Buy the wrong life insurance policy and your family might not find out until its due date. Either the coverage lapses when they need it most of the payout will get delayed for the month because the beneficiary form was never updated. That is not a rare story. It happens to the family every year but the plans are based on the sales pitch instead of understanding what they will actually get while signing.

This life insurance FAQ answers the questions people actually type into Google before buying, during a policy and after filing a claim. That is just not the basics every other page covers.

What Is Life Insurance and How Does It Actually Work?

Life insurance is a contract where you have to pay the premiums to an insurance company and then in exchange the company will pay a tax fee that benefits your named beneficiaries when you die. That is the entire mechanism and everything else is a variation on that core promise.

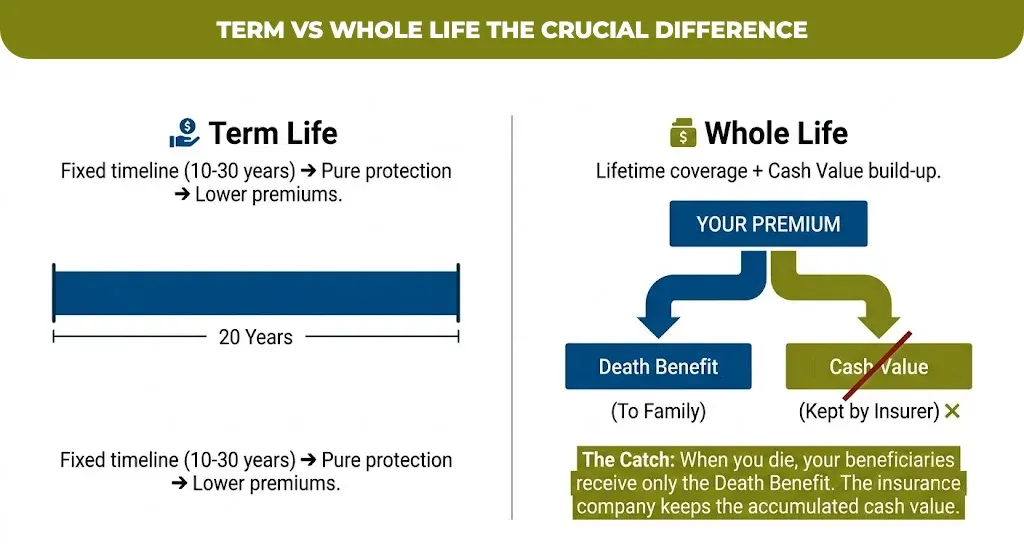

There are two broad categories: the one is term life insurance which covers you for a fixed number of years and the permanent life insurance that will cover you for your entire life and it also builds cash value. Your choice between them shapes almost every other answer in this FAQ.

Term Life Insurance FAQ: What You Actually Need to Know

How long does term coverage last?

Most of the time life insurance policies run 10, 20 or 30 years. With level premiums that do not change during that time. The coverage and when the term ends and there is no payout, no refund and to renew or convert your plan.

Can I convert term life insurance to a permanent policy later?

Yes, most of the term life insurance policies include a conversion writer that will help you to switch the part of all the death benefit to the permanent coverage without a new medical exam as long as you convert within that time specified in your policy. This will matter if you health changes and you would otherwise be denied a new policy.

Whole Life Insurance FAQ: Cash Value, Cost, and Catches

Do I get both the death benefit and the cash value when I die?

No, this is one of the most common misunderstandings. In a standard whole life insurance policy, the insurance company would keep their accumulated cash value and your beneficiaries will receive the policy face value death benefit not the cash value on top of it.

Is whole life insurance worth the higher premium?

It depends on your goal. Whole life insurance premiums generally tend to be significantly higher as compared to term life insurance for the same death benefit. So it seems to make sense for the permanent needs like state planning, special need dependent or the final expense coverage. It is not a general savings account for most of the working age families.

How Much Life Insurance Coverage Do I Actually Need?

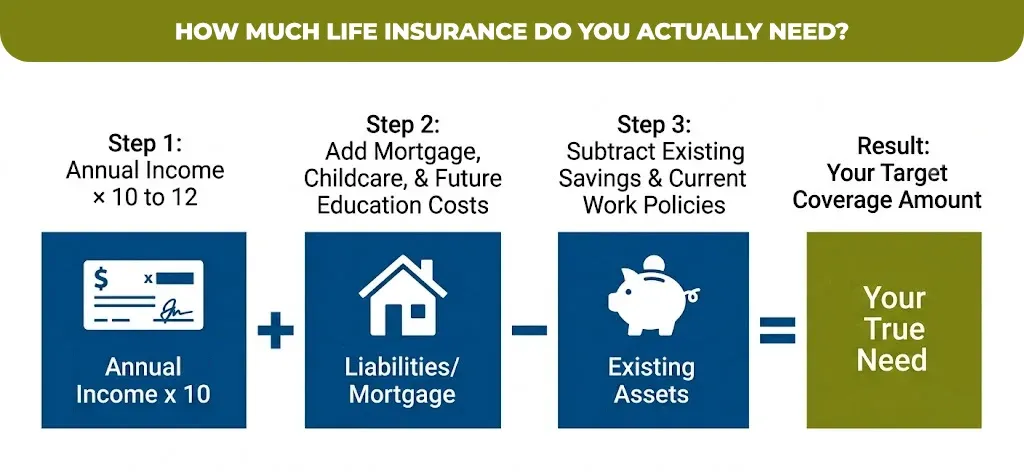

A common starting point is 10 to 12 times your annual income and it is adjusted for the outstanding tax and future obligations. Add your mortgage case balance, remaining years of childcare or education cost and subtract any existing savings or the coverage you already have through your work.

This is not a one size number, this is a single 25 year old with no dependent need for far less than 40 years old with a mortgage for three kids. Run your own actual tax and rather than default to the round figure an agent suggests.

Life Insurance Claims FAQ: What Happens When You File

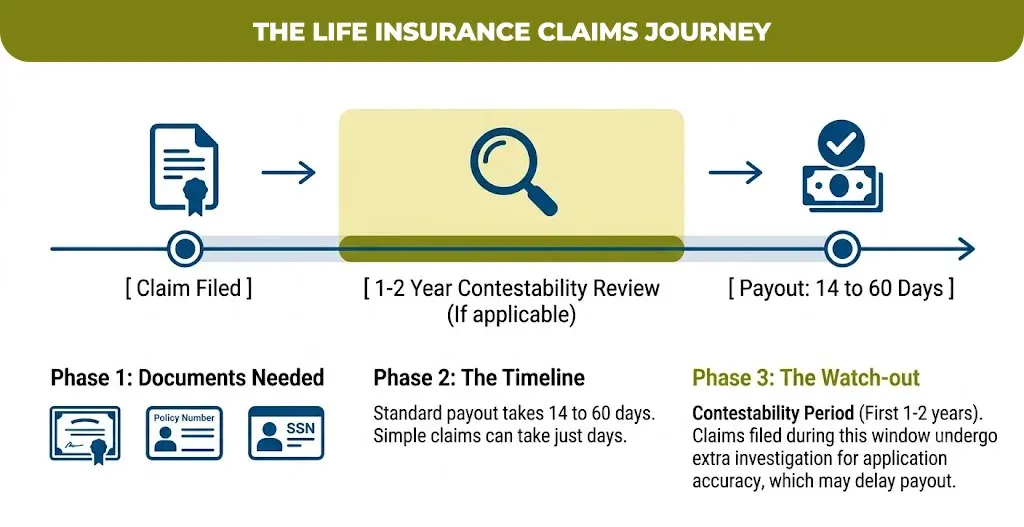

How long does it take for a beneficiary to get paid?

Most of the insurance companies’ space is acclaimed within 14 to 60 days of receiving a complete claim and simple claim with no complication can sometimes pay in as little as a few days or two weeks which of the claims involving the cons period, and unclear cause of death or missing paperwork take longer.

What is the contestability period and why does it matter?

It is generally the first one or two years after policies are issued, during which the insurance company can investigate the application more closely if a claim is filed. If no fraud or miss presentation is found then the claim is paid but the review itself can add to the timeline.

What documents does a beneficiary need to file a claim?

Generally a certified copy of that certificate, the policy number and the insured Social Security number is needed to complete a claim form. Most of the insurance companies also accept claims that our fight online which tend to move faster than mailed paperwork.

Is there a deadline to file a life insurance claim?

No, and in most of the cases there is no time limit so the beneficiaries can take the time they need before filing. The payout remains as long as the policy is active when the insured person dies.

Is Life Insurance Taxable? What Beneficiaries Need to Know

Generally no, the life insurance procedure pays to name the beneficiary because of the insured percentage that is not included in the cross income and does not need to be reported. This is confirmed directly by the IRS guidance on life insurance and disability insurance proceeds.

No-Medical-Exam and Guaranteed-Acceptance Life Insurance FAQ

Can I get life insurance without a medical exam?

Yes, the simplified issue policy skipped the exam but still asked the questions on the application. While the guaranteed issue policies are no health questions at all and except nearly everyone within an age range. Both trade the convenience for high premiums and lower coverage caps as compared to full under written policies.

Who should consider guaranteed-issue coverage?

It tends to fit the older applicants or the people with serious health conditions who would have otherwise declined for the standard coverage. Most commonly for the smaller final expense policies than the large income replacement needs. The guaranteed issue policies generally include a graded death benefit for the first two years. It means a reduced payout if the death occurs early from non-accidental causes.

Group Life Insurance FAQ: What Your Employer’s Policy Actually Covers

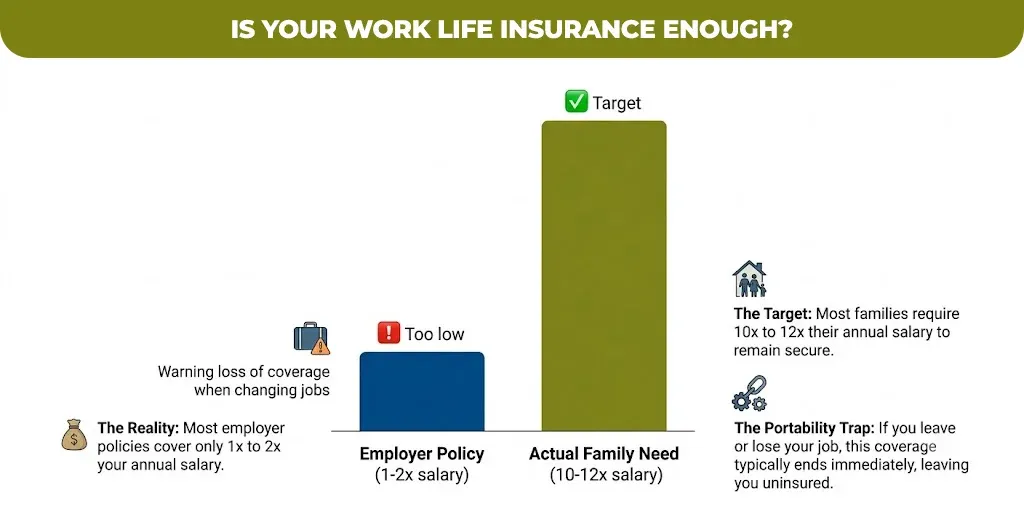

Is the life insurance my employer provides enough?

Thursday not on its own, most of the employer group policies provide one to two times your salary. Very short for 10 to 12 time benchmark most of the families need. Treat it as supplemental to the personal policy, not the replacement for your main one.

What happens to my group life insurance if I leave my job?

In most of the cases, the coverage ends when your employment ends and some of the employers allow you to convert to an individual policy within an unlimited window, usually a higher premium. This is one of the biggest gaps that people do not discover until they are between jobs or uninsured.

Life insurance decisions get easier once you know which questions actually matter for your situation and coverage amount, term length, and how the payout gets taxed. If you’d like help running your specific numbers, MLife Insurance can walk you through real quotes for your age and health profile, at no cost and no pressure to buy.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.