you decide anything.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.