Most people shopping for life insurance land on return of premium policies because the pitch sounds almost too good: pay for coverage for 20 or 30 years, and if you’re still alive at the end, you get every dollar back. Tax-free.

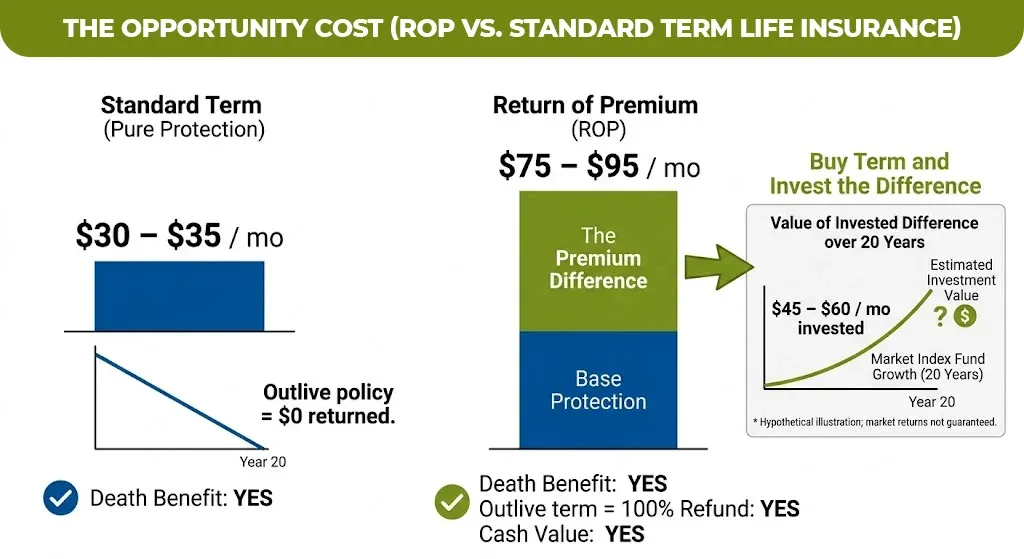

That’s real. It works exactly as advertised. But here’s what nobody tells you upfront: you’ll pay 2 to 3 times more than a standard term policy for that guarantee and whether that trade-off makes sense depends entirely on your situation, not on how good it sounds in a brochure.

The wrong choice here doesn’t just cost you money. It can lock you into a policy you can’t afford to keep, or push you away from a policy you genuinely needed.

What Is the Return of Premium Life Insurance, Exactly?

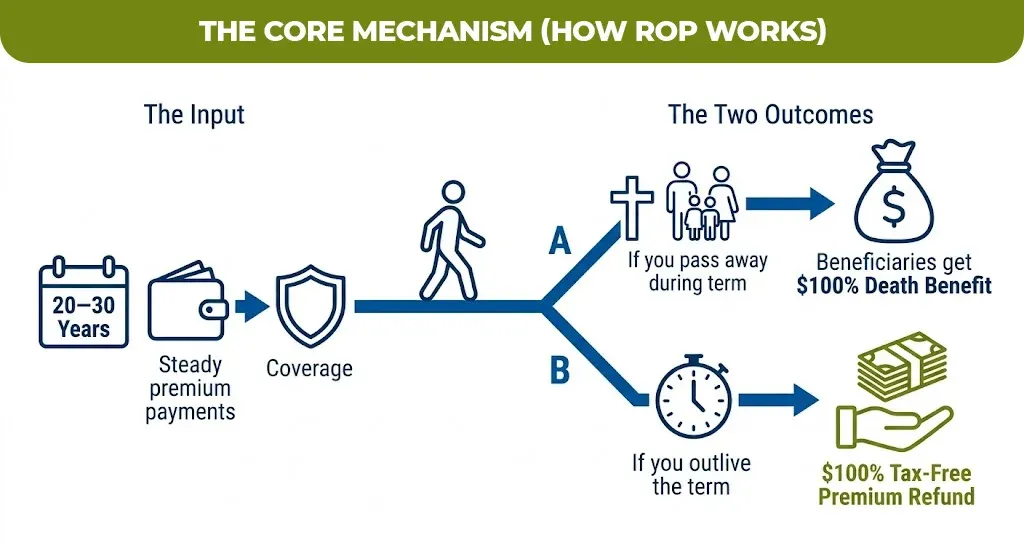

Life insurance return of premium term life policy that will refund 100% of your premiums if you outlive the coverage time. If you die during the term, then your beneficiaries receive the full death benefit just like any standard policy.

The key difference is that, with regular term life insurance, if you outlive your policy, you receive nothing. With an ROP policy, you get every premium dollar back at the end of the term, and the IRS does not consider that refund taxable income

A return of premium life insurance policy is not the same as whole life, universal life, or variable life insurance, even though it builds cash value over time. It’s still a term product. It has a set end date. When that date arrives, either your family collects the death benefit, or you collect your premiums back.

Return of Premium Term Life Insurance Pros and Cons

No product is right for everyone. Here’s the honest breakdown.

Comparison Table – ROP vs. Standard Term Life Insurance

| Feature | Standard Term Life | Return of Premium Term |

| Monthly cost (35M, $500K, 20yr) | $30–$35/month | $75–$95/month |

| Death benefit | Yes | Yes |

| Premium refund if you survive | No | Yes |

| Cash value | No | Builds over time |

| Can borrow against policy | No | Yes |

| Best for | Tight budgets, pure protection | Savers who want a guaranteed return |

| Worst for | Those who want money back | Active investors comfortable with market risk |

Pros

- Guaranteed return

- Refund is 100% tax-free per IRS guidelines

- You still carry life insurance protection for your family throughout

- Can borrow against the cash value before the term ends

Cons

- Significantly higher premiums

- If you cancel early, you may receive little to nothing back

- The premium difference, if invested, would likely outperform the refund over time

- Fewer carriers offer ROP in 2026 than in prior years

Best Return of Premium Life Insurance Companies in 2026

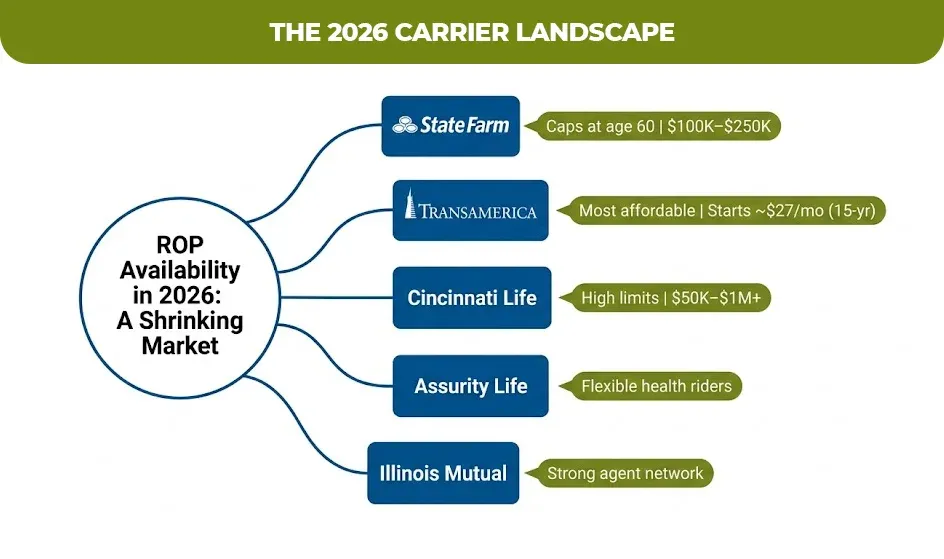

Finding an ROP policy has gotten harder. Many carriers have quietly exited this product category over the past five years. As of 2026, the carriers that consistently receive strong marks for ROP policies are:

State Farm

The company gives 20 or 30-year terms, $100K–$250K coverage, ages 18–60, strong bundling discounts.

Cincinnati Life

Comes with Termsetter ROP product, $50K–$1M+ coverage, 20, 25 or 30 year terms, direct underwriter access

Assurity Life

ROP rider available on 20 and 30-year terms, flexible for qualifying health classes

Illinois Mutual

User-friendly quoting process, available in most states, strong agent support

Transamerica

Among the most affordable ROP rates, starting around $27/month for 15-year terms

Senior Life Return of Premium Life Insurance: What’s Different for Older Buyers

Senior life return of premium life insurance is a distinct product designed for applicants typically aged 50–75 who want coverage without permanently losing their premium payments.

The Honest Reality For Seniors

Qualifying for standard ROP policies gets harder with age. Most carriers cap ROP eligibility between age 60 and 65 at the time of application. State Farm, for example, accepts applicants up to age 60 for their ROP product.

Senior Life Insurance Company of America markets a specific 20 year ROP product aimed at seniors, with face amounts from $10,000 to $50,000 that is designed primarily for final expense coverage rather than income replacement. If you outlive the 20 year term, you receive 100% of your premiums back.

Who this makes sense for

A healthy 55-year-old who wants final expense coverage through age 75, values the certainty of getting their money back, and can comfortably absorb the higher monthly premium without straining their retirement budget.

Who should look elsewhere

Seniors on fixed incomes where the extra premium cost creates financial pressure because if you lapse the policy early, you lose the refund guarantee entirely.

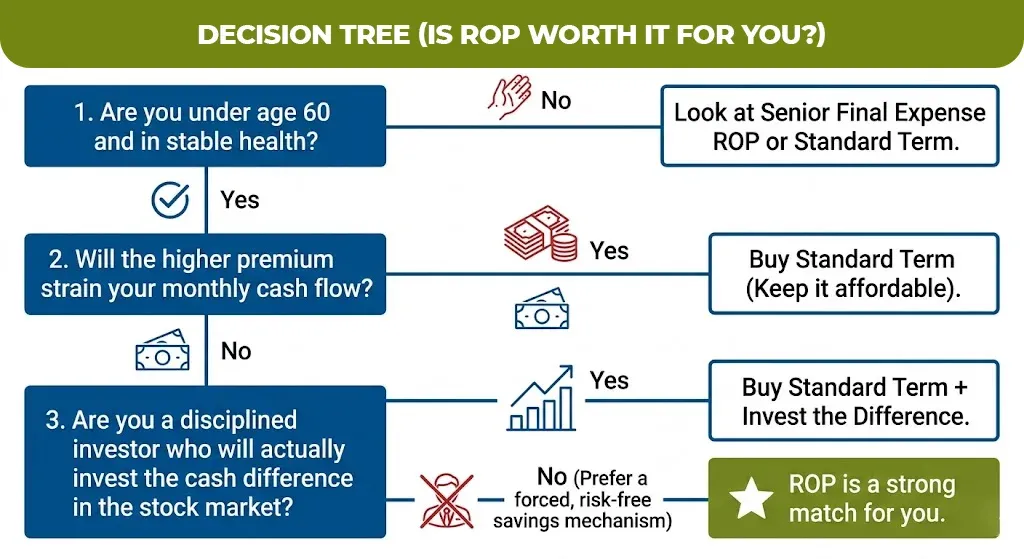

Is Return of Premium Life Insurance Worth It? The Honest Answer.

It depends on one thing like how you feel about guaranteed outcomes versus investment returns.

If you would invest the premium difference in the market and stay disciplined for 20–30 years, standard term life + investing the difference will likely produce more wealth. Historical market data supports this.

ROP makes the most sense if:

- You are in your 30s or 40s, in good health, and can lock in low rates now

- You value guaranteed, risk-free returns over market-dependent growth

- You have a specific time horizon in mind kids leaving home, mortgage paid off, retirement

- You want both life insurance protection and a forced savings mechanism

ROP likely isn’t the best fit if:

- You are on a tight budget and the premium increase would strain you

- You are already a disciplined investor with a diversified portfolio

- You are over 60 and coverage options are limited

How to Get Return of Premium Life Insurance Quotes Without Wasting Time

Getting return of premium life insurance quotes requires working with either a carrier directly or an independent agent who has access to multiple ROP-approved carriers. Not every broker or quote aggregator can surface these policies.

What to tell any agent or quote tool:

- Confirm you want an ROP policy specifically

- Ask whether the ROP is built into the base policy or offered as a rider

- Ask what happens if you cancel at year 10 vs. year 15

- Make sure to compare at least 3 insurance companies before committing

Looking for Reliable Guidance on Life Insurance Options?

If you are still weighing if an ROP policy fits your situation, the most useful next step isn’t another comparison article, it’s a conversation with someone who can look at your actual numbers.

Visit MLife insurance to connect with licensed agents who specialize in term life and return of premium policies across multiple carriers. No pressure, no sales scripts, just a clear look at what’s available for your age, health, and coverage goals.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.