The Self Employed Health Insurance Deduction: How It Actually Works in 2026

The self employed health insurance deduction will allow you to deduct 100% of the premiums you pay for the medical, dental, vision and eligible long-term care insurance for yourself, your spouse and your dependence. You do not need to itemize your taxes to claim this deduction. Instead you can report it on Schedule 1 (Form 1040), Line 17, using IRS Form 7206 to calculate the exact amount.

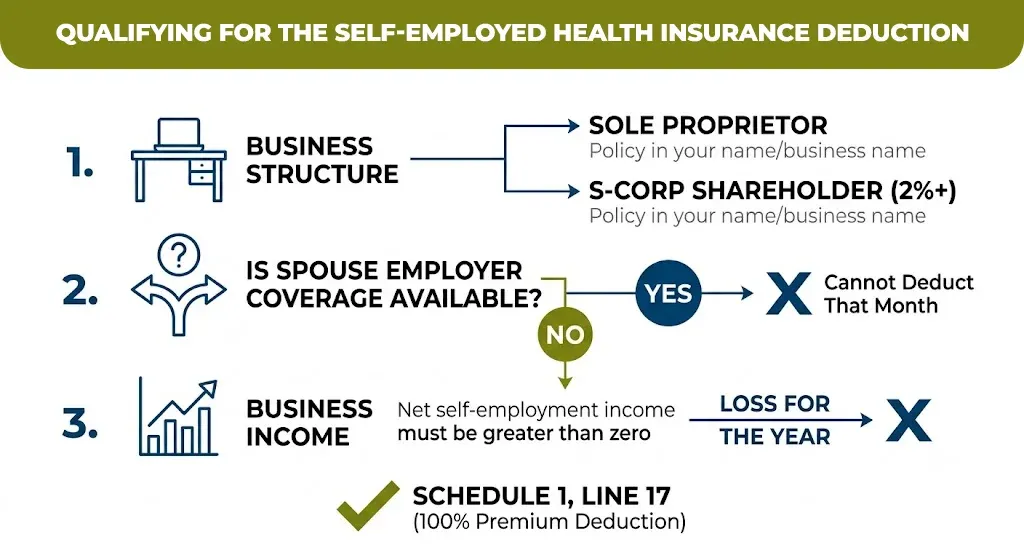

Three conditions determine whether you qualify

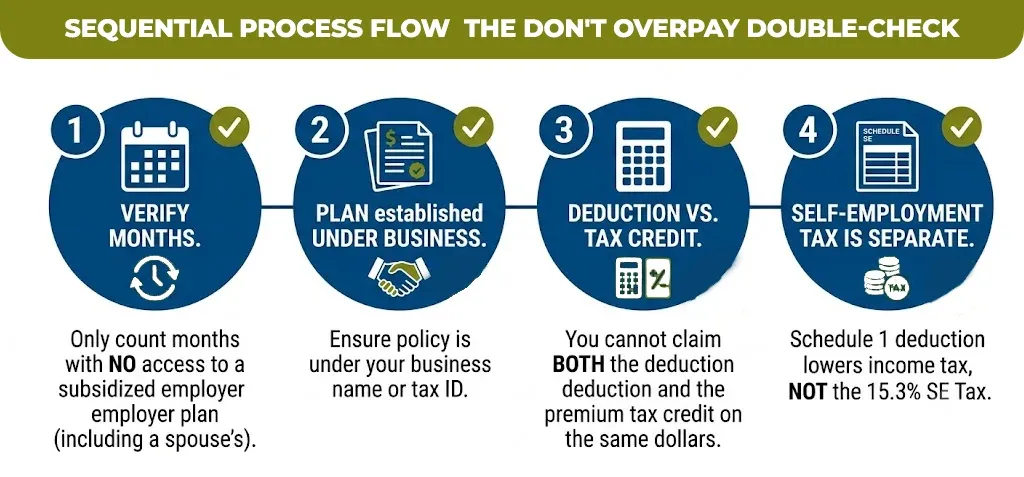

Your Plan Must Be Established Under Your Business

A policy in your name, or on your sole proprietorship’s name, your partnerships name or if you are an S-Corp shareholder or the employee owning more than 2% than reported correctly through your W-2.

You Can’t Have Access To A Subsidized Employer Plan

This will include your spouse employer plan. If your spouse will enroll you in the coverage through their job then even if you decline it, you will lose the deduction for those months under IRS rules for Form 7206.

The Deduction Can’t Exceed Your Net Self Employment Income

A business with a loss for the year generally will not claim the deduction against other income.

There is one detail that will catch almost everyone off guard and it is that the self employed health insurance deduction will lower your income tax, but it will not reduce the 15.3% self employed tax calculated on schedule SE. It’s a real savings, just not a self employment tax savings.

Health Insurance For Self Employed Deduction Vs. The Premium Tax Credit — You Can’t Use Both

This is where a lot of self-employed filers accidentally cost themselves money. You cannot claim the self employed health insurance deduction and the ACA premium tax credit on the same premium dollars. If you receive advance premium tax credits, you can only deduct the portion of the premium you actually paid out of pocket, and the IRS runs a circular calculation that is detailed in Publication 974 to determine which combination gives you the larger benefit. A tax professional or tax software built for self-employment (not a generic filing tool) will run this calculation correctly, doing it by hand is where most errors happen.

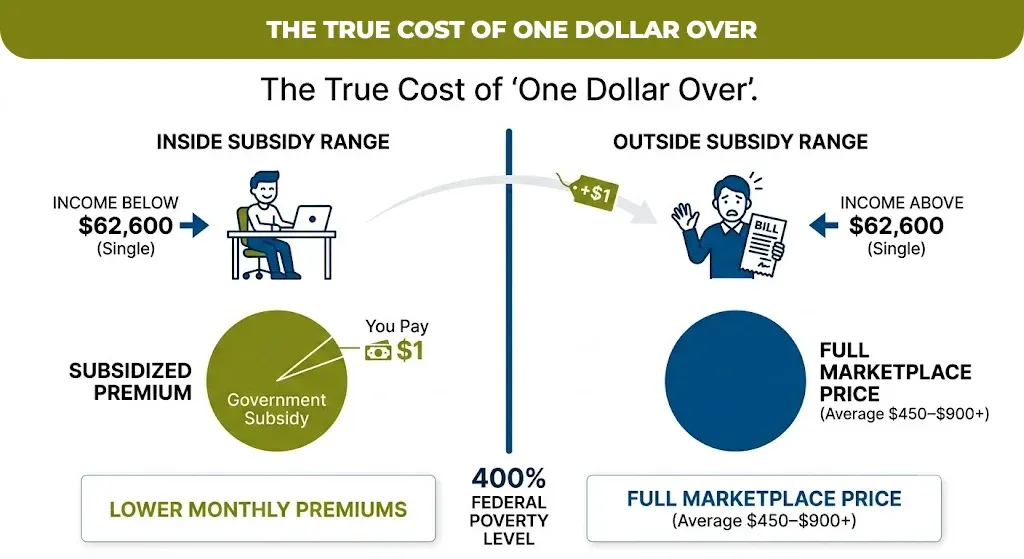

The 2026 Subsidy Cliff: Why It Matters More for Self-Employed Income

The extra ACA premium tax credit data started in 2021 were not renewed for 2026. Because of this, the original ACA subsidy rules are back. Now you can only get the premium subsidies if your income is below 400% of the federal poverty level. In 2026, that price is $62,600 for a single person and $28,600 for a family of four in the continental US. If your modified adjusted cross income goes over the limit by even one dollar then you could lose all of your premium tax credit for that year.

| Household size | 2026 subsidy cliff (400% FPL, continental U.S.) |

| 1 person | $62,600 |

| 2 people | $84,600 (approx.) |

| 3 people | $106,600 (approx.) |

| 4 people | $128,600 |

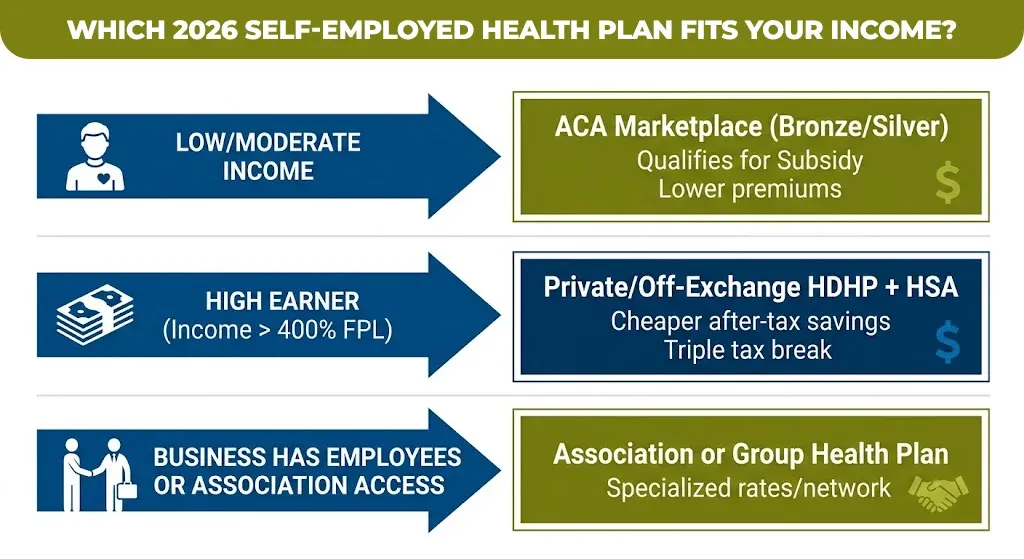

ACA Marketplace vs. Private Plans vs. Group Coverage: Which Fits Your Situation?

| Factor | ACA Marketplace | Private/Off-Exchange | Group (via association or small biz) |

| Subsidy eligible | Yes, if under 400% FPL | No, never | No |

| Deduction eligible (Sched. 1, Line 17) | Yes | Yes | Yes, if plan established under business |

| Guaranteed issue (no health questions) | Yes | Yes (ACA-compliant only) | Usually, if group size met |

| Best for | Income under $62,600 (single) / near cliff | Income above cliff, healthy, wants HSA | Self-employed with 1+ employees, or professional association access |

| Open enrollment restriction | Yes — Nov–Jan, or qualifying life event | No, enroll anytime | Varies by group |

Where to Go From Here

Health insurance is one piece of protecting your income as a self-employed worker, the other is making sure your family isn’t left covering business debts, a mortgage, or lost income if something happens to you. If you haven’t looked at how life insurance fits into that picture, Mlife Insurance has straightforward guides and quotes built for self-employed households, with no pressure to buy on the spot.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.